Academic Profile

Statistics

Similar Authors

Papers on arXiv

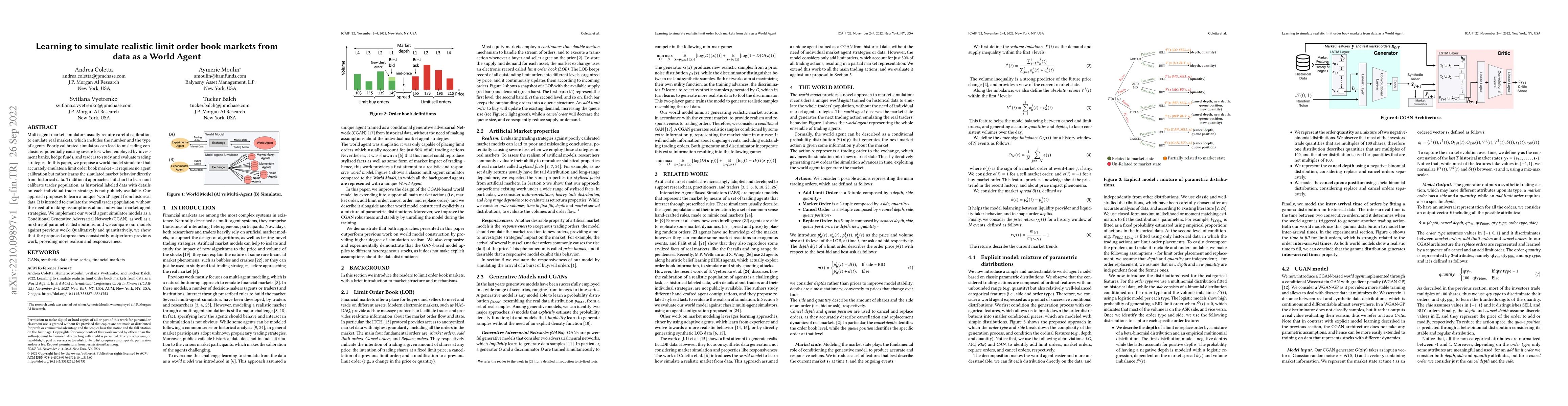

Multi-agent market simulators usually require careful calibration to emulate real markets, which includes the number and the type of agents. Poorly calibrated simulators can lead to misleading concl...

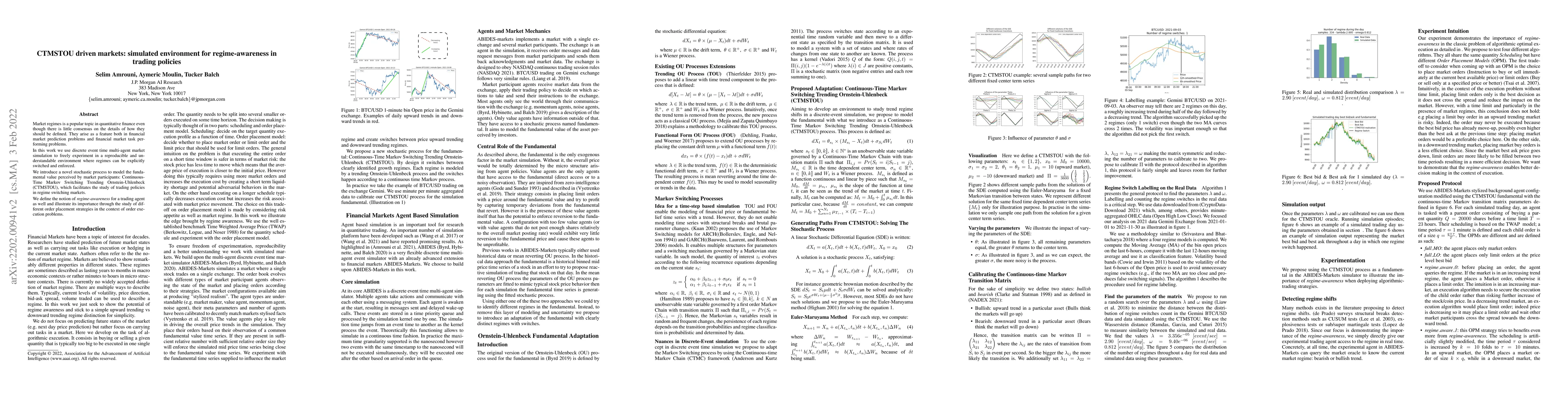

Market regimes is a popular topic in quantitative finance even though there is little consensus on the details of how they should be defined. They arise as a feature both in financial market predict...

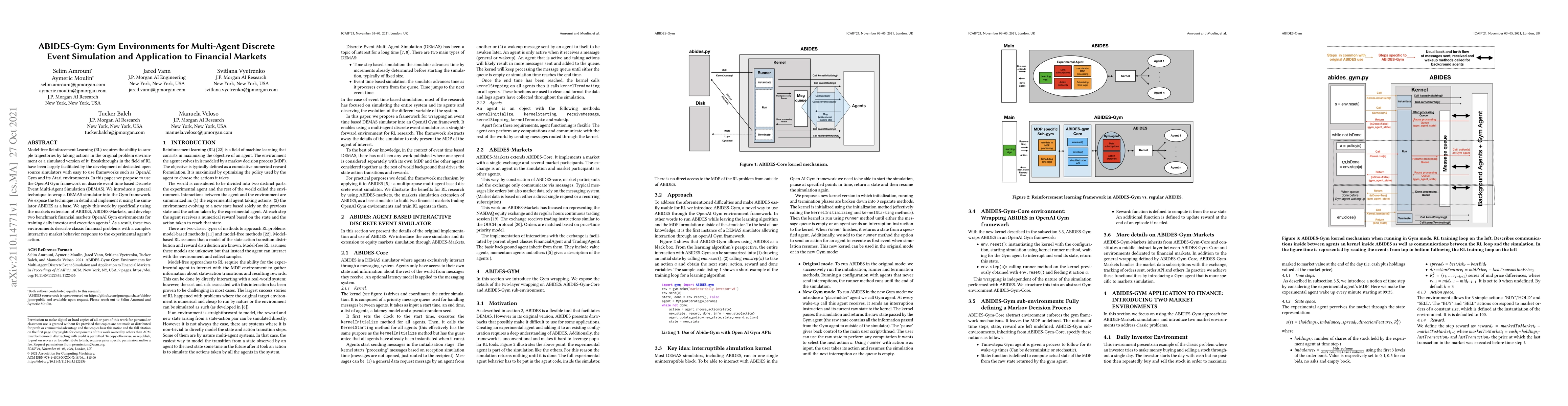

Model-free Reinforcement Learning (RL) requires the ability to sample trajectories by taking actions in the original problem environment or a simulated version of it. Breakthroughs in the field of R...

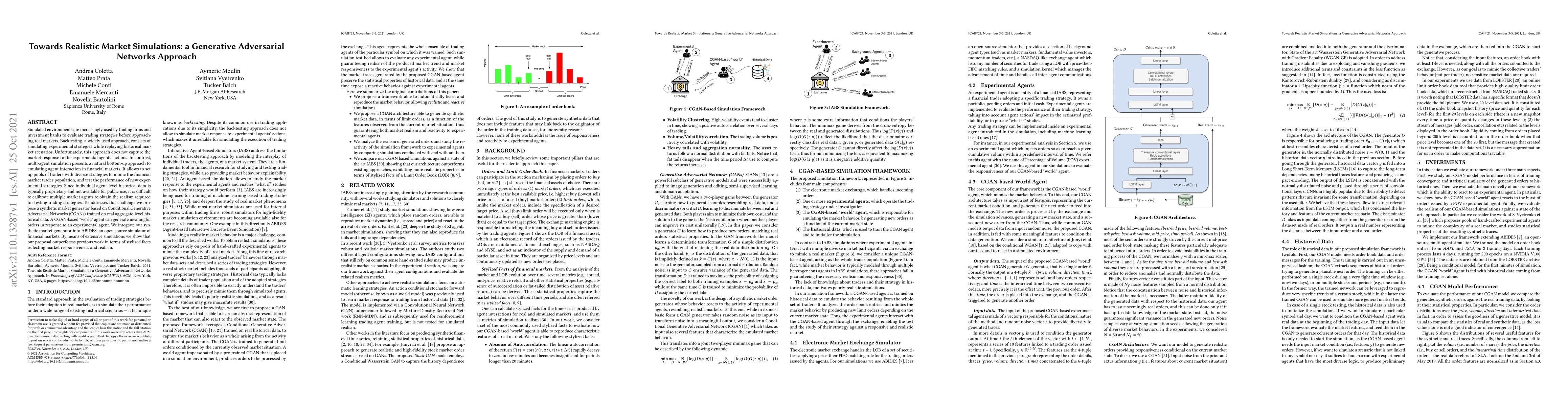

Simulated environments are increasingly used by trading firms and investment banks to evaluate trading strategies before approaching real markets. Backtesting, a widely used approach, consists of si...