Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this note, we characterize the limiting functions in mod-Gausssian convergence; our approach sheds a new light on the nature of mod-Gaussian convergence as well. Our results in fact more generall...

We introduce a new numerical approximation method for functionals of factor credit portfolio models based on the theory of mod-$\phi$ convergence and mod-$\phi$ approximation schemes. The method can...

In this article, we provide an extension of the Chen-Stein inequality for Poisson approximation in the total variation distance for sums of independent Bernoulli random variables in two ways. We pro...

In this article, we establish the mod-$\phi$ convergence of the major index of a uniform random standard tableau whose shape converges in the Thoma simplex. This implies various probabilistic estima...

We present several refinements on the fluctuations of sequences of random vectors (with values in the Euclidean space $\mathbb{R}^d$) which converge after normalization to a multidimensional Gaussia...

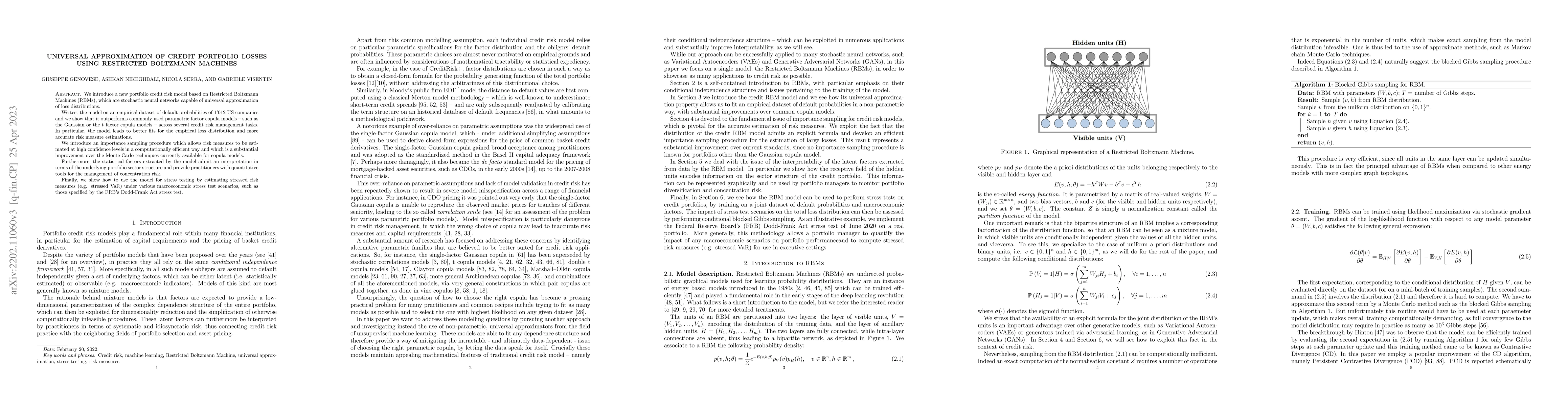

We introduce a new portfolio credit risk model based on Restricted Boltzmann Machines (RBMs), which are stochastic neural networks capable of universal approximation of loss distributions. We test t...

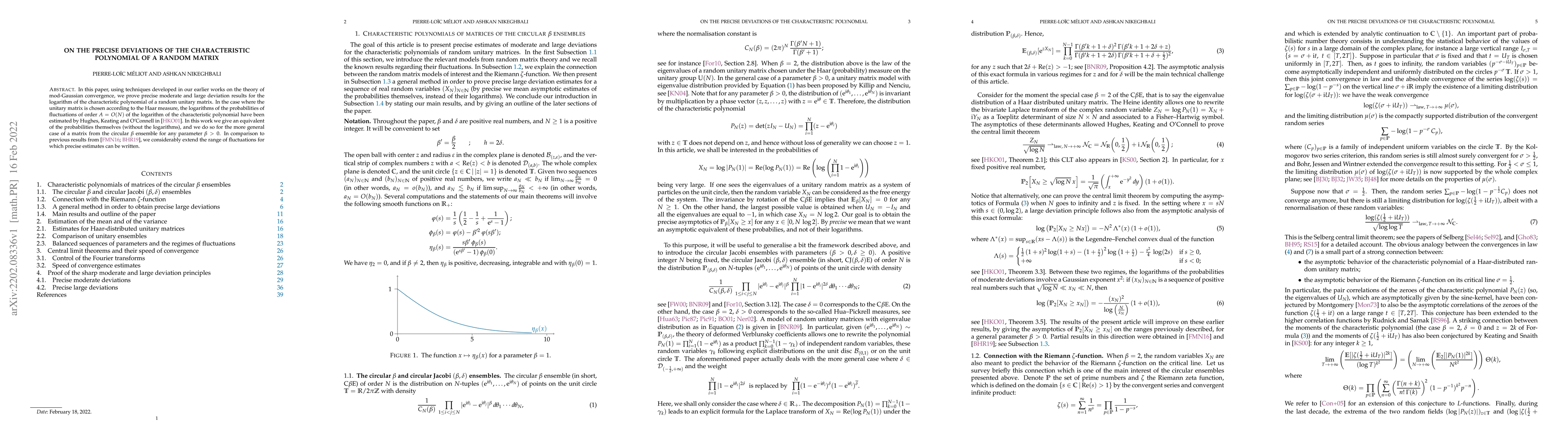

In this paper, using techniques developed in our earlier works on the theory of mod-Gaussian convergence, we prove precise moderate and large deviation results for the logarithm of the characteristi...

In this article, we provide sufficient conditions under which the convergence of random point processes on the real line implies the convergence in law, for the topology of uniform convergence on co...