Academic Profile

Statistics

Papers on arXiv

Multivariate adaptive regression splines (MARS) is a popular method for nonparametric regression introduced by Friedman in 1991. MARS fits simple nonlinear and non-additive functions to regression d...

Multivariate, heteroscedastic errors complicate statistical inference in many large-scale denoising problems. Empirical Bayes is attractive in such settings, but standard parametric approaches rest ...

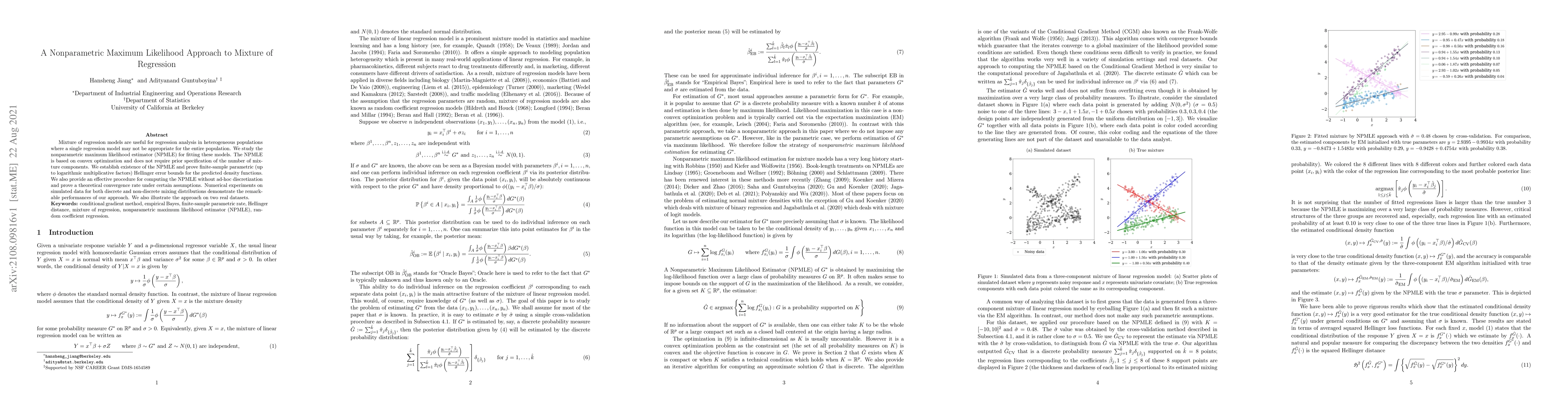

Mixture of regression models are useful for regression analysis in heterogeneous populations where a single regression model may not be appropriate for the entire population. We study the nonparamet...

We prove minimax bounds for estimating Gaussian location mixtures on $\mathbb{R}^d$ under the squared $L^2$ and the squared Hellinger loss functions. Under the squared $L^2$ loss, we prove that the ...

We study the problem of high-dimensional covariance estimation under the constraint that the partial correlations are nonnegative. The sign constraints dramatically simplify estimation: the Gaussian...

We develop a technique for establishing lower bounds on the sample complexity of Least Squares (or, Empirical Risk Minimization) for large classes of functions. As an application, we settle an open ...

Max-affine regression refers to a model where the unknown regression function is modeled as a maximum of $k$ unknown affine functions for a fixed $k \geq 1$. This generalizes linear regression and (...

We study the adaptation properties of the multivariate log-concave maximum likelihood estimator over three subclasses of log-concave densities. The first consists of densities with polyhedral suppor...

The Grenander estimator is a well-studied procedure for univariate nonparametric density estimation. It is usually defined as the Maximum Likelihood Estimator (MLE) over the class of all non-increasin...

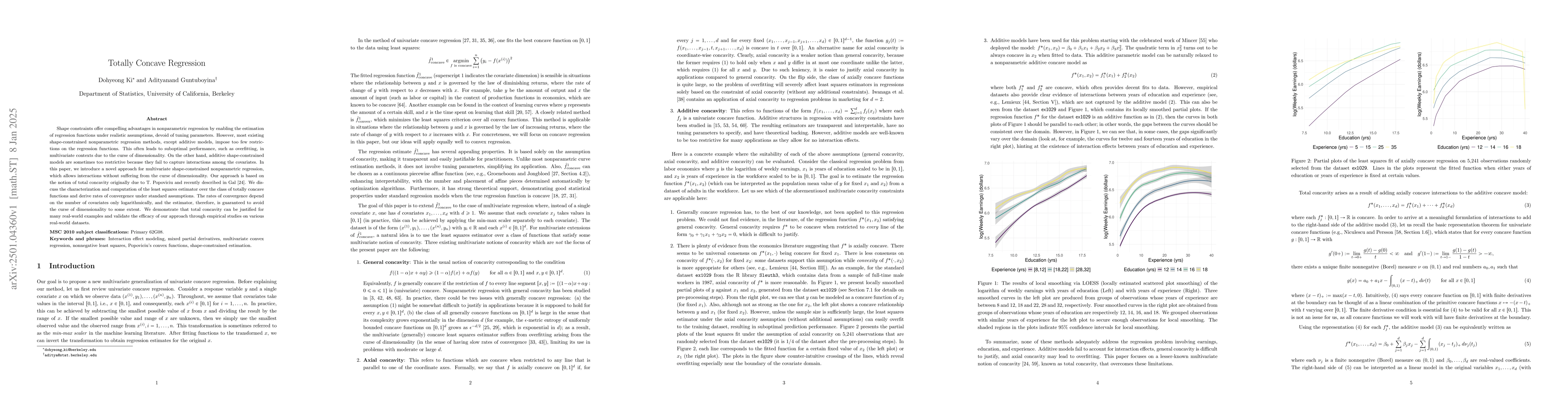

Shape constraints offer compelling advantages in nonparametric regression by enabling the estimation of regression functions under realistic assumptions, devoid of tuning parameters. However, most exi...

This paper establishes a rigorous theoretical foundation for the function class implicitly learned by XGBoost, bridging the gap between its empirical success and our theoretical understanding. We intr...

In this work, we investigate Gaussian Mixture Models ({\it abbrv} GMM) and the related problem of non parametric maximum likelihood estimation ({\it abbrv} NPMLE) from the perspective of statistical m...