Academic Profile

Statistics

Similar Authors

Papers on arXiv

Various methods in statistical learning build on kernels considered in reproducing kernel Hilbert spaces. In applications, the kernel is often selected based on characteristics of the problem and th...

Higher order risk measures are stochastic optimization problems by design, and for this reason they enjoy valuable properties in optimization under uncertainties. They nicely integrate with stochast...

The quantization problem aims to find the best possible approximation of probability measures on ${\mathbb{R}}^d$ using finite, discrete measures. The Wasserstein distance is a typical choice to mea...

This paper proposes a novel technique called "successive stochastic smoothing" that optimizes nonsmooth and discontinuous functions while considering various constraints. Our methodology enables loc...

This contribution presents substantial computational advancements to compare measures even with varying masses. Specifically, we utilize the nonequispaced fast Fourier transform to accelerate the ra...

The paper addresses general constrained and non-linear optimization problems. For some of these notoriously hard problems, there exists a reformulation as an unconstrained, global optimization probl...

This paper features expectiles in dynamic and stochastic optimization. Expectiles are a family of risk functionals characterized as minimizers of optimization problems. For this reason, they enjoy v...

This contribution features an accelerated computation of the Sinkhorn's algorithm, which approximates the Wasserstein transportation distance, by employing nonequispaced fast Fourier transforms (NFF...

This paper addresses the problem of regression to reconstruct functions, which are observed with superimposed errors at random locations. We address the problem in reproducing kernel Hilbert spaces....

The Covid-19 pandemic still causes severe impacts on society and the economy. This paper studies excess mortality during the pandemic years 2020 and 2021 in Germany empirically with a special focus ...

We study evolution equations of drift-diffusion type when various parameters are random. Motivated by applications in pedestrian dynamics, we focus on the case when the total mass is, due to boundar...

Multistage stochastic optimization problems are oftentimes formulated informally in a pathwise way. These are correct in a discrete setting and suitable when addressing computational challenges, for...

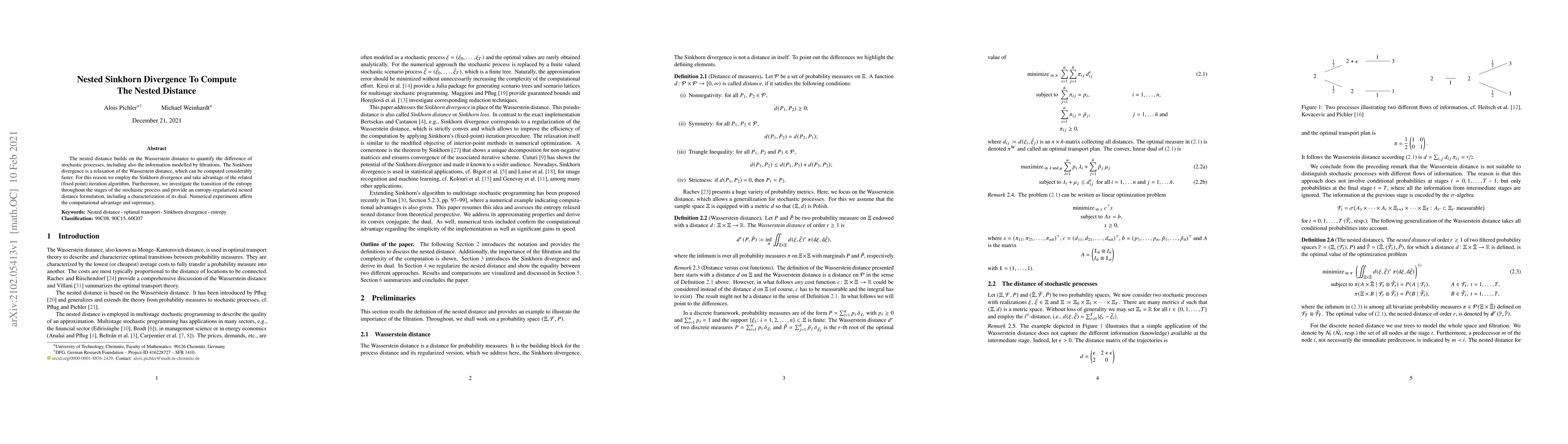

The nested distance builds on the Wasserstein distance to quantify the difference of stochastic processes, including also the information modelled by filtrations. The Sinkhorn divergence is a relaxa...

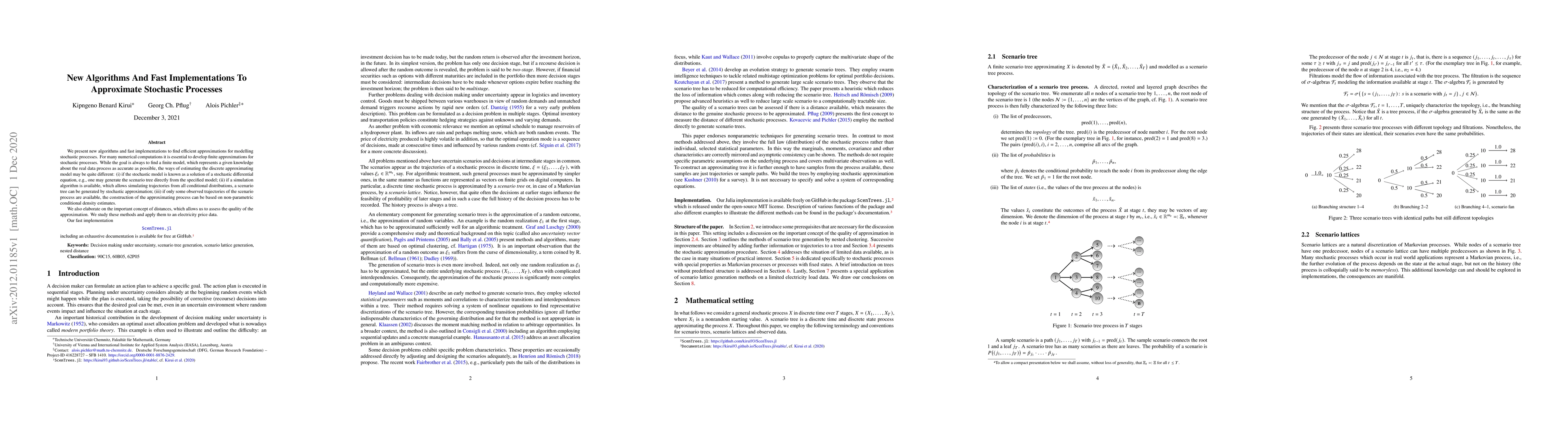

We present new algorithms and fast implementations to find efficient approximations for modelling stochastic processes. For many numerical computations it is essential to develop finite approximatio...

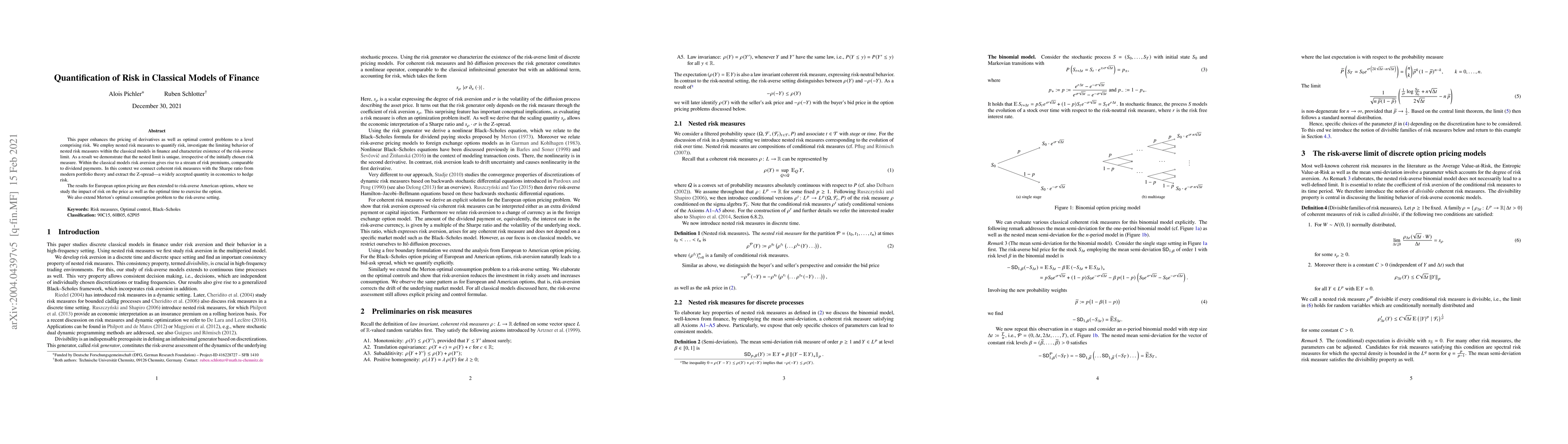

This paper enhances the pricing of derivatives as well as optimal control problems to a level comprising risk. We employ nested risk measures to quantify risk, investigate the limiting behavior of n...

Risk measures connect probability theory or statistics to optimization, particularly to convex optimization. They are nowadays standard in applications of finance and in insurance involving risk ave...

When propagating uncertainty in the data of differential equations, the probability laws describing the uncertainty are typically themselves subject to uncertainty. We present a sensitivity analysis...

Any applied mathematical model contains parameters. The paper proposes to use kernel learning for the parametric analysis of the model. The approach consists in setting a distribution on the parameter...

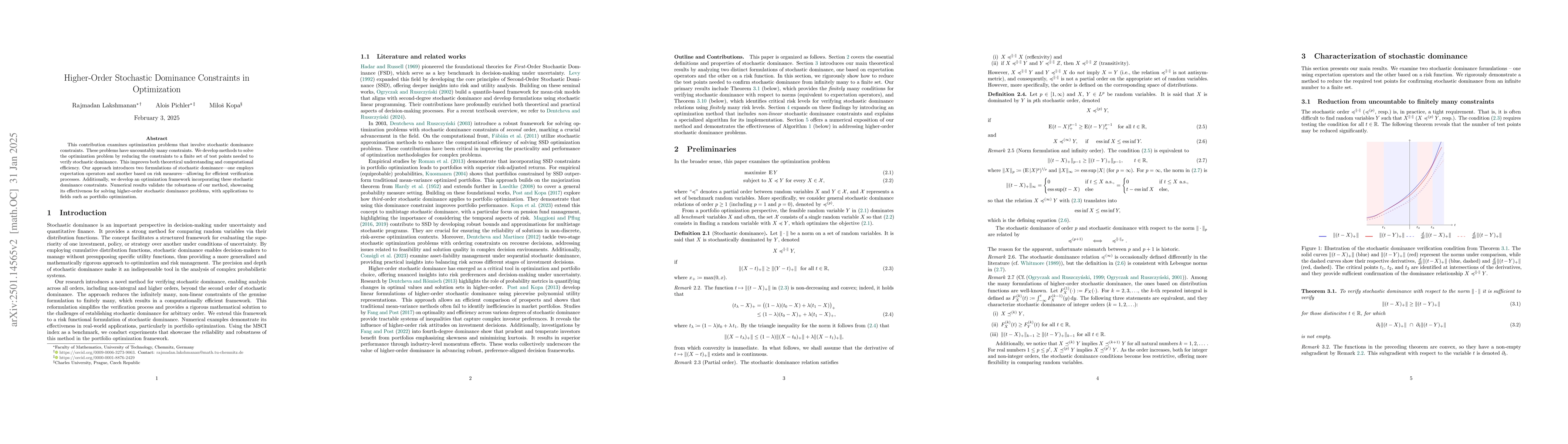

This contribution examines optimization problems that involve stochastic dominance constraints. These problems have uncountably many constraints. We develop methods to solve the optimization problem b...

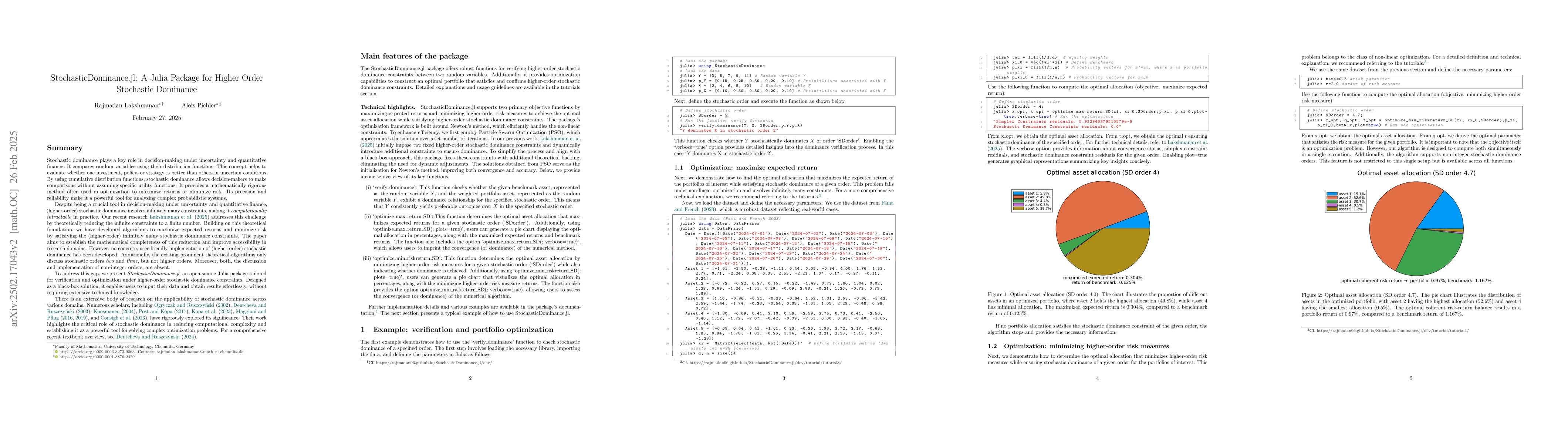

Stochastic dominance is a fundamental concept in decision-making under uncertainty and quantitative finance, yet its practical application is hindered by computational intractability due to infinitely...

Accurate approximation of probability measures is essential in numerical applications. This paper explores the quantization of probability measures using the maximum mean discrepancy (MMD) distance as...