Academic Profile

Statistics

Similar Authors

Papers on arXiv

We give a thorough description of the asymptotic property of the maximum likelihood estimator (MLE) of the skewness parameter of a Skew Brownian Motion (SBM). Thanks to recent results on the Central...

We give an asymptotic development of the maximum likelihood estimator (MLE), or any other estimator defined implicitly, in a way which involves the limiting behavior of the score and its higher-orde...

We prove the convergence of the law of grid-valued random walks, which can be seen as time-space Markov chains, to the law of a general diffusion process. This includes processes with sticky feature...

The non-linear sewing lemma constructs flows of rough differential equations from a braod class of approximations called almost flows. We consider a class of almost flows that could be approximated ...

Solutions of Rough Differential Equations (RDE) may be defined as paths whose increments are close to an approximation of the associated flow. They are constructed through a discrete scheme using a ...

We give an unified framework to solve rough differential equations. Based on flows, our approach unifies the former ones developed by Davie, Friz-Victoir and Bailleul. The main idea is to build a fl...

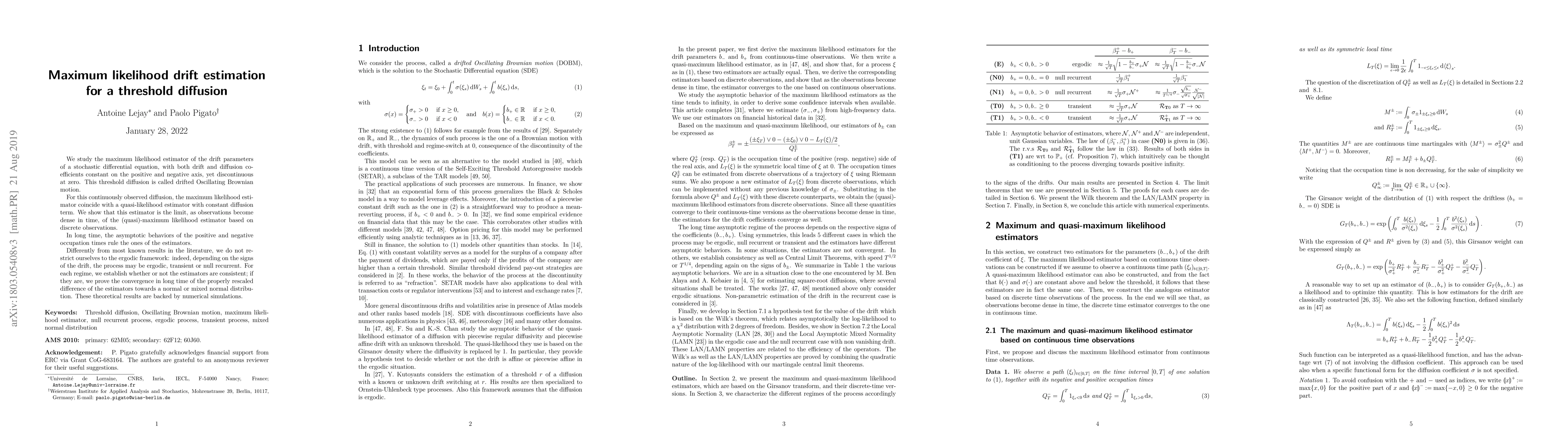

We study the maximum likelihood estimator of the drift parameters of a stochastic differential equation, with both drift and diffusion coefficients constant on the positive and negative axis, yet di...