Academic Profile

Statistics

Similar Authors

Papers on arXiv

One the one hand, rough volatility has been shown to provide a consistent framework to capture the properties of stock price dynamics both under the historical measure and for pricing purposes. On t...

We provide explicit small-time formulae for the at-the-money implied volatility, skew and curvature in a large class of models, including rough volatility models and their multi-factor versions. Our...

We develop a new analysis for portfolio optimisation with options, tackling the three fundamental issues with this problem: asymmetric options' distributions, high dimensionality and dependence stru...

The problem of rapid and automated detection of distinct market regimes is a topic of great interest to financial mathematicians and practitioners alike. In this paper, we outline an unsupervised le...

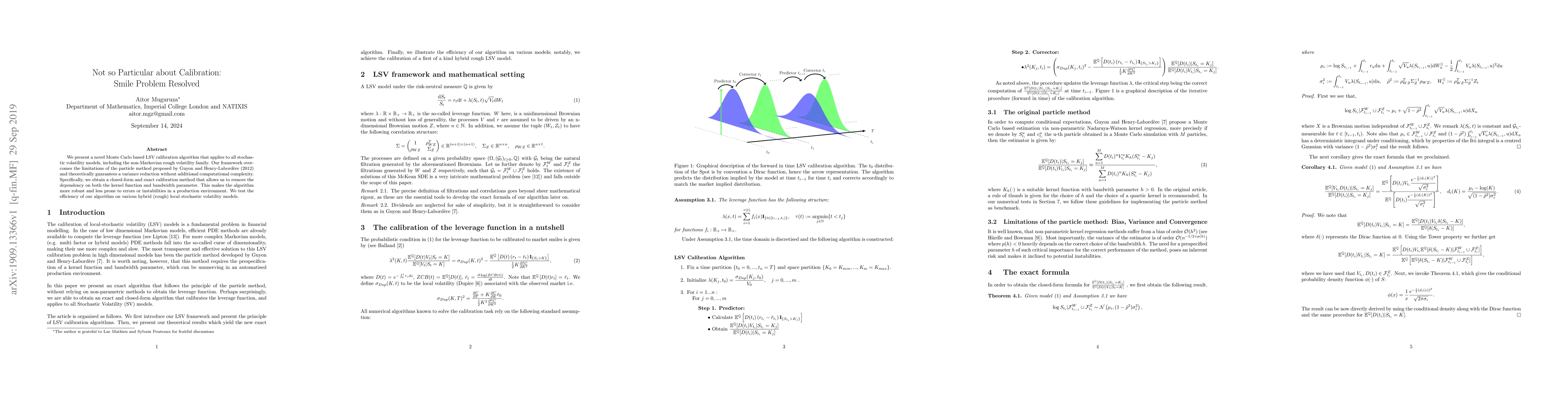

We present a novel Monte Carlo based LSV calibration algorithm that applies to all stochastic volatility models, including the non-Markovian rough volatility family. Our framework overcomes the limi...

Techniques from deep learning play a more and more important role for the important task of calibration of financial models. The pioneering paper by Hernandez [Risk, 2017] was a catalyst for resurfa...

We present a neural network based calibration method that performs the calibration task within a few milliseconds for the full implied volatility surface. The framework is consistently applicable th...

The non-Markovian nature of rough volatility processes makes Monte Carlo methods challenging and it is in fact a major challenge to develop fast and accurate simulation algorithms. We provide an eff...