Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the study of extremes, the presence of asymptotic independence signifies that extreme events across multiple variables are probably less likely to occur together. Although well-understood in a bi...

The stability of a complex financial system may be assessed by measuring risk contagion between various financial institutions with relatively high exposure. We consider a financial network model us...

We consider a model for multivariate data with heavy-tailed marginal distributions and a Gaussian dependence structure. The different marginals in the model are allowed to have non-identical tail be...

In this paper, we compute multivariate tail risk probabilities where the marginal risks are heavy-tailed and the dependence structure is a Gaussian copula. The marginal heavy-tailed risks are modele...

The tail behavior of aggregates of heavy-tailed random vectors is known to be determined by the so-called principle of "one large jump'', be it for finite sums, random sums, or, L\'evy processes. We...

Random network models generated using sparse exchangeable graphs have provided a mechanism to study a wide variety of complex real-life networks. In particular, these models help with investigating ...

The number of common friends (or connections) in a graph is a commonly used measure of proximity between two nodes. Such measures are used in link prediction algorithms and recommendation systems in...

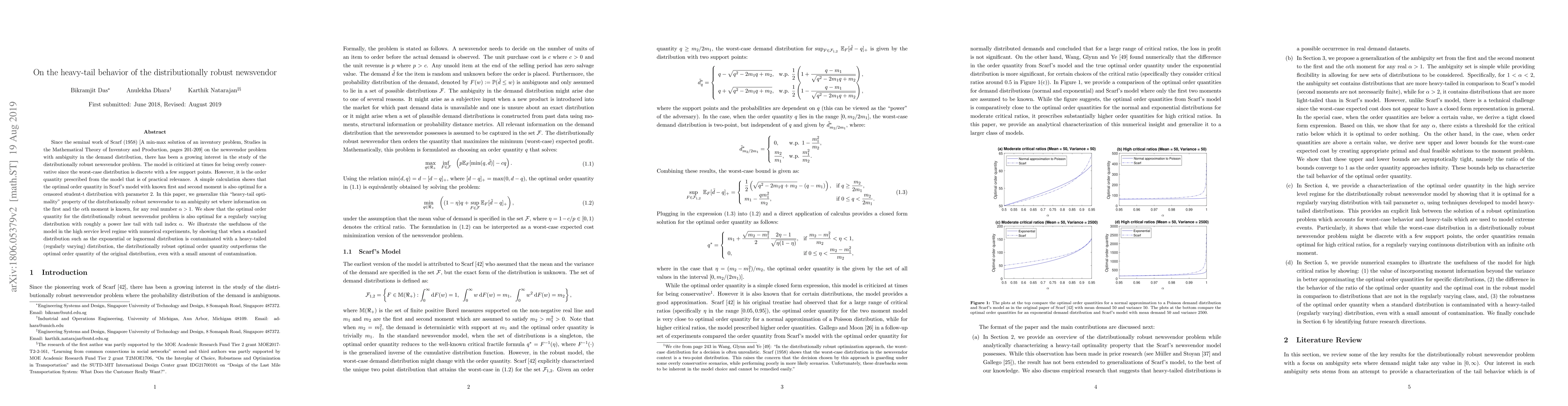

Since the seminal work of Scarf (1958) [A min-max solution of an inventory problem, Studies in the Mathematical Theory of Inventory and Production, pages 201-209] on the newsvendor problem with ambi...

Measures of risk concentration and their asymptotic behavior for portfolios with heavy-tailed risk factors is of interest in risk management. Second order regular variation is a structural assumptio...

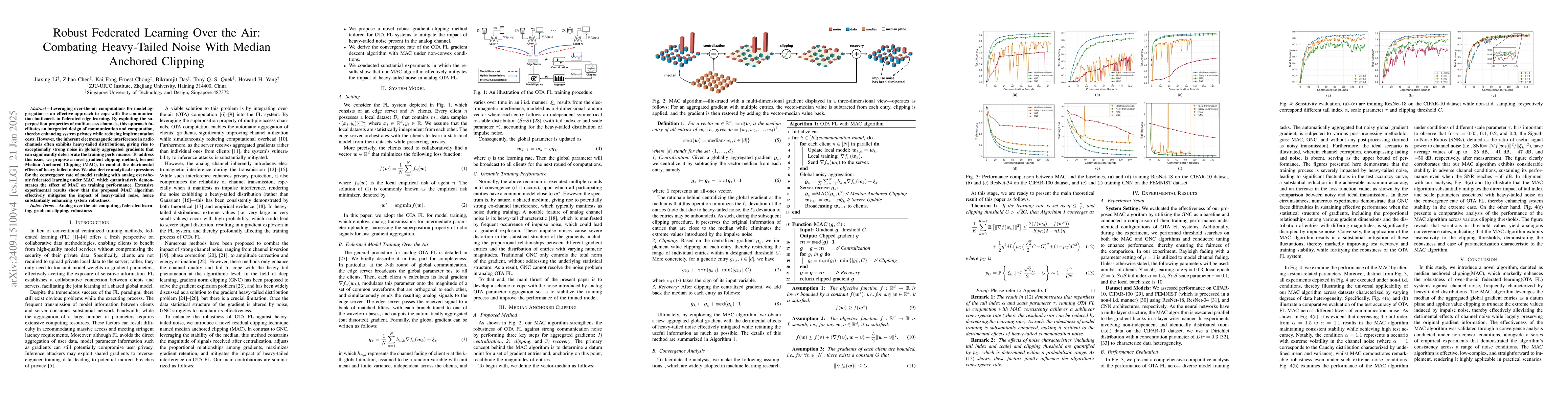

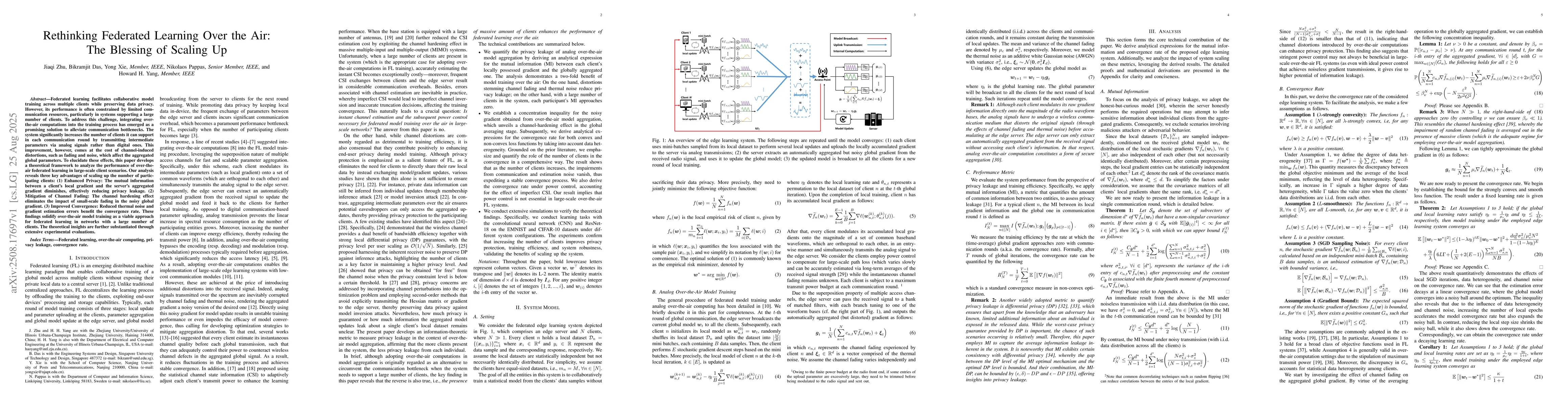

Leveraging over-the-air computations for model aggregation is an effective approach to cope with the communication bottleneck in federated edge learning. By exploiting the superposition properties of ...

Federated learning facilitates collaborative model training across multiple clients while preserving data privacy. However, its performance is often constrained by limited communication resources, par...

Bitcoin mining hardware acquisition requires strategic timing due to volatile markets, rapid technological obsolescence, and protocol-driven revenue cycles. Despite mining's evolution into a capital-i...

Simultaneous occurrences of extreme events need not imply symmetric or reciprocal tail dependence. However, most existing measures of extremal dependence are inherently symmetric and hence often fail ...