Academic Profile

Statistics

Similar Authors

Papers on arXiv

A distributional equation as a criterion for invariant measures of Markov processes associated to L\'evy-type operators is established. This is obtained via a characterization of infinitesimally inv...

We establish sufficient conditions for the existence, and derive explicit formulas for the $\kappa$'th moments, $\kappa \geq 1$, of Markov modulated generalized Ornstein-Uhlenbeck processes as well ...

We derive the Markov-modulated generalized Ornstein-Uhlenbeck process by embedding a Markov-modulated random recurrence equation in continuous time. The obtained process turns out to be the unique s...

Scale functions play a central role in the fluctuation theory of spectrally negative L\'evy processes. For spectrally negative compound Poisson processes with positive drift, a new representation of...

In this article a special case of an M/G/2-queue is considered, where the two servers are exposed to two types of jobs that are distributed among the servers via a random switch. In this model the a...

For two independent L\'{e}vy processes $\xi$ and $\eta$ and an exponentially distributed random variable $\tau$ with parameter $q>0$ that is independent of $\xi$ and $\eta$, the killed exponential f...

For two independent L\'evy processes $\xi$ and $\eta$ and an exponentially distributed random variable $\tau$ with parameter $q>0$, independent of $\xi$ and $\eta$, the killed exponential functional...

We provide necessary and sufficient conditions for convergence of exponential integrals of Markov additive processes. Other than in the classical L\'evy case studied by Erickson and Maller we have t...

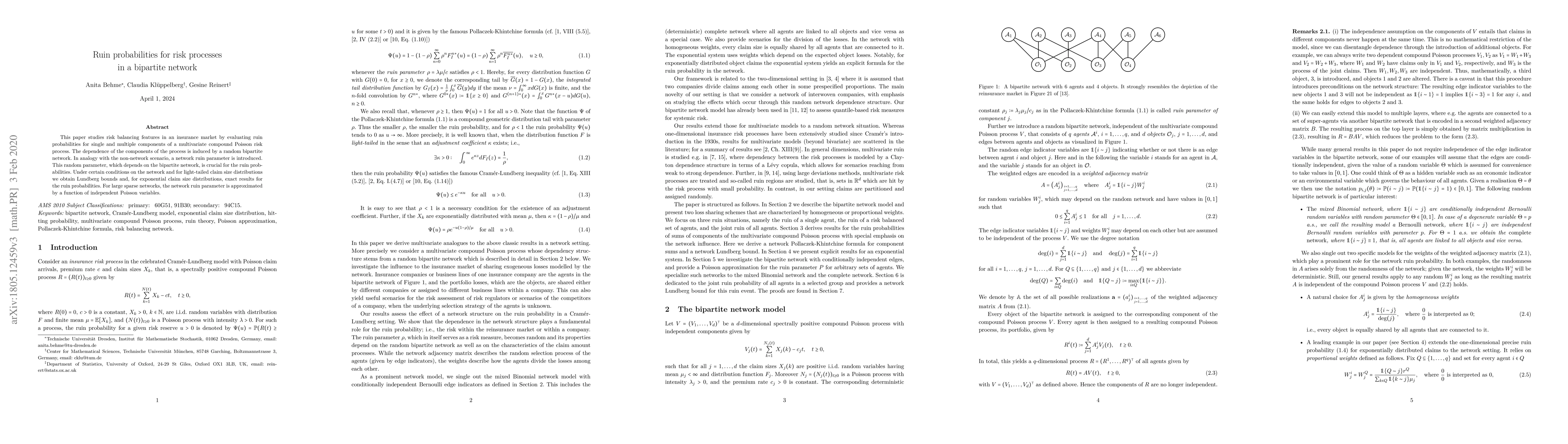

This paper studies risk balancing features in an insurance market by evaluating ruin probabilities for single and multiple components of a multivariate compound Poisson risk process. The dependence ...

We study the long-time behaviour of matrix-valued stochastic exponentials of L\'evy processes, i.e. of multiplicative L\'evy processes in the general linear group. In particular, we prove laws of larg...

We introduce generalizations of the COGARCH model of Kl\"uppelberg et al. from 2004 and the volatility and price model of Barndorff-Nielsen and Shephard from 2001 to a Markov-switching environment. Th...

We derive explicit representations for the (Siegmund-) dual and the time-reversed flow of generalized Ornstein-Uhlenbeck processes whenever these exist. It turns out that the dual and the process corr...

We extend the L\'evy Langevin Monte Carlo method studied by Oechsler in 2024 to the setting of a target distribution with heavy tails: Choosing a target distribution from the class of subexponential d...

This article studies regularity properties of multiplicative stochastic processes on infinite-dimensional Lie groups. We investigate conditions under which these processes admit càdlàg modifications a...

We study the tail behavior of Markov-modulated generalized Ornstein-Uhlenbeck processes -- that is, solutions to Langevin-type stochastic differential equations driven by a background continuous-time ...