Academic Profile

Statistics

Similar Authors

Papers on arXiv

We combine the one-dimensional Monte Carlo simulation and the semi-analytical one-dimensional heat potential method to design an efficient technique for pricing barrier options on assets with correl...

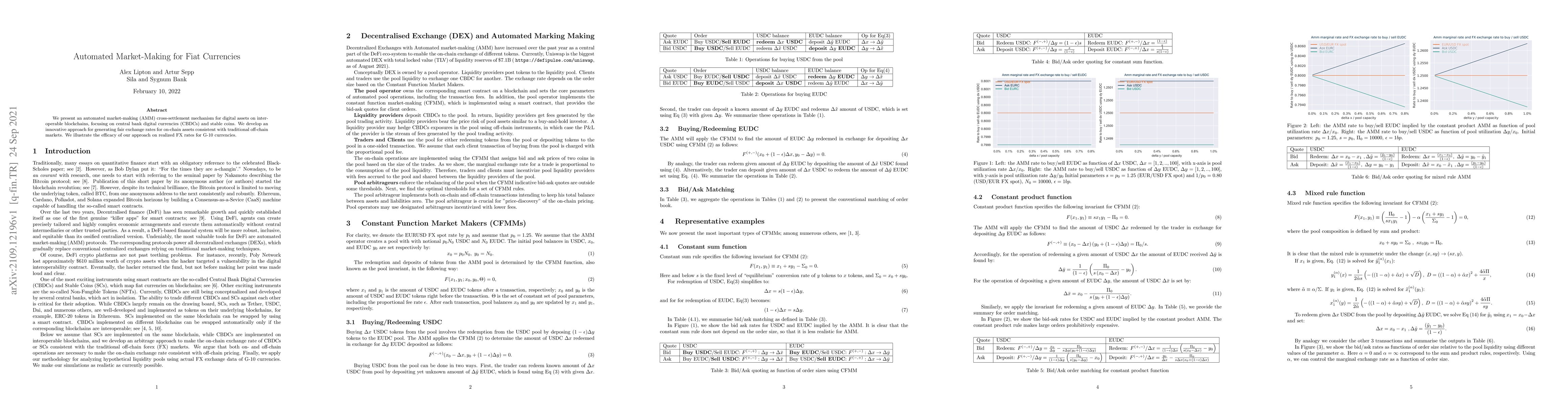

We present an automated market-making (AMM) cross-settlement mechanism for digital assets on interoperable blockchains, focusing on central bank digital currencies (CBDCs) and stable coins. We devel...

We develop static and dynamic approaches for hedging of the impermanent loss (IL) of liquidity provision (LP) staked at Decentralised Exchanges (DEXes) which employ Uniswap V2 and V3 protocols. We pro...

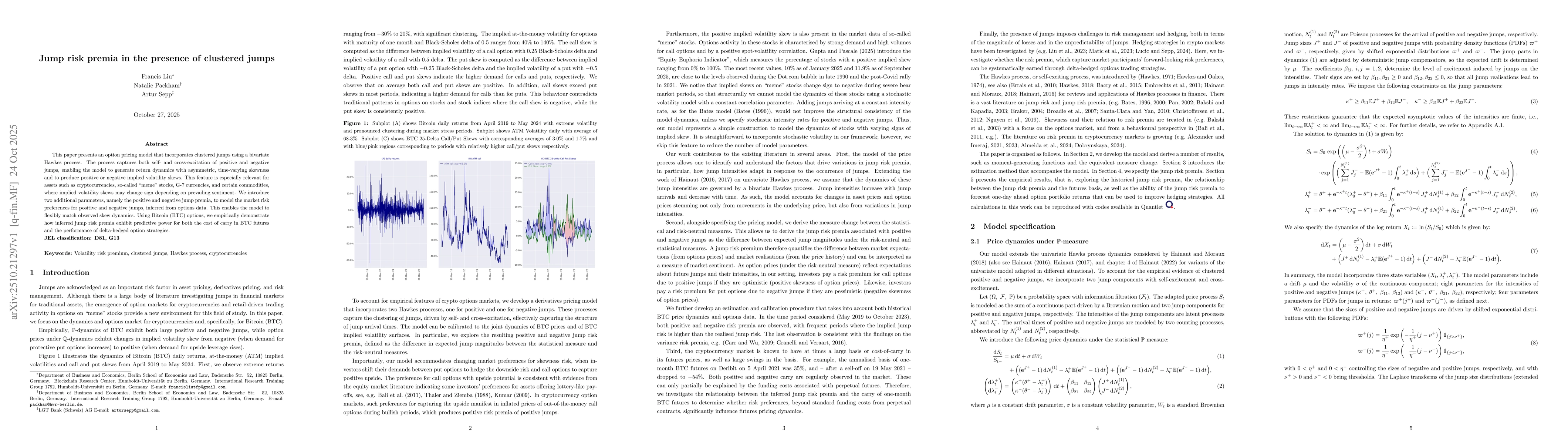

This paper presents an option pricing model that incorporates clustered jumps using a bivariate Hawkes process. The process captures both self- and cross-excitation of positive and negative jumps, ena...