Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper builds a core-satellite model of semi-static Kelly betting and log-optimal investment. We study the problem of a saver whose core portfolio consists in unlevered (1x) retirement plans wit...

To protect his teaching evaluations, an economics professor uses the following exam curve: if the class average falls below a known target, $m$, then all students will receive an equal number of fre...

This paper formulates and solves the optimal stopping problem for a loan made to one's self from a tax-advantaged retirement account such as a 401(k), 403(b), or 457(b) plan. If the plan participant...

This paper studies the general relationship between the gearing ratio of a Leveraged ETF and its corresponding expense ratio, viz., the investment management fees that are charged for the provision ...

I juxtapose Cover's vaunted universal portfolio selection algorithm (Cover 1991) with the modern representation (Qian 2016; Roncalli 2013) of a portfolio as a certain allocation of risk among the av...

This note provides a neat and enjoyable expansion and application of the magnificent Ordentlich-Cover theory of "universal portfolios." I generalize Cover's benchmark of the best constant-rebalanced...

I unravel the basic long run dynamics of the broker call money market, which is the pile of cash that funds margin loans to retail clients (read: continuous time Kelly gamblers). Call money is assum...

We consider a two-person trading game in continuous time whereby each player chooses a constant rebalancing rule $b$ that he must adhere to over $[0,t]$. If $V_t(b)$ denotes the final wealth of the ...

This paper supplies two possible resolutions of Fortune's (2000) margin-loan pricing puzzle. Fortune (2000) noted that the margin loan interest rates charged by stock brokers are very high in relati...

In this paper, which is the third installment of the author's trilogy on margin loan pricing, we analyze $1,367$ monthly observations of the U.S. broker call money rate, which is the interest rate a...

I derive practical formulas for optimal arrangements between sophisticated stock market investors (namely, continuous-time Kelly gamblers or, more generally, CRRA investors) and the brokers who lend...

We study T. Cover's rebalancing option (Ordentlich and Cover 1998) under discrete hindsight optimization in continuous time. The payoff in question is equal to the final wealth that would have accru...

This paper studies a two-person trading game in continuous time that generalizes Garivaltis (2018) to allow for stock prices that both jump and diffuse. Analogous to Bell and Cover (1988) in discret...

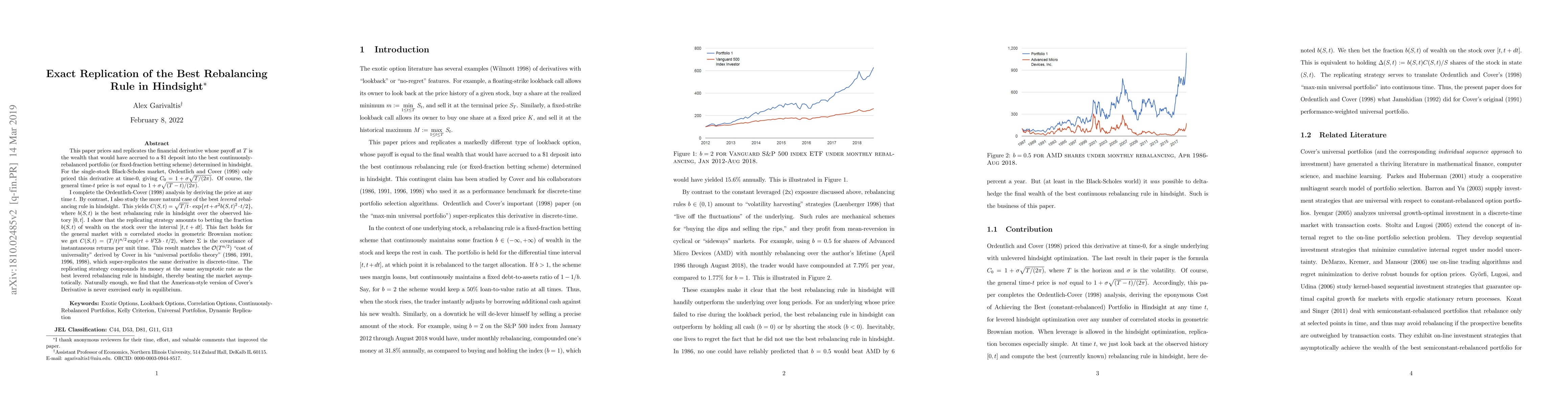

This paper prices and replicates the financial derivative whose payoff at $T$ is the wealth that would have accrued to a $\$1$ deposit into the best continuously-rebalanced portfolio (or fixed-fract...

In a pathbreaking paper, Cover and Ordentlich (1998) solved a max-min portfolio game between a trader (who picks an entire trading algorithm, $\theta(\cdot)$) and "nature," who picks the matrix $X$ ...

This paper derives a robust on-line equity trading algorithm that achieves the greatest possible percentage of the final wealth of the best pairs rebalancing rule in hindsight. A pairs rebalancing r...