Academic Profile

Statistics

Similar Authors

Papers on arXiv

We formulate a forward inflation index model with multi-factor volatility structure featuring a parametric form that allows calibration to correlations between indices of different tenors observed i...

We consider two data driven approaches, Reinforcement Learning (RL) and Deep Trajectory-based Stochastic Optimal Control (DTSOC) for hedging a European call option without and with transaction cost ...

We consider two data-driven approaches to hedging, Reinforcement Learning and Deep Trajectory-based Stochastic Optimal Control, under a stepwise mean-variance objective. We compare their performance...

Differential machine learning (DML) is a recently proposed technique that uses samplewise state derivatives to regularize least square fits to learn conditional expectations of functionals of stocha...

We propose a non-parametric extension with leverage functions to the Andersen commodity curve model. We calibrate this model to market data for WTI and NG including option skew at the standard matur...

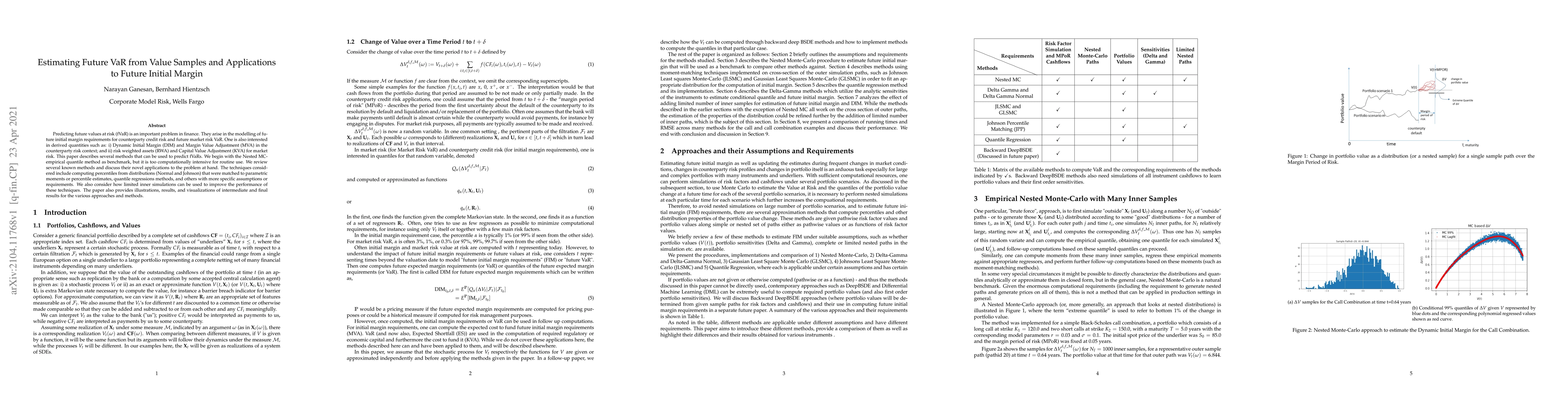

Predicting future values at risk (fVaR) is an important problem in finance. They arise in the modelling of future initial margin requirements for counterparty credit risk and future market risk VaR....

We propose Monte Carlo calibration algorithms for three models: local volatility with stochastic interest rates, stochastic local volatility with deterministic interest rates, and finally stochastic...

In this paper, we present a backward deep BSDE method applied to Forward Backward Stochastic Differential Equations (FBSDE) with given terminal condition at maturity that time-steps the BSDE backwar...

This paper presents a novel and direct approach to price boundary and final-value problems, corresponding to barrier options, using forward deep learning to solve forward-backward stochastic differe...

We derive generalizations of Dupire formula to the cases of general stochastic drift and/or stochastic local volatility. First, we handle a case in which the drift is given as difference of two stoc...

In this introductory paper, we discuss how quantitative finance problems under some common risk factor dynamics for some common instruments and approaches can be formulated as time-continuous or tim...

In [1], we calibrated a one-factor Cheyette SLV model with a local volatility that is linear in the benchmark forward rate and an uncorrelated CIR stochastic variance to 3M caplets of various maturiti...

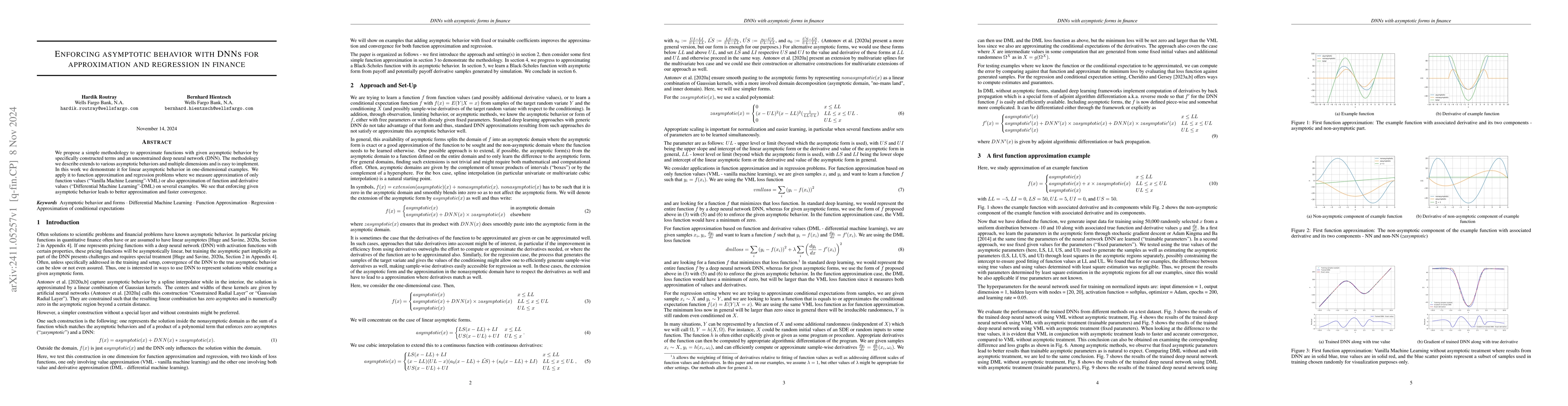

We propose a simple methodology to approximate functions with given asymptotic behavior by specifically constructed terms and an unconstrained deep neural network (DNN). The methodology we describe ...

Motivated by the need for efficient estimation of conditional expectations, we consider a least-squares function approximation problem with heavily polluted data. Existing methods that are powerful in...