Academic Profile

Statistics

Similar Authors

Papers on arXiv

Spatial heteroskedasticity refers to stochastically changing variances and covariances in space. Such features have been observed in, for example, air pollution and vegetation data. We study how vol...

We consider trawl processes, which are stationary and infinitely divisible stochastic processes and can describe a wide range of statistical properties, such as heavy tails and long memory. In this ...

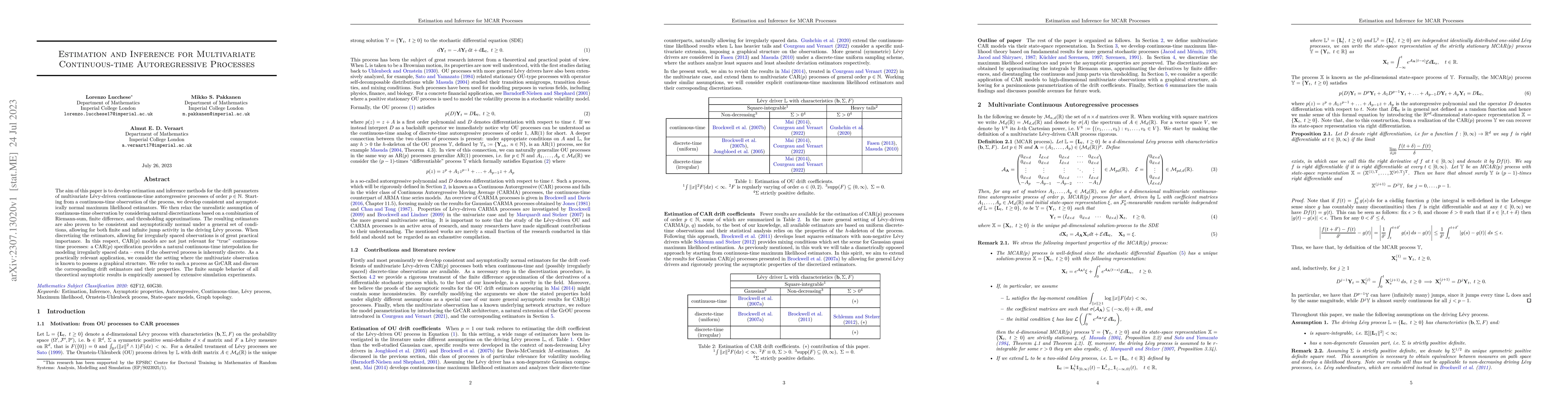

The aim of this paper is to develop estimation and inference methods for the drift parameters of multivariate L\'evy-driven continuous-time autoregressive processes of order $p\in\mathbb{N}$. Starti...

This article introduces the class of periodic trawl processes, which are continuous-time, infinitely divisible, stationary stochastic processes, that allow for periodicity and flexible forms of thei...

Trawl processes belong to the class of continuous-time, strictly stationary, infinitely divisible processes; they are defined as L\'{e}vy bases evaluated over deterministic trawl sets. This article ...

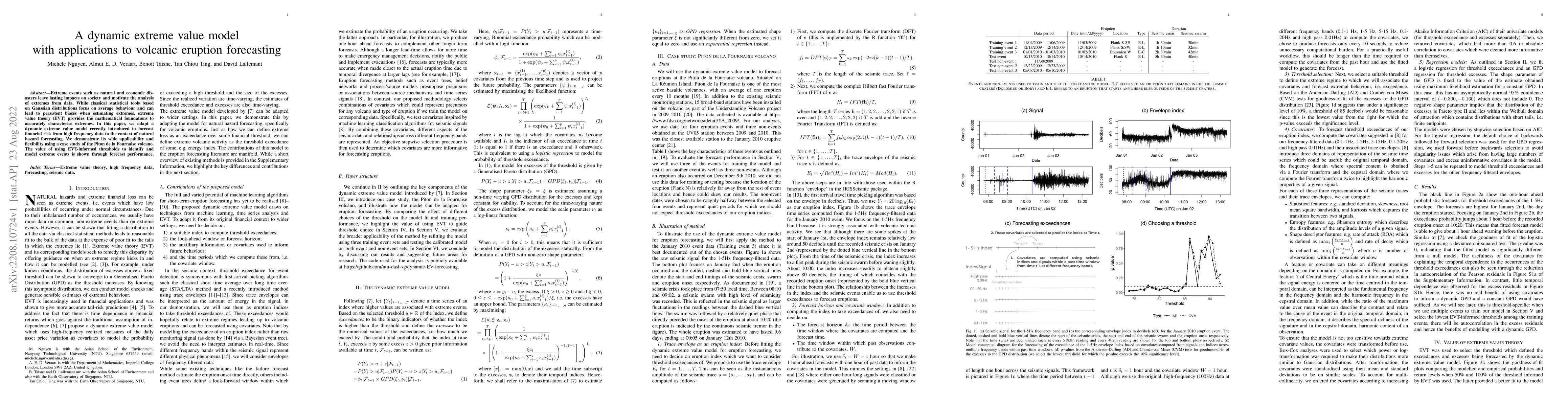

Extreme events such as natural and economic disasters leave lasting impacts on society and motivate the analysis of extremes from data. While classical statistical tools based on Gaussian distributi...

Trawl processes are continuous-time, stationary and infinitely divisible processes which can describe a wide range of possible serial correlation patterns in data. In this paper, we introduce new si...

This article establishes an asymptotic theory for volatility estimation in an infinite-dimensional setting. We consider mild solutions of semilinear stochastic partial differential equations and der...

In this article we will introduce the realised semicovariance for Brownian semistationary (BSS) processes, which is obtained from the decomposition of the realised covariance matrix into components ...

This paper develops likelihood-based methods for estimation, inference, model selection, and forecasting of continuous-time integer-valued trawl processes. The full likelihood of integer-valued traw...

Understanding multivariate extreme events play a crucial role in managing the risks of complex systems since extremes are governed by their own mechanisms. Conditional on a given variable exceeding ...

This article generalises the concept of realised covariation to Hilbert-space-valued stochastic processes. More precisely, based on high-frequency functional data, we construct an estimator of the t...

In this work we derive limit theorems for trawl processes. First,we study the asymptotic behaviour of the partial sums of the discretized trawl process $(X_{i\Delta_{n}})_{i=0}^{\lfloor nt\rfloor-1}...

We consider the problem of modelling restricted interactions between continuously-observed time series as given by a known static graph (or network) structure. For this purpose, we define a parametr...

Prediction of quantiles at extreme tails is of interest in numerous applications. Extreme value modelling provides various competing predictors for this point prediction problem. A common method of ...

We develop a simulation scheme for a class of spatial stochastic processes called volatility modulated moving averages. A characteristic feature of this model is that the behaviour of the moving ave...

While short-range dependence is widely assumed in the literature for its simplicity, long-range dependence is a feature that has been observed in data from finance, hydrology, geophysics and economi...

This article surveys key aspects of ambit stochastics and remembers Ole E. Barndorff-Nielsen's important contributions to the foundation and advancement of this new research field over the last two de...

This article introduces Levy-driven graph supOU processes, offering a parsimonious parametrisation for high-dimensional time-series, where dependencies between the individual components are governed v...

This paper introduces a periodic multivariate Poisson autoregression with potentially infinite memory, with a special focus on the network setting. Using contraction techniques, we study the stability...

The expected signature maps a collection of data streams to a lower dimensional representation, with a remarkable property: the resulting feature tensor can fully characterize the data generating dist...

Extreme events are often multivariate in nature. A compound extreme occurs when a combination of variables jointly produces a significant impact, even if individual components are not necessarily marg...

The growing availability of large and complex datasets has increased interest in temporal stochastic processes that can capture stylized facts such as marginal skewness, non-Gaussian tails, long memor...

We introduce a class of Lévy-driven graph Ornstein-Uhlenbeck (grOU) models for edge-indexed network time series. The proposed framework extends generalized network autoregressive (GNAR) processes for ...

We propose the stochastic block Ornstein-Uhlenbeck (SBOU) process, a continuous-time multivariate model in which the drift matrix encodes a latent group structure among its components. Our main contri...