Academic Profile

Statistics

Similar Authors

Papers on arXiv

Attention heads retrieve: given a query, they return a softmax-weighted average of stored values. We show that this computation is one step of gradient descent on a classical energy function, and that...

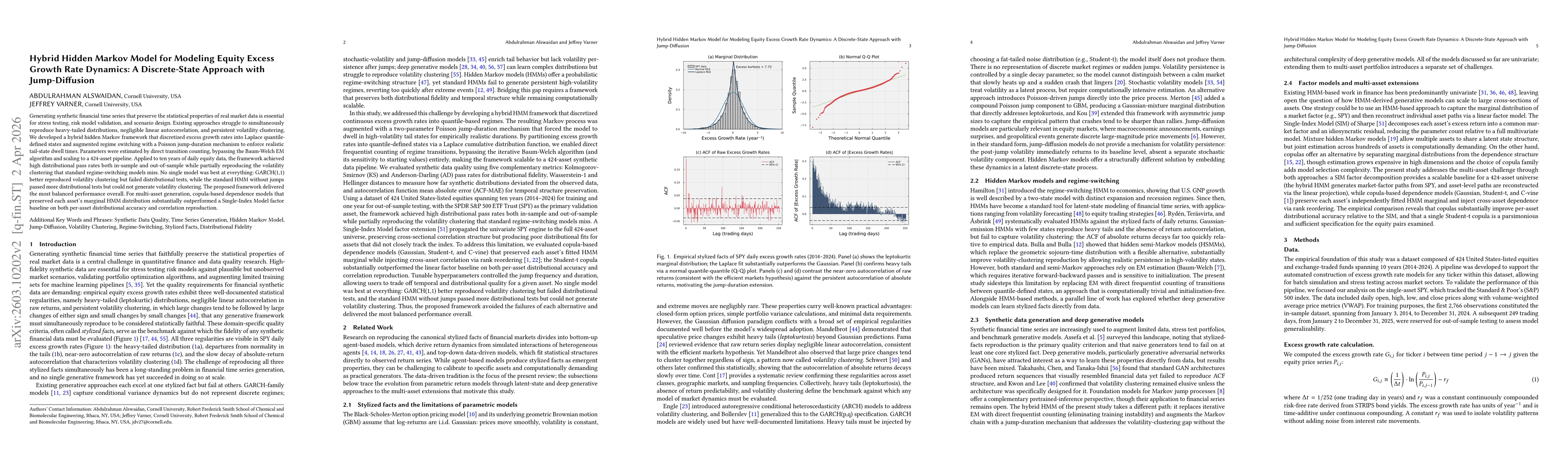

Generating synthetic financial time series that preserve statistical properties of real market data is essential for stress testing, risk model validation, and scenario design. Existing approaches, fr...

Synthetic generators of daily equity returns let practitioners stress test, backtest, and design scenarios that a single realized market history cannot supply, but only if the generator reproduces the...