Academic Profile

Statistics

Similar Authors

Papers on arXiv

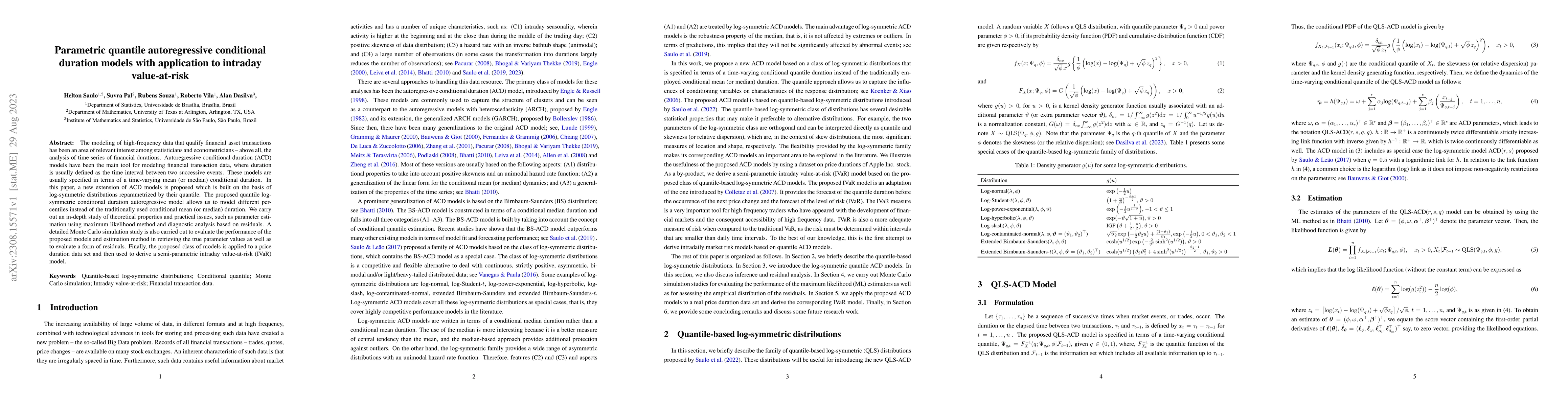

The modeling of high-frequency data that qualify financial asset transactions has been an area of relevant interest among statisticians and econometricians -- above all, the analysis of time series ...

Parametric autoregressive moving average models with exogenous terms (ARMAX) have been widely used in the literature. Usually, these models consider a conditional mean or median dynamics, which limi...

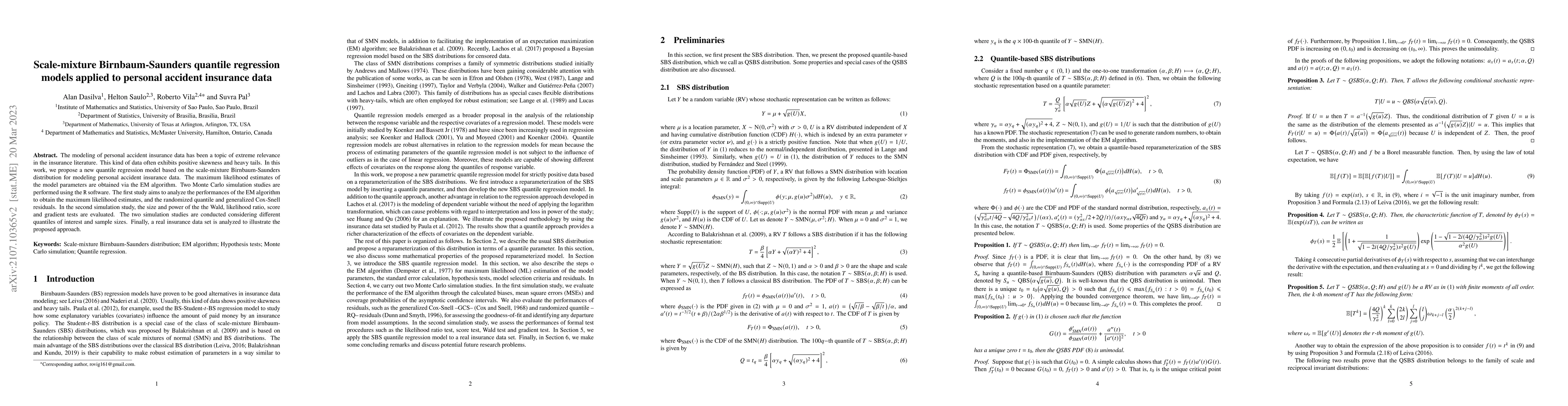

The modeling of personal accident insurance data has been a topic of extreme relevance in the insurance literature. This kind of data often exhibits positive skewness and heavy tails. In this work, ...

Regression models based on the log-symmetric family of distributions are particularly useful when the response is strictly positive and asymmetric. In this paper, we propose a class of quantile regr...