Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we study the well-posedness and regularity of non-autonomous stochastic differential algebraic equations (SDAEs) with nonlinear, locally Lipschitz and monotone (2) coefficients of the...

The aim of this work is to provide the first strong convergence result of numerical approximation of a general time-fractional second order stochastic partial differential equation involving a Caput...

Stochastic optimal principle leads to the resolution of a partial differential equation (PDE), namely the Hamilton-Jacobi-Bellman (HJB) equation. In general, this equation cannot be solved analytica...

In this article, we provide a numerical method based on fitted finite volume method to approximate the Hamilton-Jacobi-Bellman (HJB) equation coming from stochastic optimal control problems. The com...

In this work, we investigate the numerical approximation of the second order non-autonomous semilnear parabolic partial differential equation (PDE) using the finite element method. To the best of ou...

In this paper, we study the numerical approximation of a general second order semilinear stochastic partial differential equation (SPDE) driven by a additive fractional Brownian motion (fBm) with Hu...

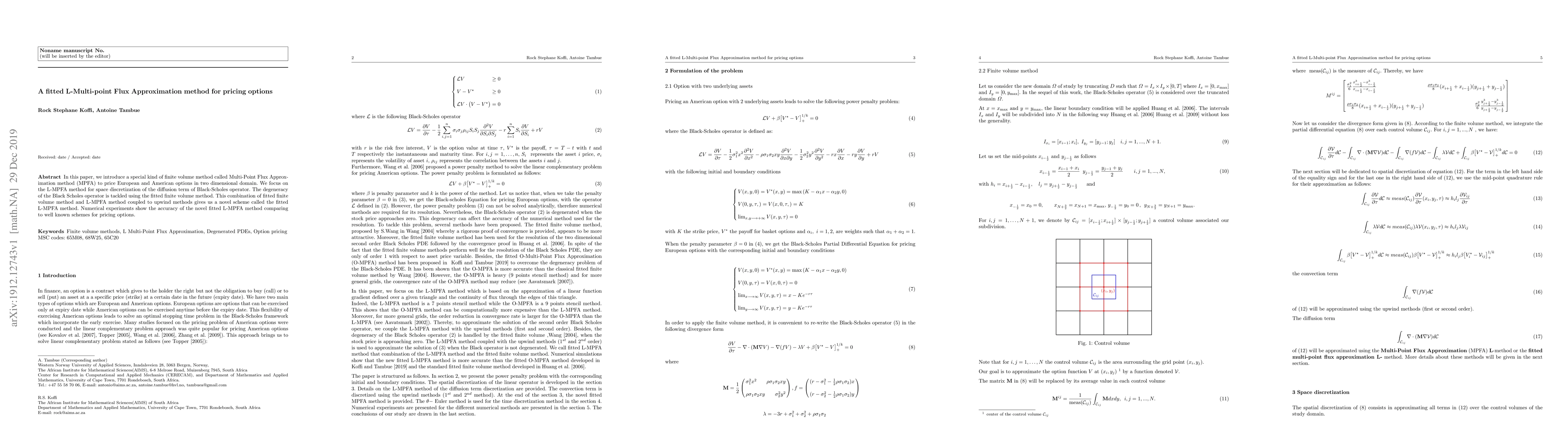

In this paper, we introduce a special kind of finite volume method called Multi-Point Flux Approximation method (MPFA) to price European and American options in two dimensional domain. We focus on t...

In this paper, we deal with numerical approximations for solving the Black-Scholes Partial Differential Equation (PDE). This PDE is well known to be degenerated. The space discretization is performe...

This paper deals with the backward Euler method applied to semilinear parabolic stochastic partial differential equations (SPDEs) driven by additive noise. The SPDE is discretized in space by the fi...

For a homogenization problem associated to a linear elliptic operator, we prove the existence of a distributional corrector and we find an approximation scheme for the homogenized coefficients. We a...

The aim of this work is to provide the strong convergence results of numerical approximations of a general second order non-autonomous semilinear stochastic partial differential equation (SPDE) driven...

This paper delves into the well-posedness and the numerical approximation of non-autonomous stochastic differential algebraic equations (SDAEs) with nonlinear local Lipschitz coefficients that satisfy...

We are investigating the first strong convergence analysis of a numerical method for stochastic differential algebraic equations (SDAEs) under a non-global Lipschitz setting. It is well known that the...

The computation of the Log-determinant of large, sparse, symmetric positive definite (SPD) matrices is essential in many scientific computational fields such as numerical linear algebra and machine le...

The paper deals with the numerical treatment of index-1 stochastic differential-algebraic equations (SDAEs) with nonlinear coefficients that satisfy the local Lipschitz and the Khasminskii conditions....

Estimating the logarithm of the determinant of large sparse positive definite symmetric matrices is an important task in numerical linear algebra, machine learning, Gaussian processes, and uncertainty...