Academic Profile

Statistics

Similar Authors

Papers on arXiv

Given an unconditional diffusion model $\pi(x, y)$, using it to perform conditional simulation $\pi(x \mid y)$ is still largely an open question and is typically achieved by learning conditional dri...

BlackJAX is a library implementing sampling and variational inference algorithms commonly used in Bayesian computation. It is designed for ease of use, speed, and modularity by taking a functional a...

In this paper, we propose a novel approach to Bayesian experimental design for non-exchangeable data that formulates it as risk-sensitive policy optimization. We develop the Inside-Out SMC$^2$ algor...

State-of-the-art methods for Bayesian inference in state-space models are (a) conditional sequential Monte Carlo (CSMC) algorithms; (b) sophisticated 'classical' MCMC algorithms like MALA, or mGRAD ...

Probabilistic ordinary differential equation (ODE) solvers have been introduced over the past decade as uncertainty-aware numerical integrators. They typically proceed by assuming a functional prior...

Stochastic optimal control of dynamical systems is a crucial challenge in sequential decision-making. Recently, control-as-inference approaches have had considerable success, providing a viable risk...

Probabilistic numerical solvers for ordinary differential equations (ODEs) treat the numerical simulation of dynamical systems as problems of Bayesian state estimation. Aside from producing posterio...

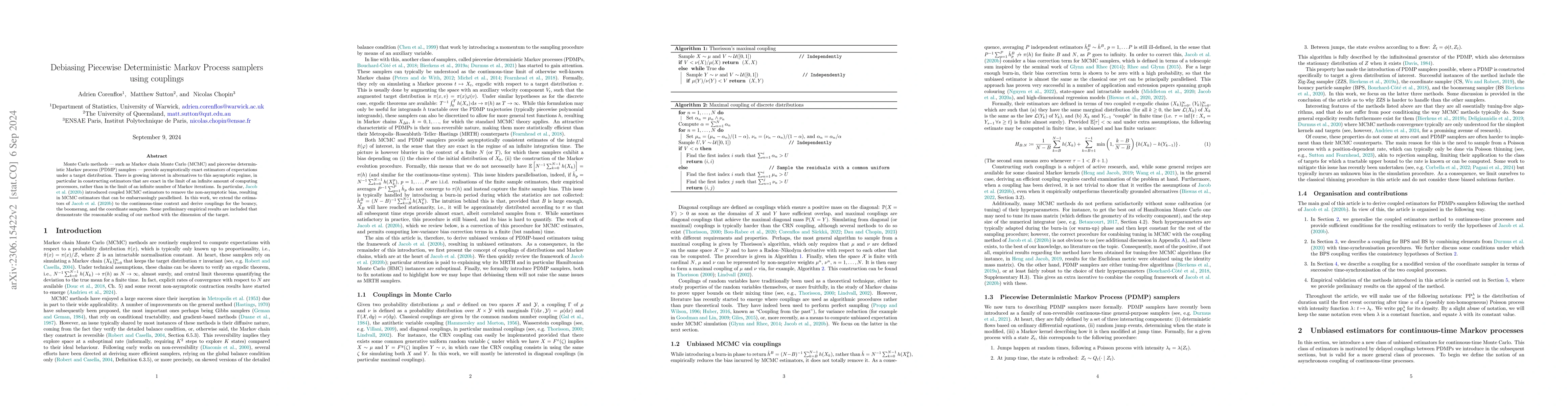

Monte Carlo methods - such as Markov chain Monte Carlo (MCMC) and piecewise deterministic Markov process (PDMP) samplers - provide asymptotically exact estimators of expectations under a target dist...

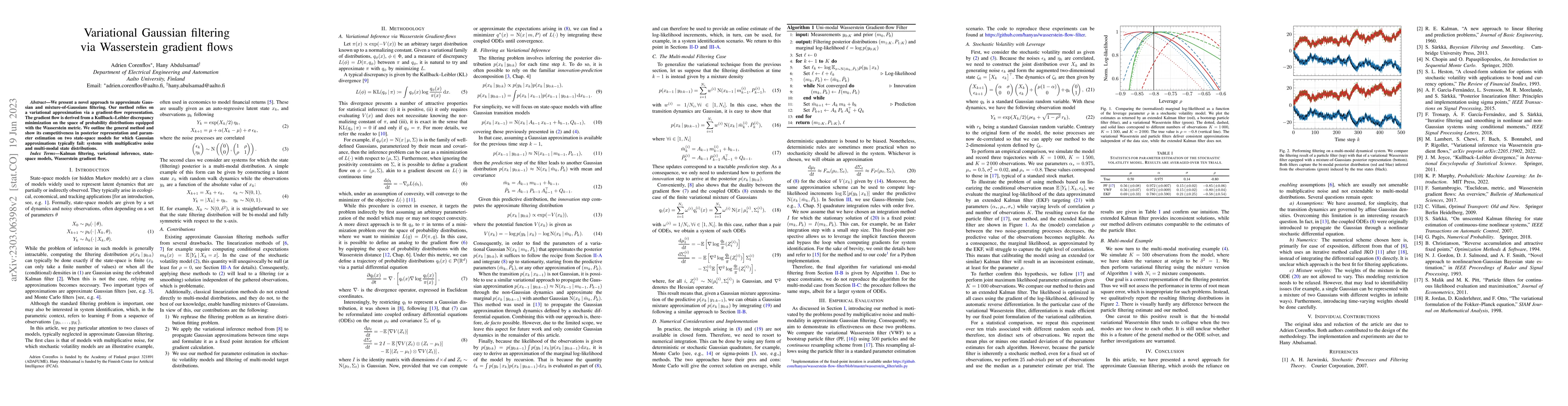

We present a novel approach to approximate Gaussian and mixture-of-Gaussians filtering. Our method relies on a variational approximation via a gradient-flow representation. The gradient flow is deri...

We introduce two new classes of exact Markov chain Monte Carlo (MCMC) samplers for inference in latent dynamical models. The first one, which we coin auxiliary Kalman samplers, relies on finding a l...

In this article, we introduce parallel-in-time methods for state and parameter estimation in general nonlinear non-Gaussian state-space models using the statistical linear regression and the iterate...

Particle smoothers are SMC (Sequential Monte Carlo) algorithms designed to approximate the joint distribution of the states given observations from a state-space model. We propose dSMC (de-Sequentia...

We propose a coupled rejection-sampling method for sampling from couplings of arbitrary distributions. The method relies on accepting or rejecting coupled samples coming from dominating marginals. C...

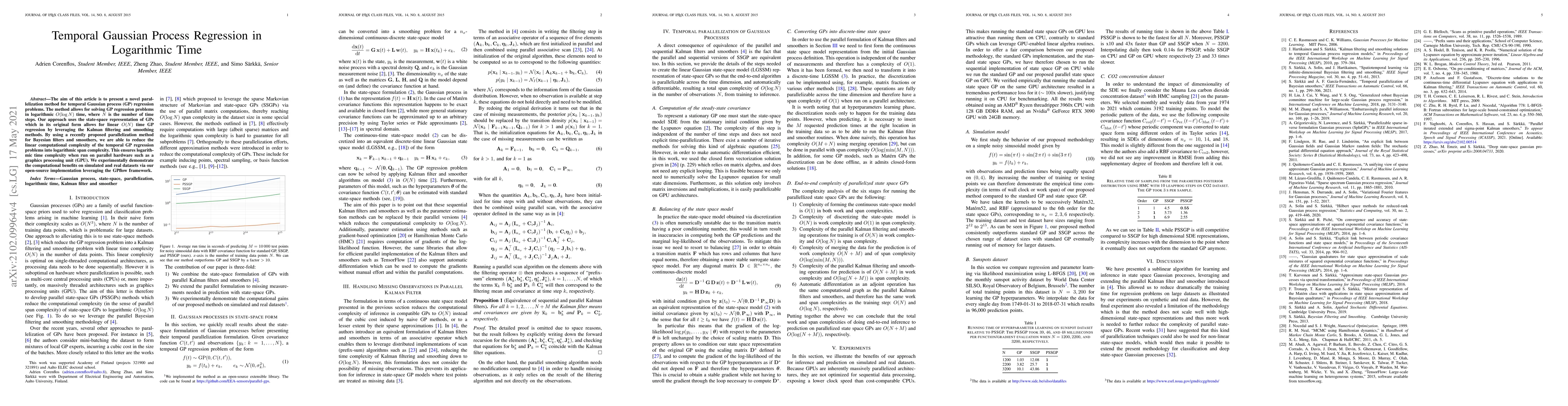

The aim of this article is to present a novel parallelization method for temporal Gaussian process (GP) regression problems. The method allows for solving GP regression problems in logarithmic O(log...

The problem of Bayesian filtering and smoothing in nonlinear models with additive noise is an active area of research. Classical Taylor series as well as more recent sigma-point based methods are tw...

This paper introduces the Inside-Out Nested Particle Filter (IO-NPF), a novel, fully recursive, algorithm for amortized sequential Bayesian experimental design in the non-exchangeable setting. We fram...

Exact parameter and trajectory inference in state-space models is typically achieved by one of two methods: particle marginal Metropolis-Hastings (PMMH) or particle Gibbs (PGibbs). PMMH is a pseudo-ma...

A long-standing gap exists between the theoretical analysis of Markov chain Monte Carlo convergence, which is often based on statistical divergences, and the diagnostics used in practice. We introduce...

We address the brittleness of Bayesian experimental design under model misspecification by formulating the problem as a max--min game between the experimenter and an adversarial nature subject to info...

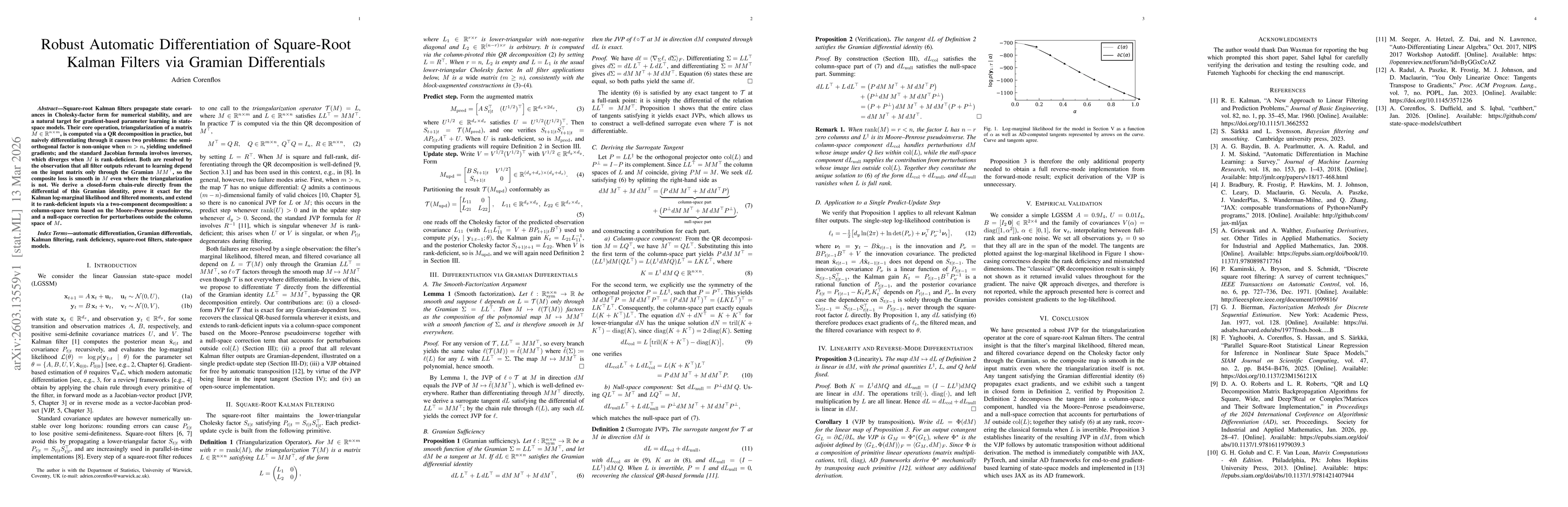

Square-root Kalman filters propagate state covariances in Cholesky-factor form for numerical stability, and are a natural target for gradient-based parameter learning in state-space models. Their core...

We study the contraction in Wasserstein distance of the coordinate ascent variational inference algorithm. This is shown to hold under a transport-information inequality at the fixed points and a func...