Academic Profile

Statistics

Similar Authors

Papers on arXiv

This study investigates the efficiency of some select stock markets. Using an improved wavelet estimator of long range dependence, we show evidence of long memory in the stock returns of some emergi...

This study attempts to investigate into the structure and features of global equity markets from a time-frequency perspective. An analysis grounded on this framework allows one to capture informatio...

This paper introduces a novel framework for analyzing systemic risk in financial markets through multi-scale network dynamics using Model Context Protocol (MCP) for agent communication. We develop an ...

We address the joint detection-and-attribution problem in cross-border financial contagion through a two-stage framework. The first stage applies wavelet-quantile transfer entropy across time-scales a...

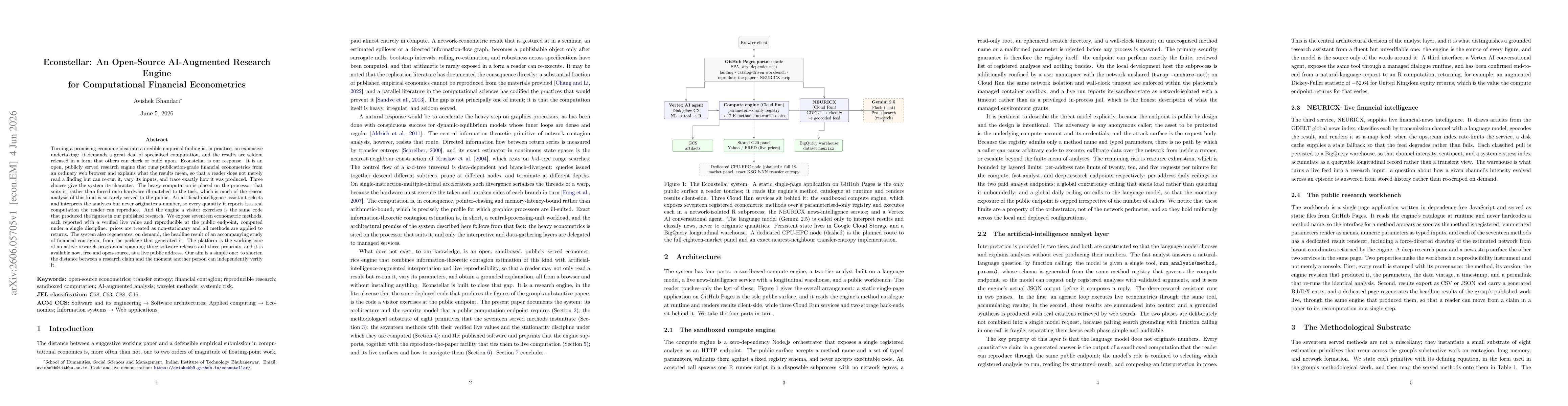

Turning a promising economic idea into a credible empirical finding is, in practice, an expensive undertaking: it demands a great deal of specialised computation, and the results are seldom released i...

In this paper, an attempt is made to examine how the speed at which financial markets absorb information governs the way shocks travel between them. It may be noted that a market which digests news sl...

The competitive equilibrium of general equilibrium theory exists as a fixed point and is, by the theorys own results on aggregate excess demand, in general silent on whether that fixed point is unique...

When markets move more and more in lockstep, are they drifting towards the point where a price bubble becomes possible, and can that drift be measured before the crossing? This paper joins two long-se...

Standard economics assumes the consumer as a flawless calculator who always buys the best basket it can afford. This paper models the shopper instead as a limited information channel: it compresses it...