Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study and solve the worst-case optimal portfolio problem as pioneered by Korn and Wilmott (2002) of an investor with logarithmic preferences facing the possibility of a market crash with stochast...

We study the $L^1$-approximation of the log-Heston SDE at the terminal time point by arbitrary methods that use an equidistant discretization of the driving Brownian motion. We show that such method...

We study the $L^1$-approximation of the log-Heston SDE at equidistant time points by Euler-type methods. We establish the convergence order $ 1/2-\epsilon$ for $\epsilon >0$ arbitrarily small, if th...

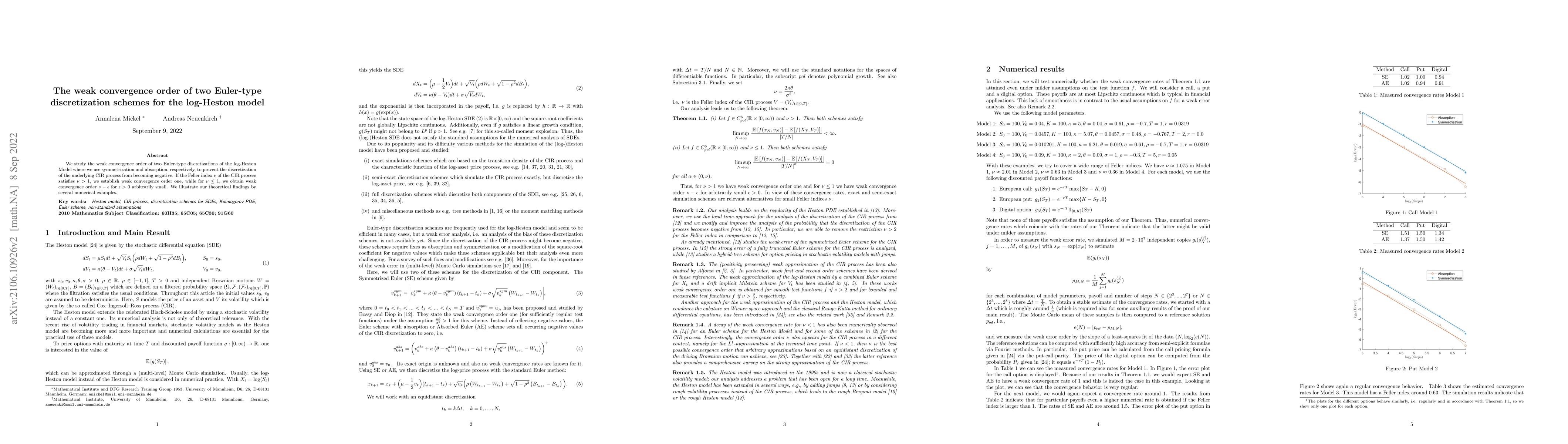

We study the weak convergence order of two Euler-type discretizations of the log-Heston Model where we use symmetrization and absorption, respectively, to prevent the discretization of the underlyin...