Academic Profile

Statistics

Similar Authors

Papers on arXiv

The paper analyzes the cryptocurrency ecosystem at both the aggregate and individual levels to understand the factors that impact future volatility. The study uses high-frequency panel data from 202...

This paper introduces SpotV2Net, a multivariate intraday spot volatility forecasting model based on a Graph Attention Network architecture. SpotV2Net represents assets as nodes within a graph and in...

The beekeeping sector has undergone considerable production variations over the past years due to adverse weather conditions, occurring more frequently as climate change progresses. These phenomena ...

In this paper, we analyze the effect of a policy recommendation on the performance of an artificial interbank market. Financial institutions stipulate lending agreements following a public recommend...

Classical portfolio optimization often requires forecasting asset returns and their corresponding variances in spite of the low signal-to-noise ratio provided in the financial markets. Modern deep r...

This paper applies deep reinforcement learning (DRL) to optimize liquidity provisioning in Uniswap v3, a decentralized finance (DeFi) protocol implementing an automated market maker (AMM) model with c...

The key objective of this paper is to develop an empirical model for pricing SPX options that can be simulated over future paths of the SPX. To accomplish this, we formulate and rigorously evaluate se...

We propose Mixed-Panels-Transformer Encoder (MPTE), a novel framework for estimating factor models in panel datasets with mixed frequencies and nonlinear signals. Traditional factor models rely on lin...

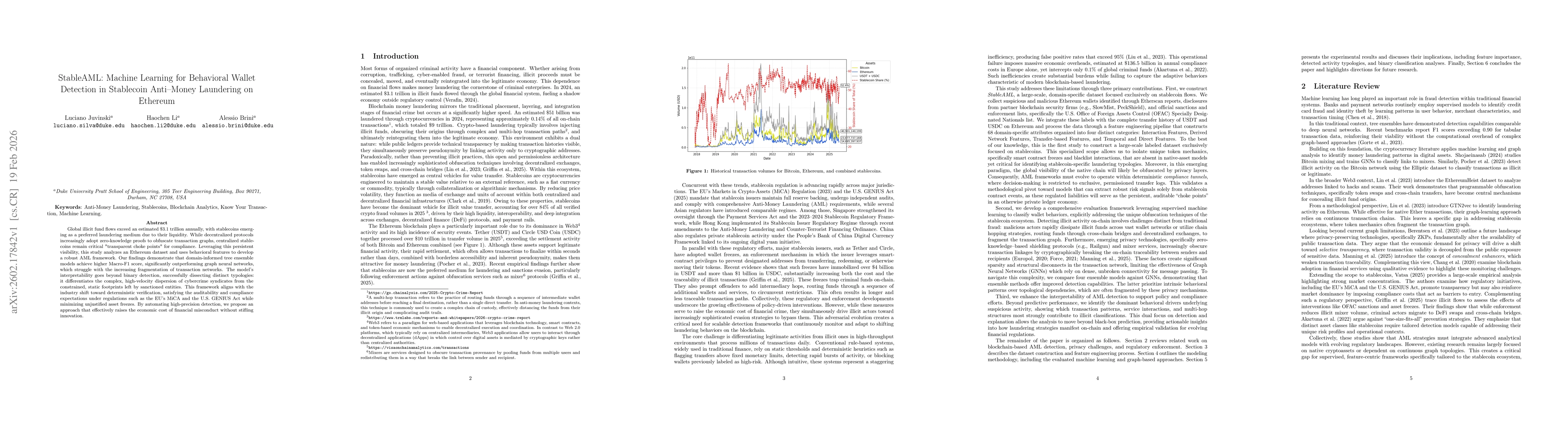

Global illicit fund flows exceed an estimated $3.1 trillion annually, with stablecoins emerging as a preferred laundering medium due to their liquidity. While decentralized protocols increasingly adop...

We ask whether pretrained time series foundation models (TSFMs) improve on established econometric benchmarks for forecasting realized volatility. Using the VOLARE dataset, we conduct the first system...