Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we consider pricing of European options and spread options for Hawkes-based model for the limit order book. We introduce multivariate Hawkes process and the multivariable general comp...

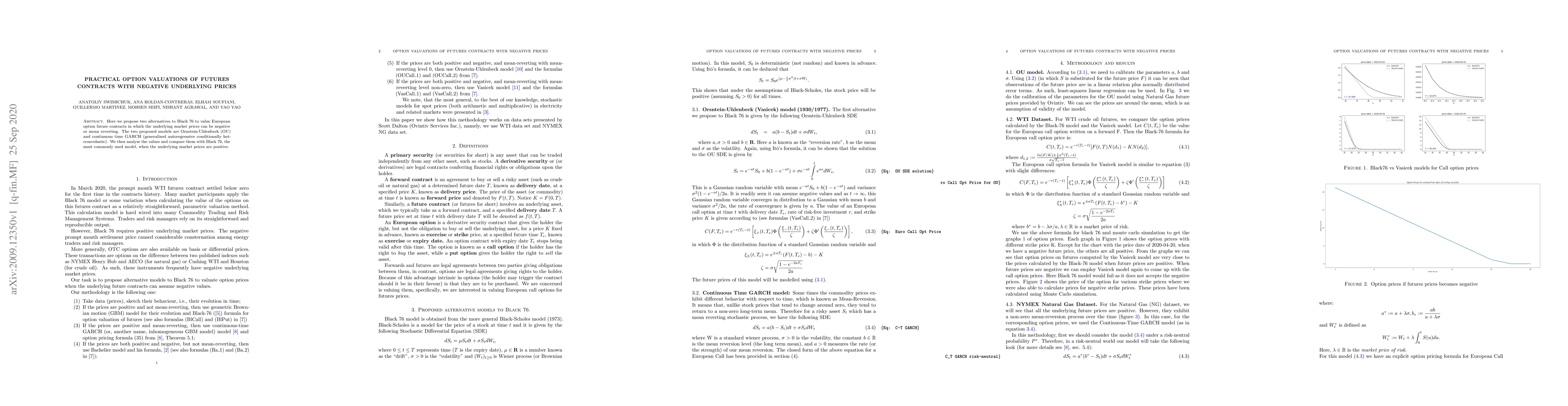

Here we propose two alternatives to Black 76 to value European option future contracts in which the underlying market prices can be negative or mean reverting. The two proposed models are Ornstein-U...

In this paper, we focus on a new generalization of multivariate general compound Hawkes process (MGCHP), which we referred to as the multivariate general compound point process (MGCPP). Namely, we a...

In this paper, we study the effects of fill probabilities and adverse fills on the trading strategy simulation process. We specifically focus on a stochastic optimal control market-making problem and ...

We develop a deep reinforcement learning (RL) framework for an optimal market-making (MM) trading problem, specifically focusing on price processes with semi-Markov and Hawkes Jump-Diffusion dynamics....

We define a new model using a Hawkes process as a subordinator in a standard Brownian motion. We demonstrate that this Hawkes subordinated Brownian motion or more succinctly, variance-Hawkes process c...

Algorithmic and High-Frequency trading (HFT) has become one of the main ways to complete transactions in many of today's major financial markets, with these transactions taking place inside what is ca...

This paper is devoted to the study of a new so-called self-exciting random evolutions (SEREs) and their applications. We introduce a new random process $x(t)$ such that it is based on a superposition ...

In this paper, we propose an event-driven Limit Order Book (LOB) model that captures twelve of the most observed LOB events in exchange-based financial markets. To model these events, we propose using...

We give functional laws of large numbers for a class of marked Hawkes processes and marked compound Hawkes processes with a general mark space. Our results provide some complement to those presented p...