Academic Profile

Statistics

Similar Authors

Papers on arXiv

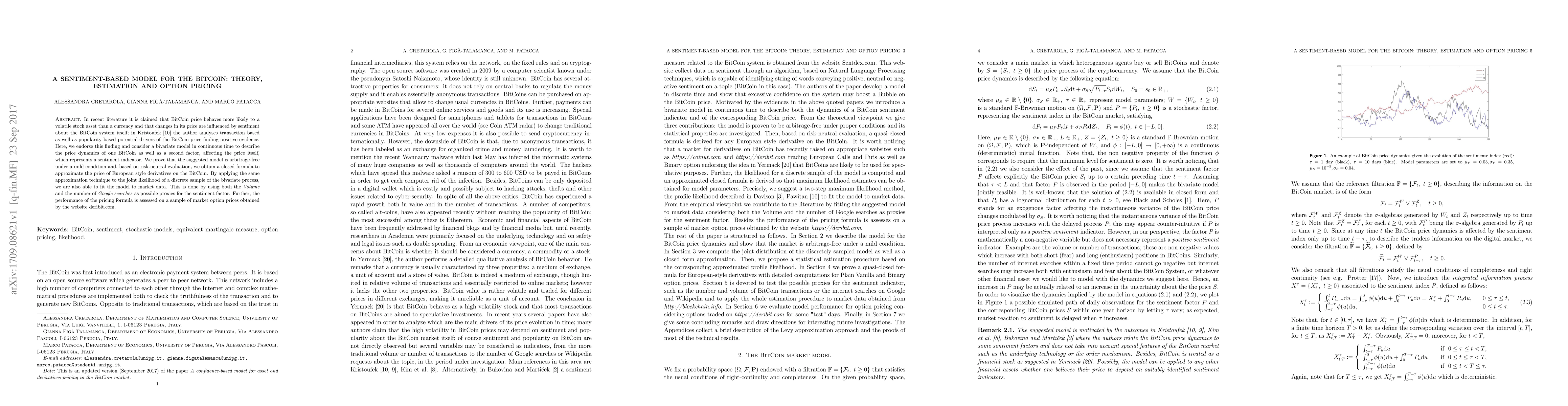

We endorse the idea, suggested in recent literature, that BitCoin prices are influenced by sentiment and confidence about the underlying technology; as a consequence, an excitement about the BitCoin...

We investigate the optimal reinsurance problem in the risk model with jump clustering features introduced in [7]. This modeling framework is inspired by the concept initially proposed in [15], combi...

In this paper we study exponential utility indifference pricing of pure endowment policies in a stochastic-factor model for an insurance company, which can also invest in a financial market. Specifi...

We study the optimal investment and proportional reinsurance problem of an insurance company, whose investment preferences are described via a forward dynamic utility of exponential type in a stocha...

In this paper we study the optimal investment and reinsurance problem of an insurance company whose investment preferences are described via a forward dynamic exponential utility in a regime-switchi...

We study optimal proportional reinsurance and investment strategies for an insurance company which experiences both ordinary and catastrophic claims and wishes to maximize the expected exponential u...

In recent literature it is claimed that BitCoin price behaves more likely to a volatile stock asset than a currency and that changes in its price are influenced by sentiment about the BitCoin system...

We investigate an optimal prevention and insurance problem in a general risk setting, where a representative agent is exposed to potential losses. The agent adopts a strategy that combines self-protec...

This paper addresses the existence of nonnegative mild solutions for stochastic evolution inclusions through a weak topology approach. Precisely, the study focuses on stochastic evolution inclusions c...

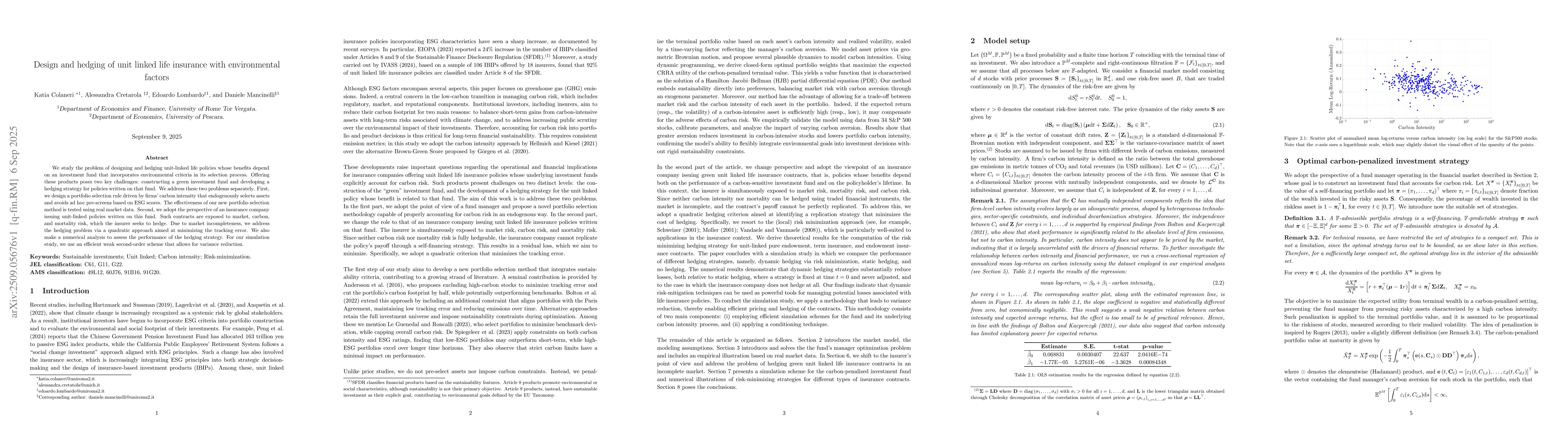

We study the problem of designing and hedging unit-linked life policies whose benefits depend on an investment fund that incorporates environmental criteria in its selection process. Offering these pr...