Academic Profile

Statistics

Similar Authors

Papers on arXiv

Given a Gaussian process $(X_t)_{t \in \mathbb{R}}$, we construct a Gaussian \emph{Markov} process with the same one-dimensional marginals using sequences of transformations of $(X_t)_{t \in \mathbb{R...

We study the small-regularisation limit of the entropic optimal transport problem on the line with distance cost. While convergence of entropic minimizers is well understood in the discrete setting an...

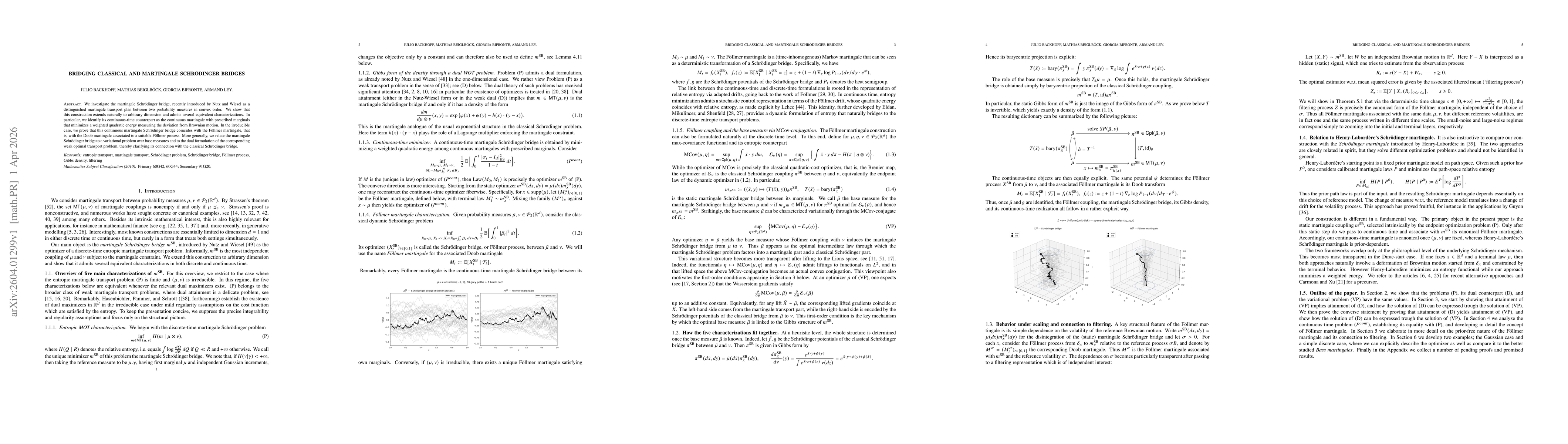

We investigate the martingale Schrödinger bridge, recently introduced by Nutz and Wiesel as a distinguished martingale transport plan between two probability measures in convex order. We show that thi...