Academic Profile

Statistics

Similar Authors

Papers on arXiv

Linear instrumental variable regressions are widely used to estimate causal effects. Many instruments arise from the use of ``technical'' instruments and more recently from the empirical strategy of...

This paper studies linear time series regressions with many regressors. Weak exogeneity is the most used identifying assumption in time series. Weak exogeneity requires the structural error to have ...

We consider estimation in moment condition models and show that under any bound on identification strength, asymptotically admissible (i.e. undominated) estimators in a wide class of estimation prob...

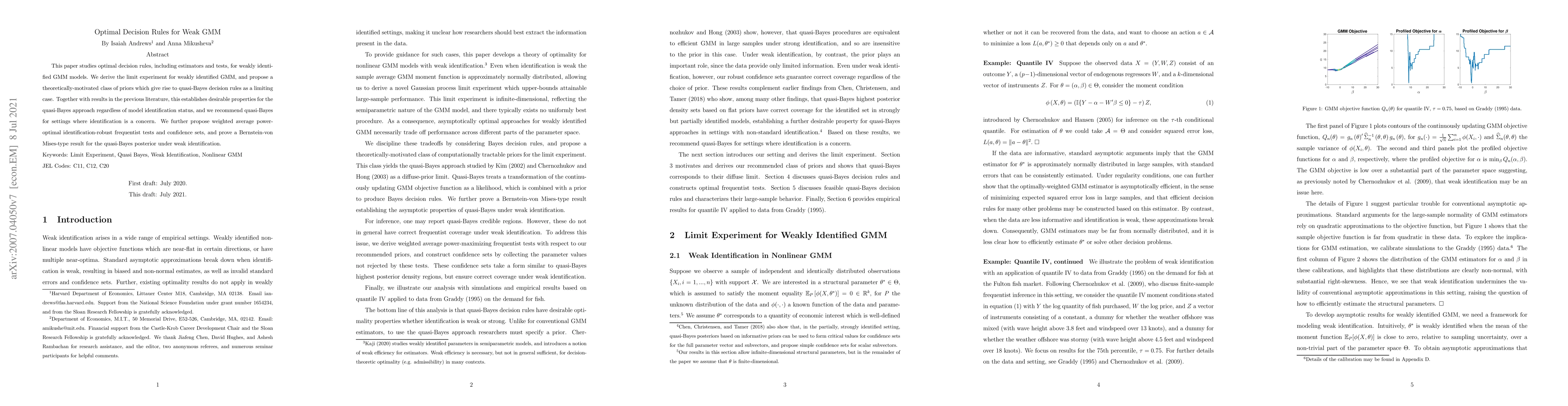

This paper studies optimal decision rules, including estimators and tests, for weakly identified GMM models. We derive the limit experiment for weakly identified GMM, and propose a theoretically-mot...

We develop a concept of weak identification in linear IV models in which the number of instruments can grow at the same rate or slower than the sample size. We propose a jackknifed version of the cl...

The paper establishes the central limit theorems and proposes how to perform valid inference in factor models. We consider a setting where many counties/regions/assets are observed for many time per...

We study linear regression models with clustered data, high-dimensional controls, and a complicated structure of exclusion restrictions. We propose a correctly centered internal IV estimator that acco...