Academic Profile

Statistics

Similar Authors

Papers on arXiv

We empirically analyze a large sample of firm sales growth expectations. We find that the relationship between forecast errors and lagged revision is non-linear. Forecasters underreact to typical (p...

In this paper, we propose ex-ante characteristics that predict the drop in risk-adjusted performance out-of-sample for a large set of stock anomalies published in finance and accounting academic jou...

Yes, but only at short lags. In this paper we investigate the relationship between factor momentum and stock momentum. Using a sample of 72 factors documented in the literature, we first replicate e...

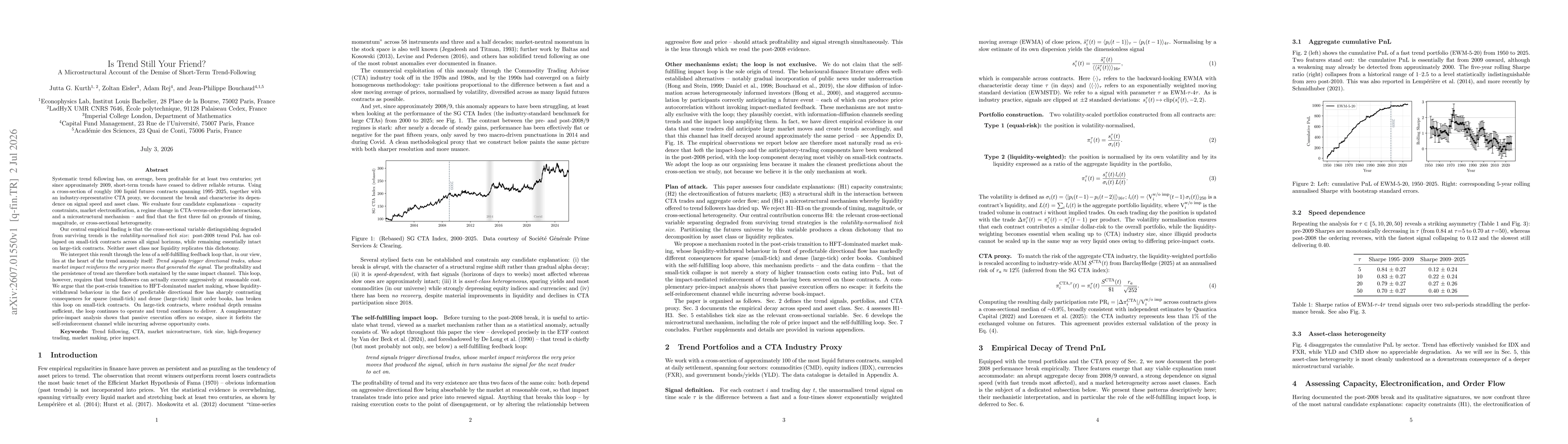

Systematic trend following has, on average, been profitable for at least two centuries; yet since approximately 2009, short-term trends have ceased to deliver reliable returns. Using a cross-section o...