Academic Profile

Statistics

Similar Authors

Papers on arXiv

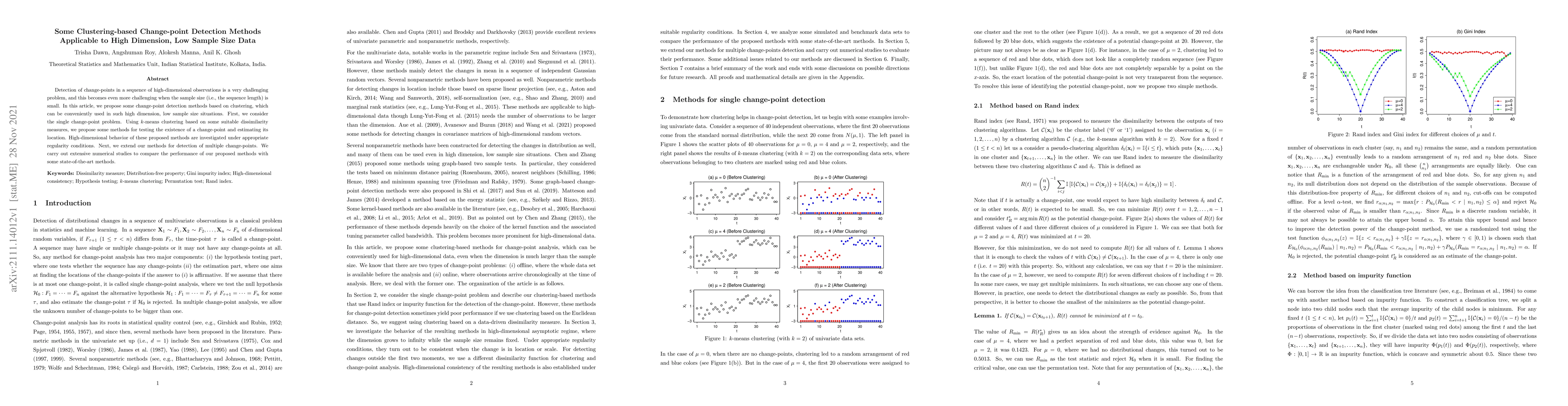

Detection of change-points in a sequence of high-dimensional observations is a very challenging problem, and this becomes even more challenging when the sample size (i.e., the sequence length) is sm...

The Tweedie exponential dispersion family is a popular choice among many to model insurance losses that consist of zero-inflated semicontinuous data. In such data, it is often important to obtain cred...

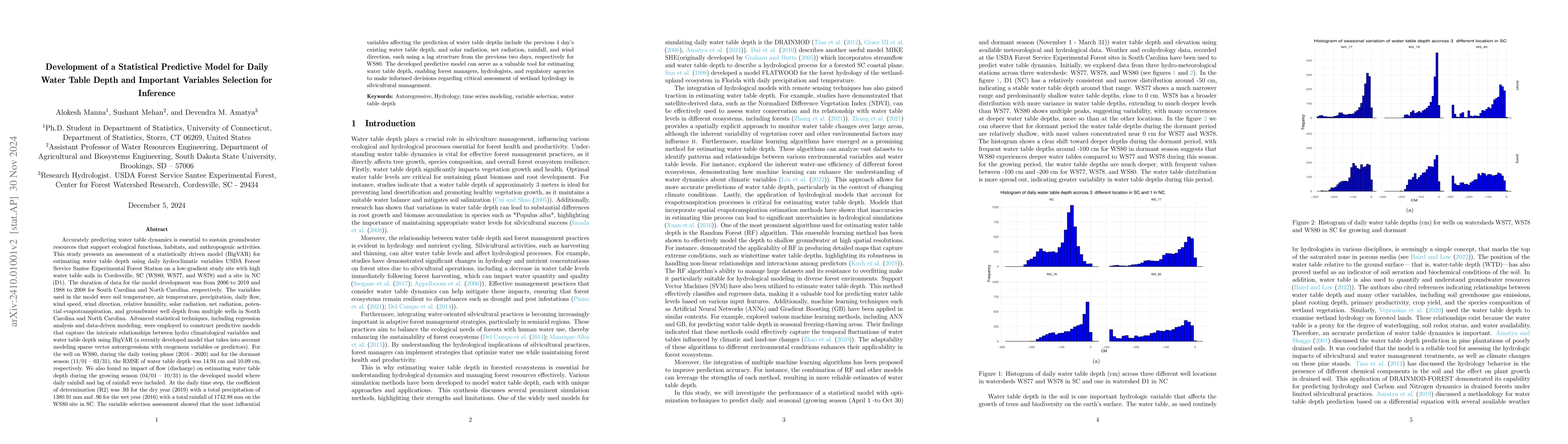

Accurately predicting water table dynamics is vital for sustaining groundwater resources that support ecological functions and anthropogenic activities. This study evaluates a statistical model (BigVA...

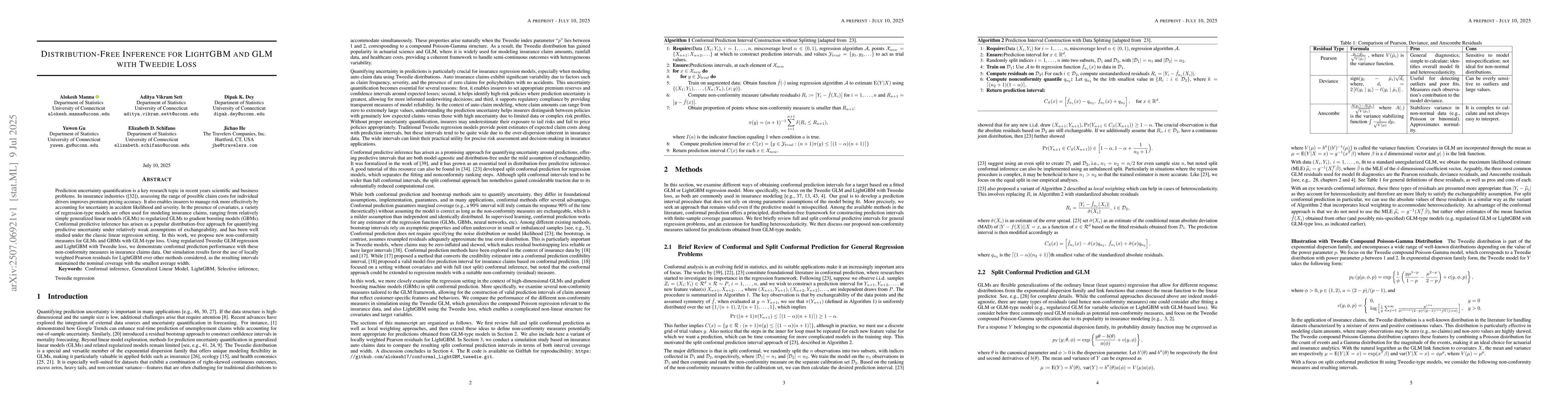

Prediction uncertainty quantification is a key research topic in recent years scientific and business problems. In insurance industries (\cite{parodi2023pricing}), assessing the range of possible clai...

We develop a Bayesian framework for variable selection in linear regression with autocorrelated errors, accommodating lagged covariates and autoregressive structures. This setting occurs in time serie...

Shoe print evidence recovered from crime scenes plays a key role in forensic investigations. By examining shoe prints, investigators can determine details of the footwear worn by suspects. However, es...

Linguistic insights may help make Large Language Model (LLM) training more efficient. We trained Meta's OPT model on the 100M word BabyLM dataset, and evaluated it on the BLiMP benchmark, which consis...