Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper delves into the dynamics of asset pricing within Bachelier market model, elucidating the representation of risky asset price dynamics and the definition of riskless assets.

We extend the application of the Cherny-Shiryaev-Yor invariance principle to a unified Bachelier-Black-Scholes-Merton (BBSM) dynamic pricing model. This extension incorporates the influence of the his...

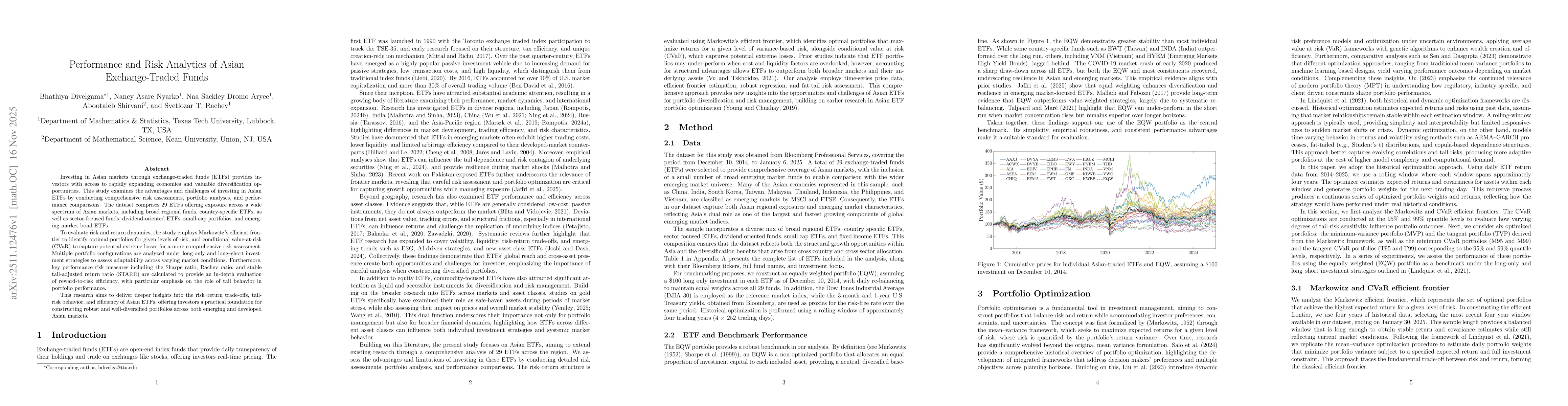

Investing in Asian markets through exchange-traded funds (ETFs) provides investors with access to rapidly expanding economies and valuable diversification opportunities. This study examines the advant...