Academic Profile

Statistics

Similar Authors

Papers on arXiv

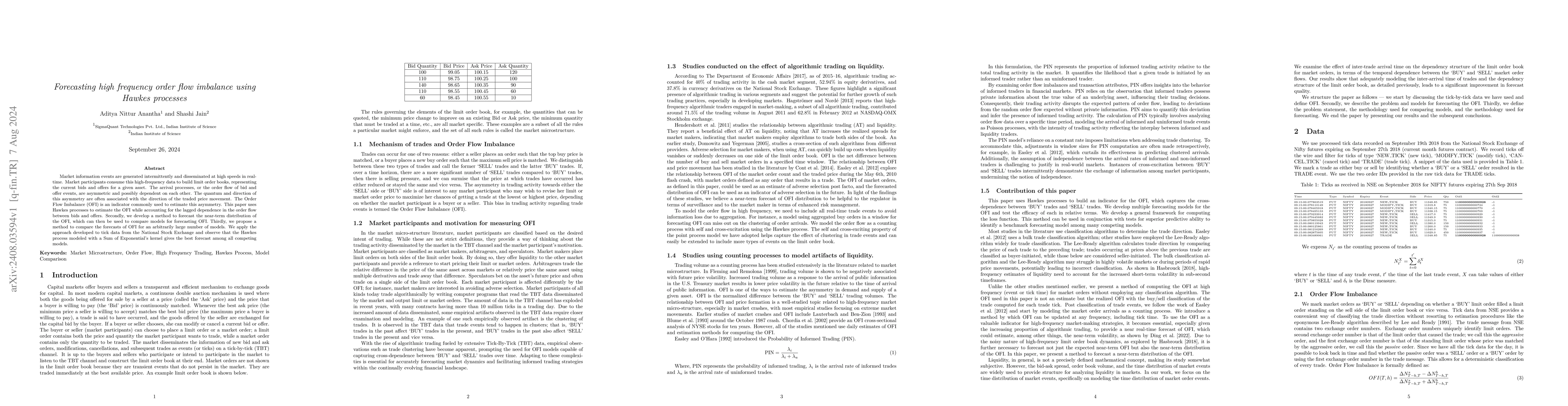

Market information events are generated intermittently and disseminated at high speeds in real-time. Market participants consume this high-frequency data to build limit order books, representing the c...

Quoting algorithms are fundamental to electronic trading systems, enabling participants to post limit orders in a systematic and adaptive manner. In multi-asset or multi-contract settings, selecting t...

With the advent of electronic capital markets and algorithmic trading agents, the number of events in tick-by-tick market data has exploded. A large fraction of these orders is transient. Their epheme...