Academic Profile

Statistics

Similar Authors

Papers on arXiv

Importance weighting is a general way to adjust Monte Carlo integration to account for draws from the wrong distribution, but the resulting estimate can be highly variable when the importance ratios...

Throughout the different phases of a drug development program, randomized trials are used to establish the tolerability, safety, and efficacy of a candidate drug. At each stage one aims to optimize ...

We present the ARR2 prior, a joint prior over the auto-regressive components in Bayesian time-series models and their induced $R^2$. Compared to other priors designed for times-series models, the AR...

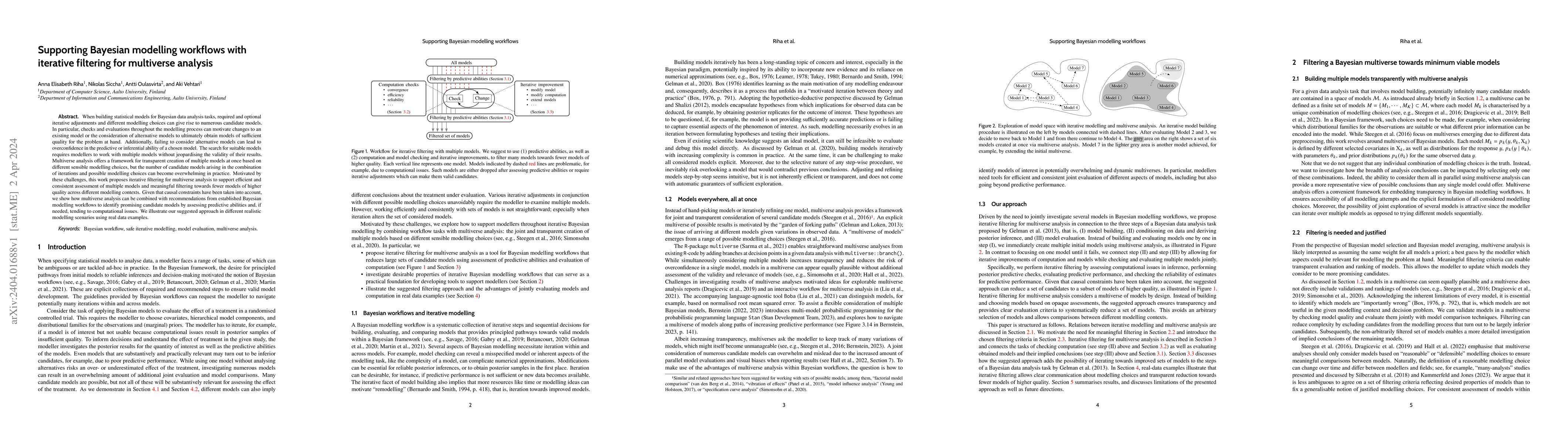

When building statistical models for Bayesian data analysis tasks, required and optional iterative adjustments and different modelling choices can give rise to numerous candidate models. In particul...

Generalization to new samples is a fundamental rationale for statistical modeling. For this purpose, model validation is particularly important, but recent work in survey inference has suggested tha...

Brute force cross-validation (CV) is a method for predictive assessment and model selection that is general and applicable to a wide range of Bayesian models. Naive or `brute force' CV approaches ar...

Model selection aims to identify a sufficiently well performing model that is possibly simpler than the most complex model among a pool of candidates. However, the decision-making process itself can...

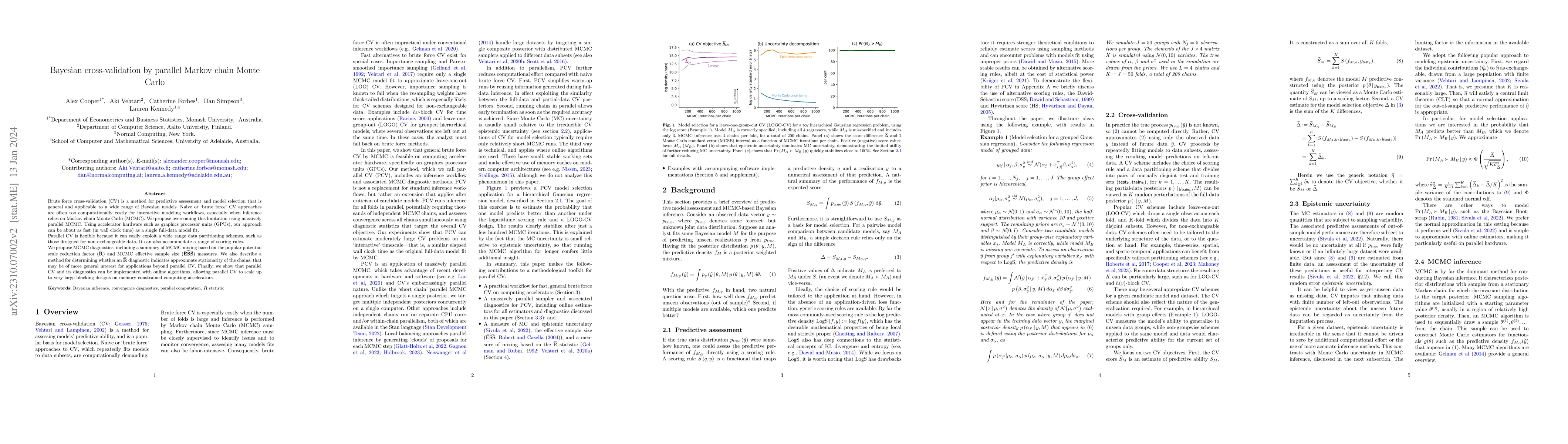

Bayesian cross-validation (CV) is a popular method for predictive model assessment that is simple to implement and broadly applicable. A wide range of CV schemes is available for time series applica...

The projection predictive variable selection is a decision-theoretically justified Bayesian variable selection approach achieving an outstanding trade-off between predictive performance and sparsity...

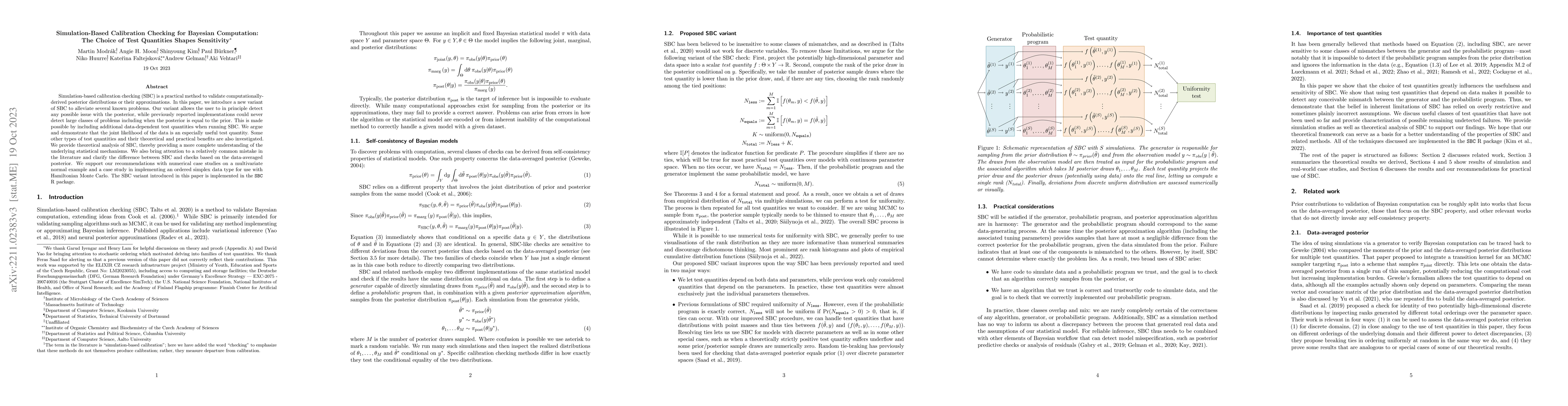

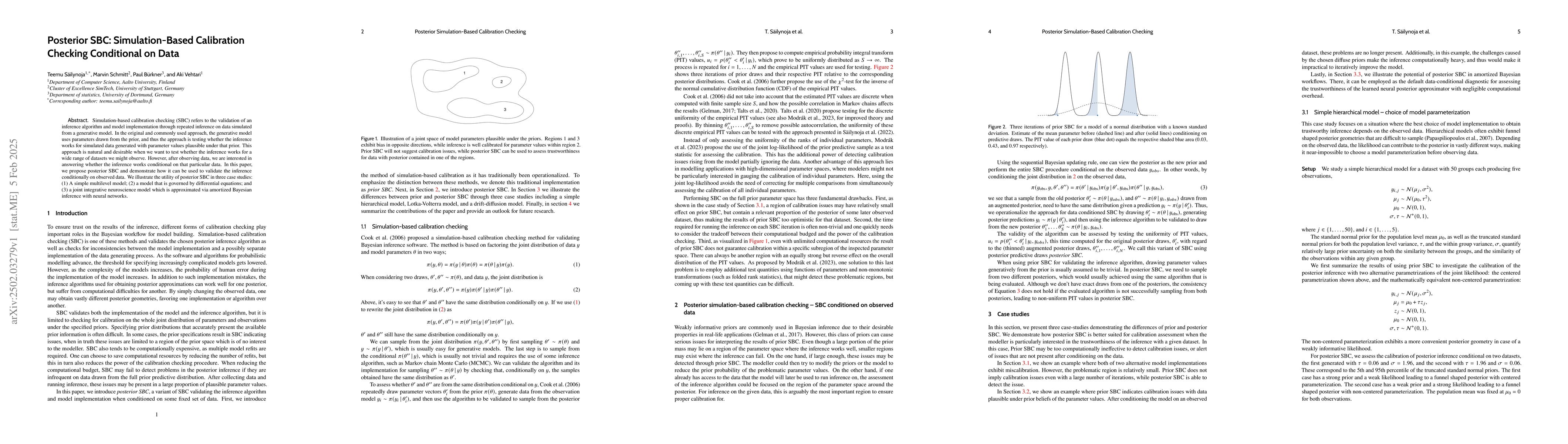

Simulation-based calibration checking (SBC) is a practical method to validate computationally-derived posterior distributions or their approximations. In this paper, we introduce a new variant of SB...

Auto-regressive moving-average (ARMA) models are ubiquitous forecasting tools. Parsimony in such models is highly valued for their interpretability and computational tractability, and as such the id...

Statistical models can involve implicitly defined quantities, such as solutions to nonlinear ordinary differential equations (ODEs), that unavoidably need to be numerically approximated in order to ...

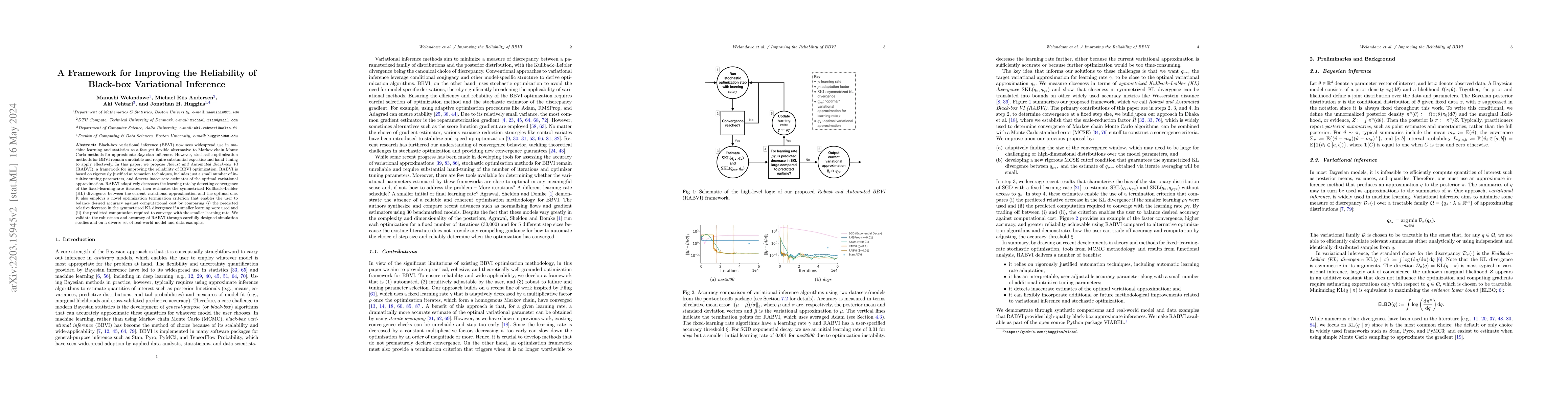

Black-box variational inference (BBVI) now sees widespread use in machine learning and statistics as a fast yet flexible alternative to Markov chain Monte Carlo methods for approximate Bayesian infe...

Specification of the prior distribution for a Bayesian model is a central part of the Bayesian workflow for data analysis, but it is often difficult even for statistical experts. In principle, prior...

Recent developments in parallel Markov chain Monte Carlo (MCMC) algorithms allow us to run thousands of chains almost as quickly as a single chain, using hardware accelerators such as GPUs. While ea...

We describe a class of algorithms for evaluating posterior moments of certain Bayesian linear regression models with a normal likelihood and a normal prior on the regression coefficients. The propos...

This paper considers reparameterization invariant Bayesian point estimates and credible regions of model parameters for scientific inference and communication. The effect of intrinsic loss function ...

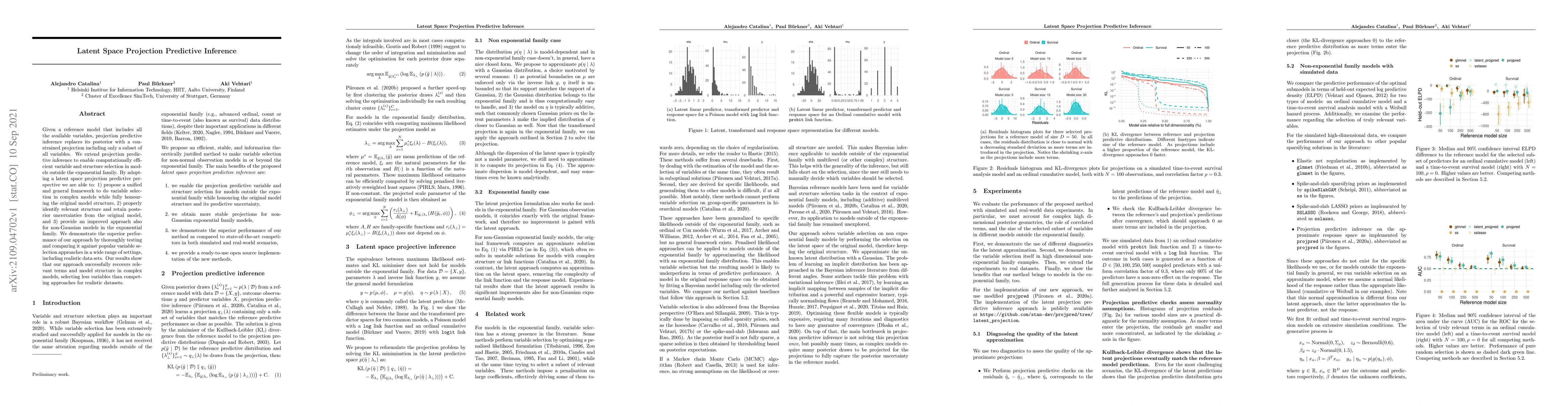

Given a reference model that includes all the available variables, projection predictive inference replaces its posterior with a constrained projection including only a subset of all variables. We e...

We propose Pathfinder, a variational method for approximately sampling from differentiable log densities. Starting from a random initialization, Pathfinder locates normal approximations to the targe...

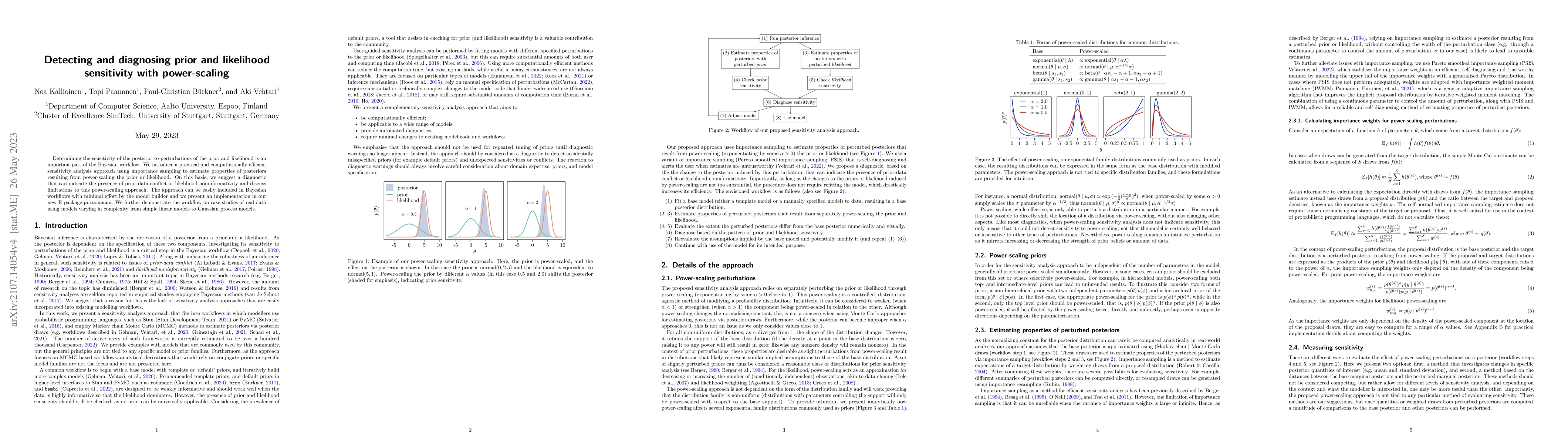

Determining the sensitivity of the posterior to perturbations of the prior and likelihood is an important part of the Bayesian workflow. We introduce a practical and computationally efficient sensit...

In some scientific fields, it is common to have certain variables of interest that are of particular importance and for which there are many studies indicating a relationship with different explanat...

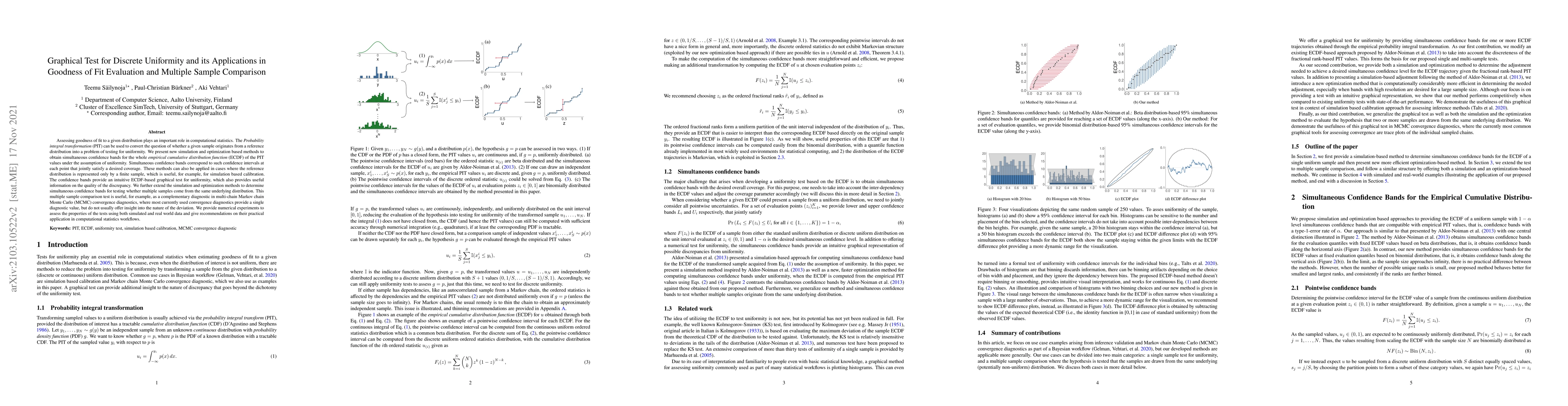

Assessing goodness of fit to a given distribution plays an important role in computational statistics. The Probability integral transformation (PIT) can be used to convert the question of whether a ...

Current black-box variational inference (BBVI) methods require the user to make numerous design choices -- such as the selection of variational objective and approximating family -- yet there is lit...

Stacking is a widely used model averaging technique that asymptotically yields optimal predictions among linear averages. We show that stacking is most effective when model predictive performance is...

We review the most important statistical ideas of the past half century, which we categorize as: counterfactual causal inference, bootstrapping and simulation-based inference, overparameterized mode...

We describe a numerical scheme for evaluating the posterior moments of Bayesian linear regression models with partial pooling of the coefficients. The principal analytical tool of the evaluation is ...

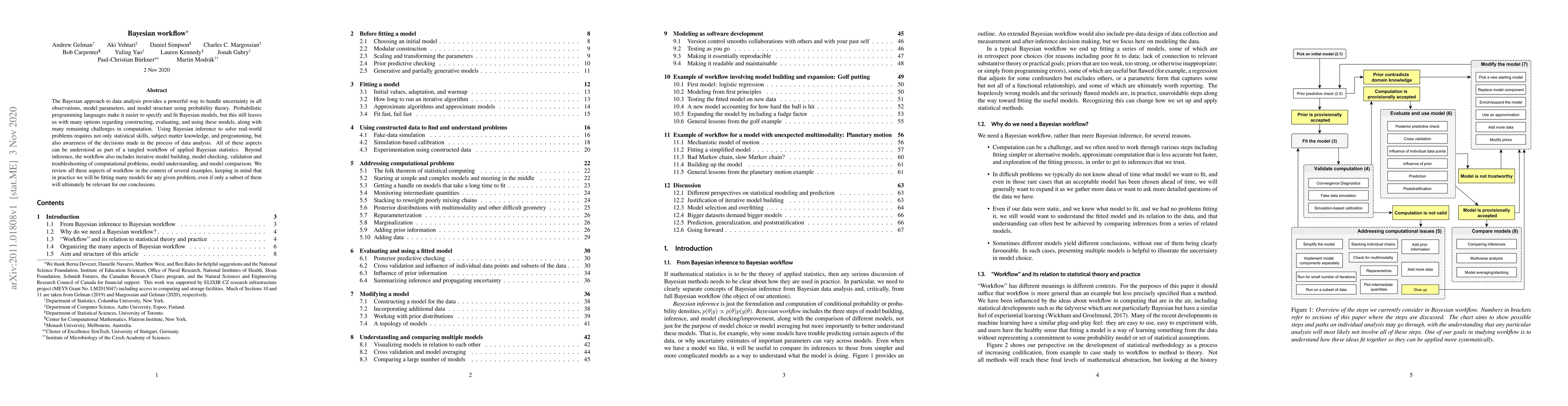

The Bayesian approach to data analysis provides a powerful way to handle uncertainty in all observations, model parameters, and model structure using probability theory. Probabilistic programming la...

Projection predictive inference is a decision theoretic Bayesian approach that decouples model estimation from decision making. Given a reference model previously built including all variables prese...

We consider the problem of fitting variational posterior approximations using stochastic optimization methods. The performance of these approximations depends on (1) how well the variational family ...

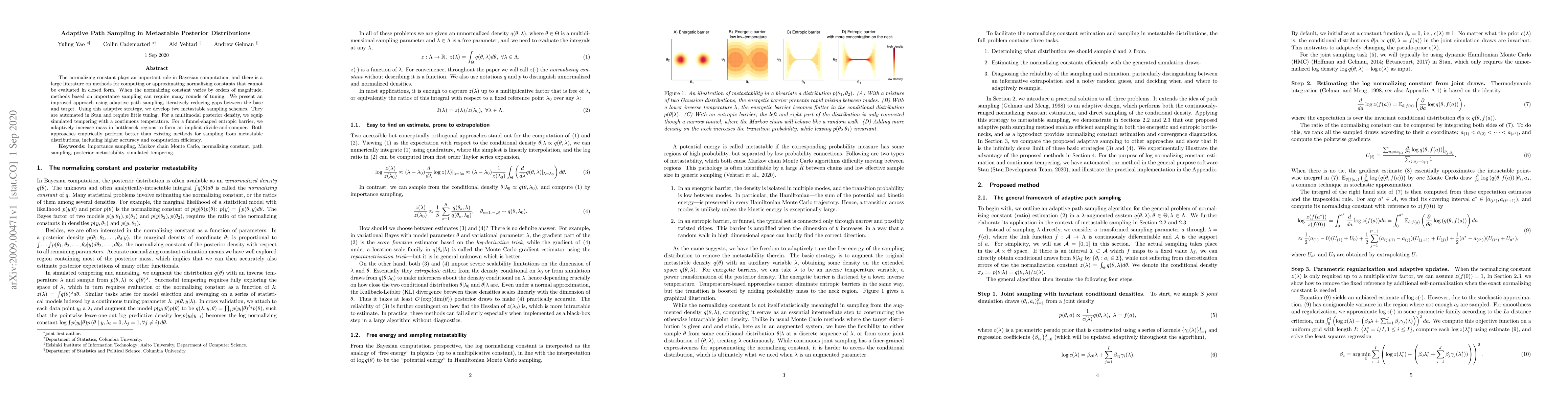

The normalizing constant plays an important role in Bayesian computation, and there is a large literature on methods for computing or approximating normalizing constants that cannot be evaluated in ...

When evaluating and comparing models using leave-one-out cross-validation (LOO-CV), the uncertainty of the estimate is typically assessed using the variance of the sampling distribution. Considering...

Leave-one-out cross-validation (LOO-CV) is a popular method for comparing Bayesian models based on their estimated predictive performance on new, unseen, data. As leave-one-out cross-validation is b...

When working with multimodal Bayesian posterior distributions, Markov chain Monte Carlo (MCMC) algorithms have difficulty moving between modes, and default variational or mode-based approximate infe...

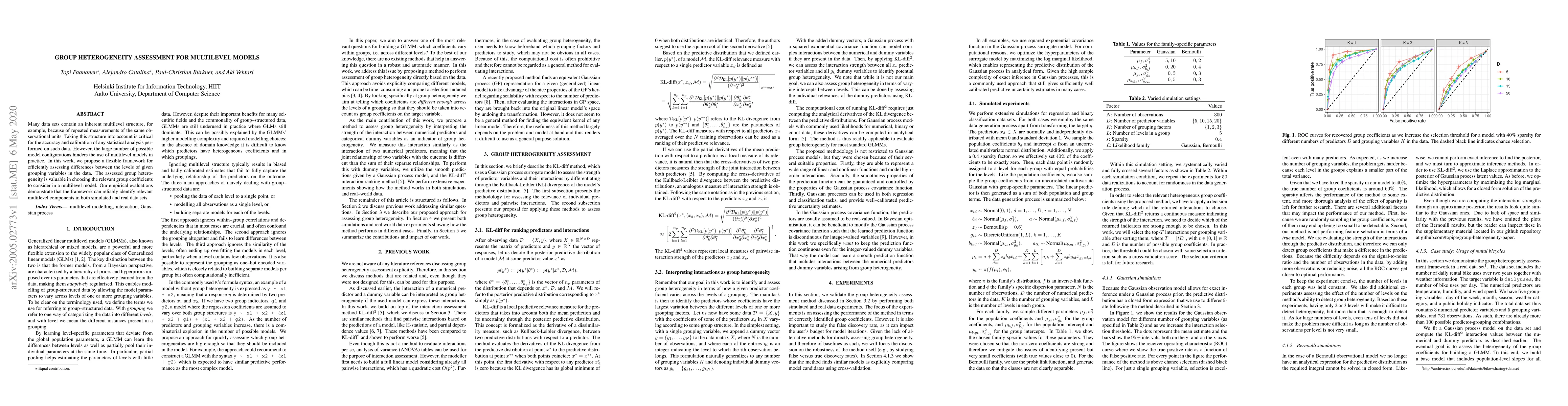

Many data sets contain an inherent multilevel structure, for example, because of repeated measurements of the same observational units. Taking this structure into account is critical for the accurac...

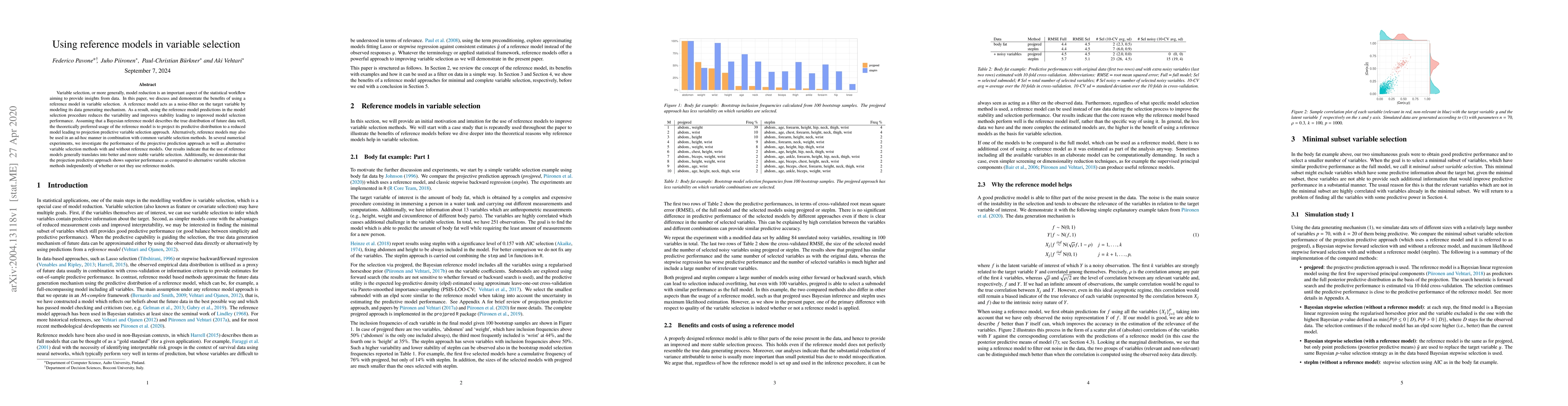

Variable selection, or more generally, model reduction is an important aspect of the statistical workflow aiming to provide insights from data. In this paper, we discuss and demonstrate the benefits...

Gaussian processes are powerful non-parametric probabilistic models for stochastic functions. However, the direct implementation entails a complexity that is computationally intractable when the num...

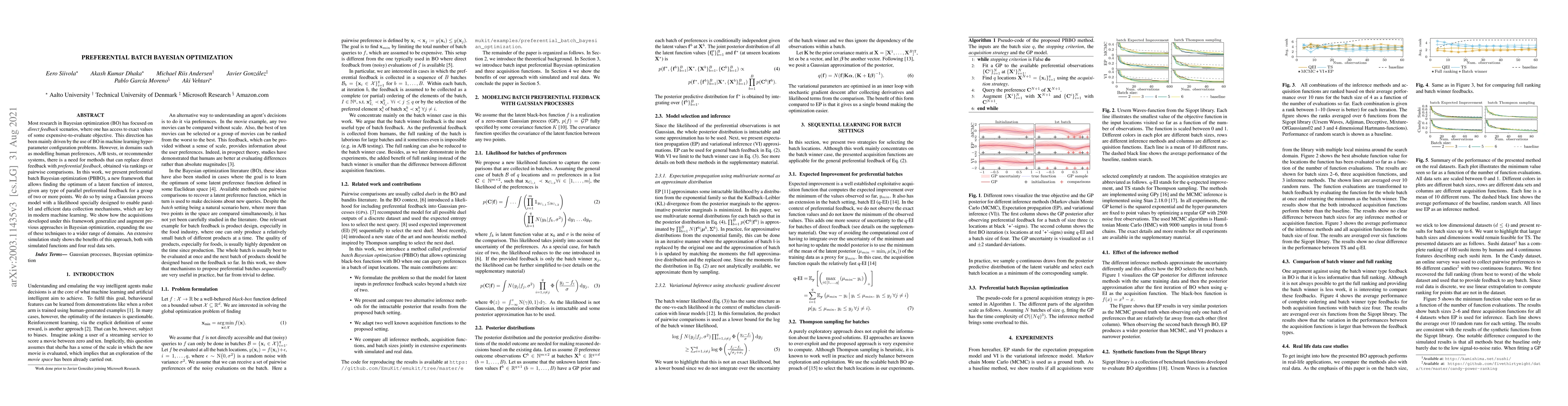

Most research in Bayesian optimization (BO) has focused on \emph{direct feedback} scenarios, where one has access to exact values of some expensive-to-evaluate objective. This direction has been mai...

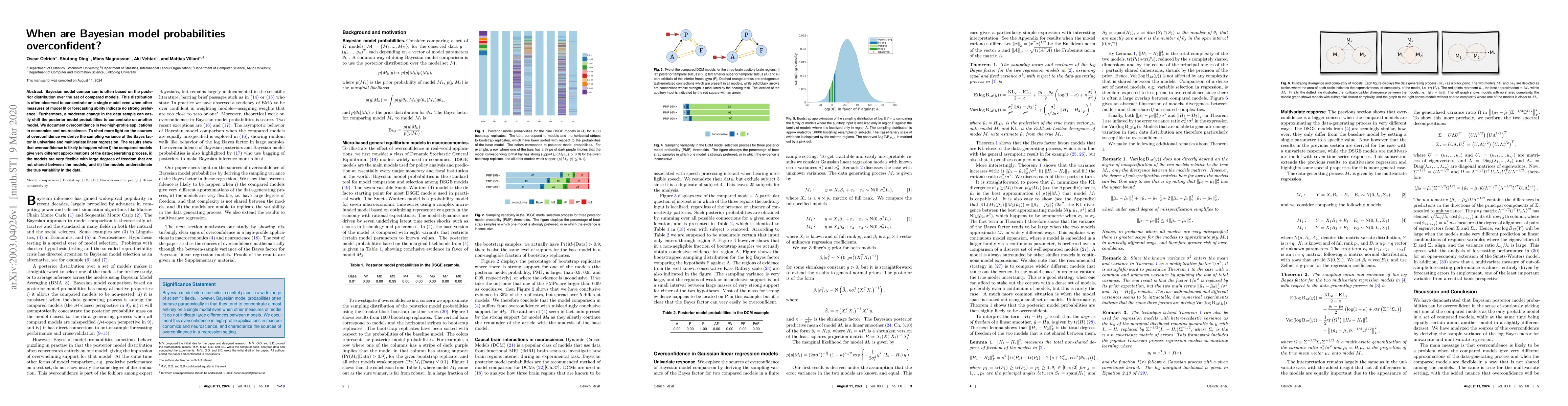

Bayesian model comparison is often based on the posterior distribution over the set of compared models. This distribution is often observed to concentrate on a single model even when other measures ...

Recently, new methods for model assessment, based on subsampling and posterior approximations, have been proposed for scaling leave-one-out cross-validation (LOO) to large datasets. Although these m...

Longitudinal study designs are indispensable for studying disease progression. Inferring covariate effects from longitudinal data, however, requires interpretable methods that can model complicated ...

Microfading Spectrometry (MFS) is a method for assessing light sensitivity color (spectral) variations of cultural heritage objects. The MFS technique provides measurements of the surface under stud...

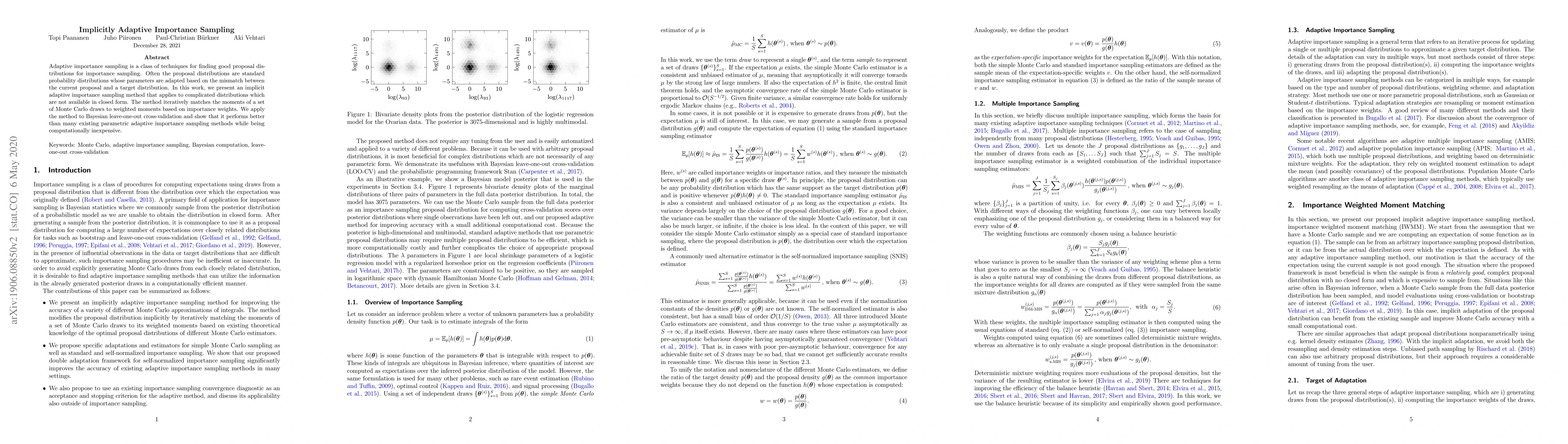

Adaptive importance sampling is a class of techniques for finding good proposal distributions for importance sampling. Often the proposal distributions are standard probability distributions whose p...

We present a selection criterion for the Euclidean metric adapted during warmup in a Hamiltonian Monte Carlo sampler that makes it possible for a sampler to automatically pick the metric based on th...

Model inference, such as model comparison, model checking, and model selection, is an important part of model development. Leave-one-out cross-validation (LOO) is a general approach for assessing th...

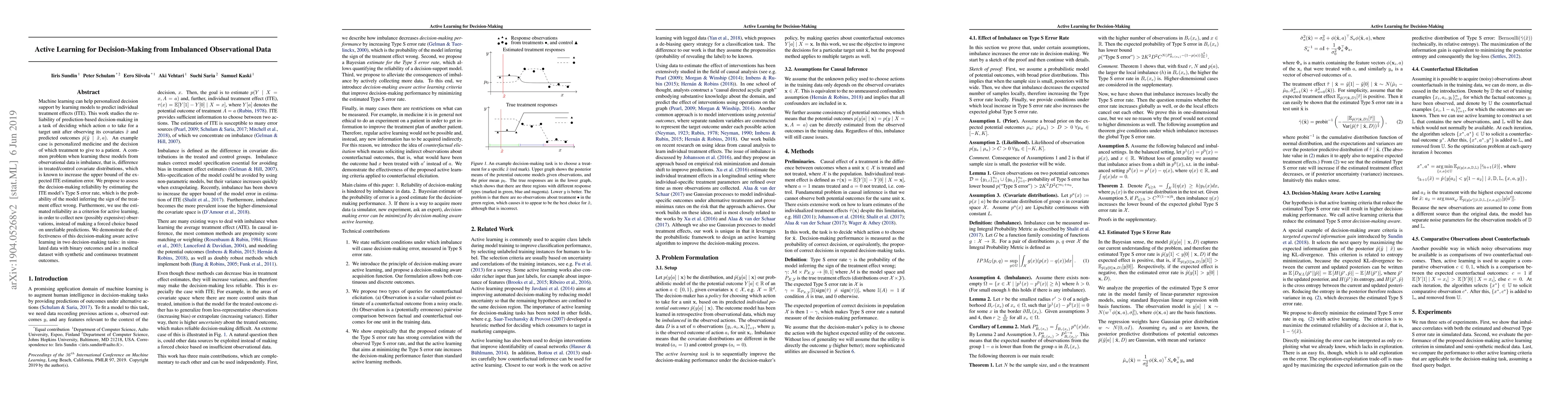

Machine learning can help personalized decision support by learning models to predict individual treatment effects (ITE). This work studies the reliability of prediction-based decision-making in a t...

This paper discusses predictive inference and feature selection for generalized linear models with scarce but high-dimensional data. We argue that in many cases one can benefit from a decision theor...

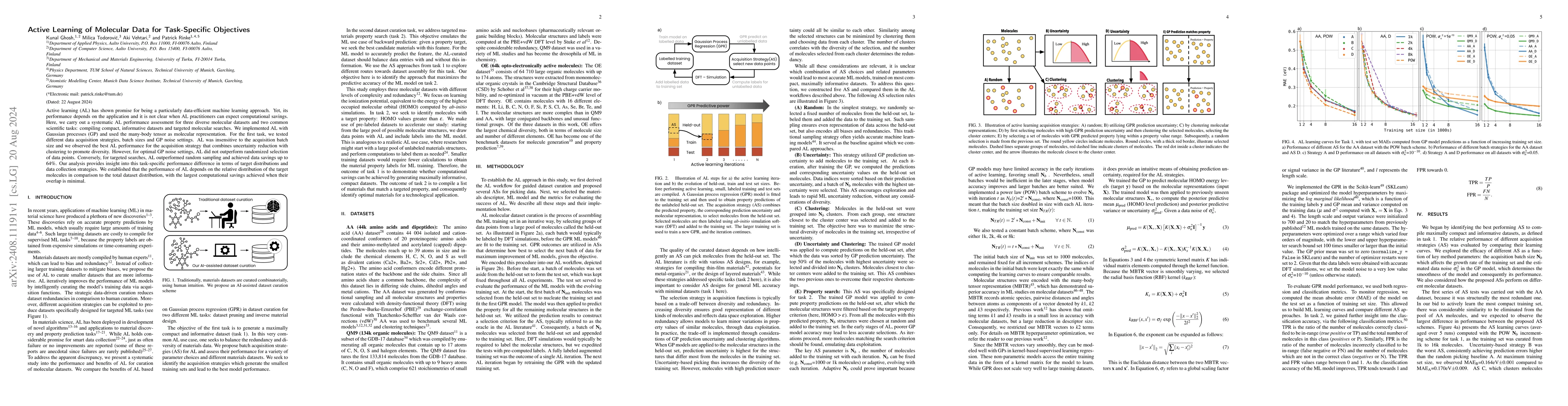

Active learning (AL) has shown promise for being a particularly data-efficient machine learning approach. Yet, its performance depends on the application and it is not clear when AL practitioners can ...

Bayesian inference often faces a trade-off between computational speed and sampling accuracy. We propose an adaptive workflow that integrates rapid amortized inference with gold-standard MCMC techniqu...

The generality and robustness of inference algorithms is critical to the success of widely used probabilistic programming languages such as Stan, PyMC, Pyro, and Turing.jl. When designing a new genera...

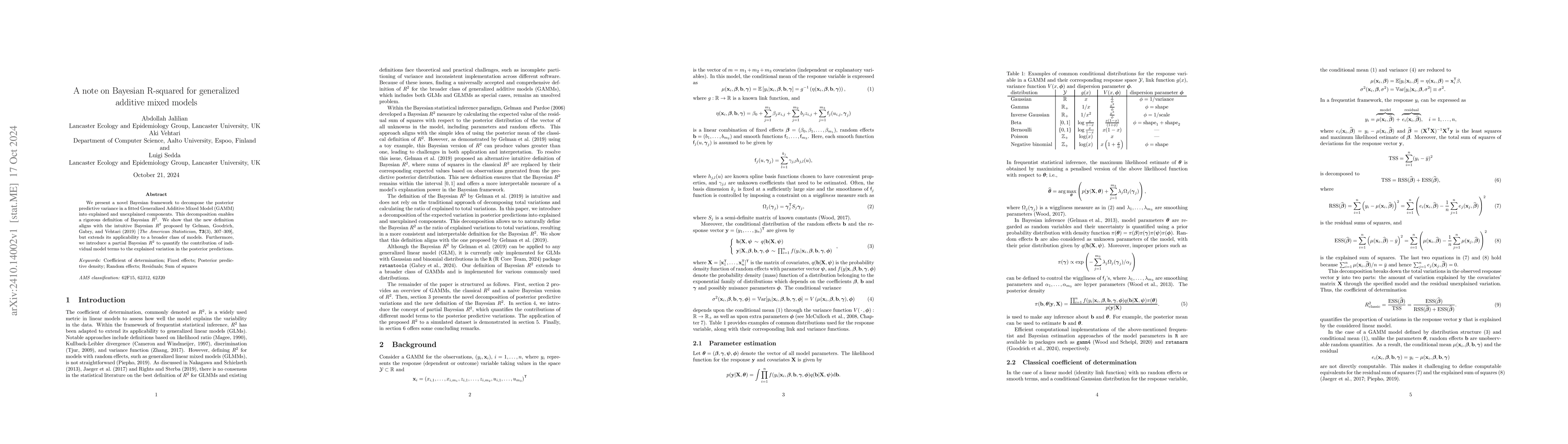

We present a novel Bayesian framework to decompose the posterior predictive variance in a fitted Generalized Additive Mixed Model (GAMM) into explained and unexplained components. This decomposition e...

Simulation-based calibration checking (SBC) refers to the validation of an inference algorithm and model implementation through repeated inference on data simulated from a generative model. In the ori...

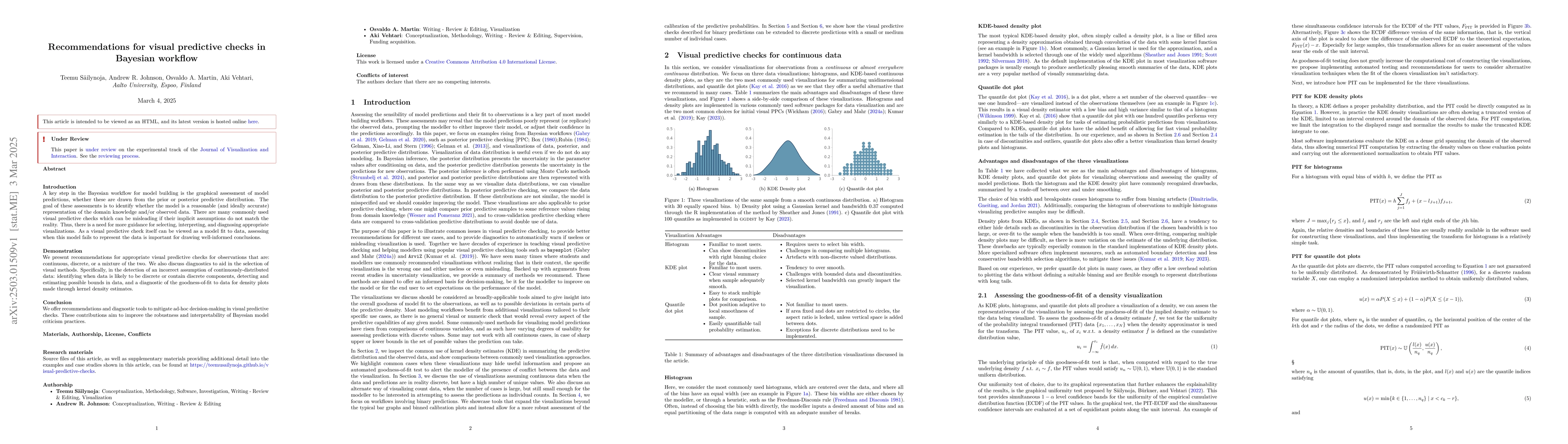

A key step in the Bayesian workflow for model building is the graphical assessment of model predictions, whether these are drawn from the prior or posterior predictive distribution. The goal of these ...

Cross-validation (CV) is a widely-used method of predictive assessment based on repeated model fits to different subsets of the available data. CV is applicable in a wide range of statistical settings...

We introduce the Group-R2 decomposition prior, a hierarchical shrinkage prior that extends R2-based priors to structured regression settings with known groups of predictors. By decomposing the prior d...

In Bayesian statistics, the marginal likelihood is used for model selection and averaging, yet it is often challenging to compute accurately for complex models. Approaches such as bridge sampling, whi...

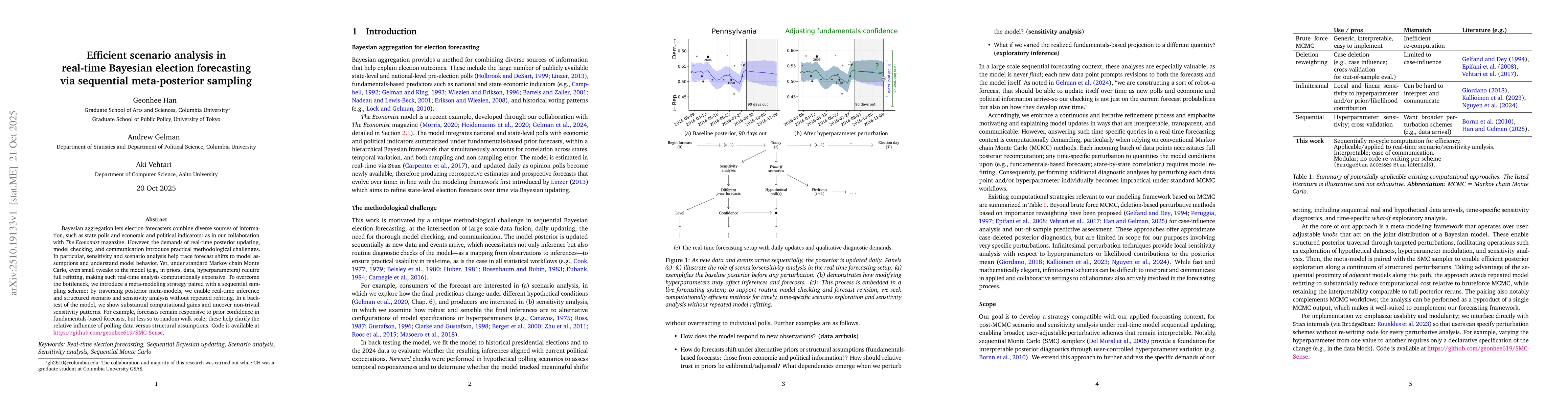

Bayesian aggregation lets election forecasters combine diverse sources of information, such as state polls and economic and political indicators: as in our collaboration with The Economist magazine. H...

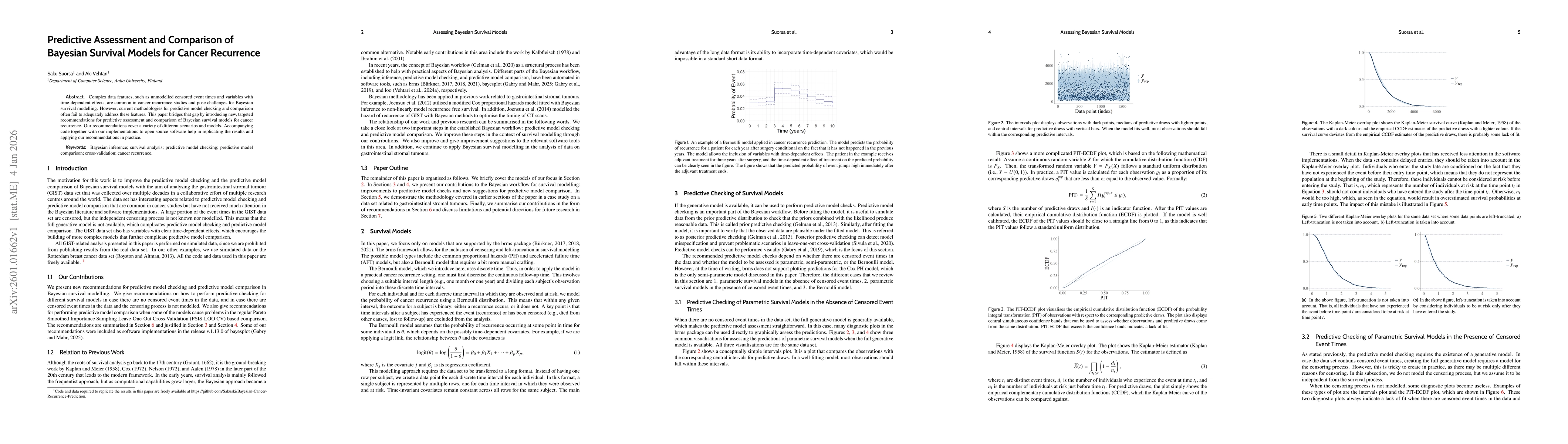

Complex data features, such as unmodelled censored event times and variables with time-dependent effects, are common in cancer recurrence studies and pose challenges for Bayesian survival modelling. H...

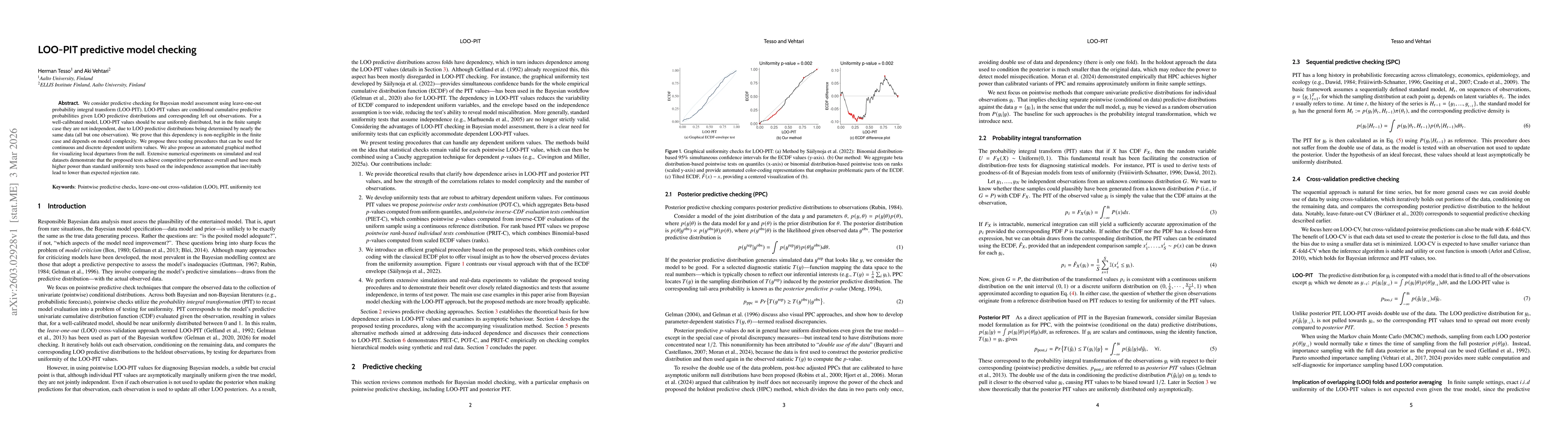

We consider predictive checking for Bayesian model assessment using leave-one-out probability integral transform (LOO-PIT). LOO-PIT values are conditional cumulative predictive probabilities given LOO...

Bayesian modelling workflows often consider multiple candidate models of varying complexity. Model selection is commonly used to navigate potential trade-offs between model complexity and generalisabi...