Academic Profile

Statistics

Similar Authors

Papers on arXiv

We model investor heterogeneity using different required returns on an investment and evaluate the impact on the valuation of an investment. By assuming no disagreement on the cash flows, we emphasi...

How do supply and demand from informed traders drive market prices of bitcoin options? Deribit options tick-level data supports the limits-to-arbitrage hypothesis about the market maker's supply. Th...

Over 90% of exchange trading on crypto options has always been on the Deribit platform. This centralised crypto exchange only lists inverse products because they do not accept fiat currency. Current...

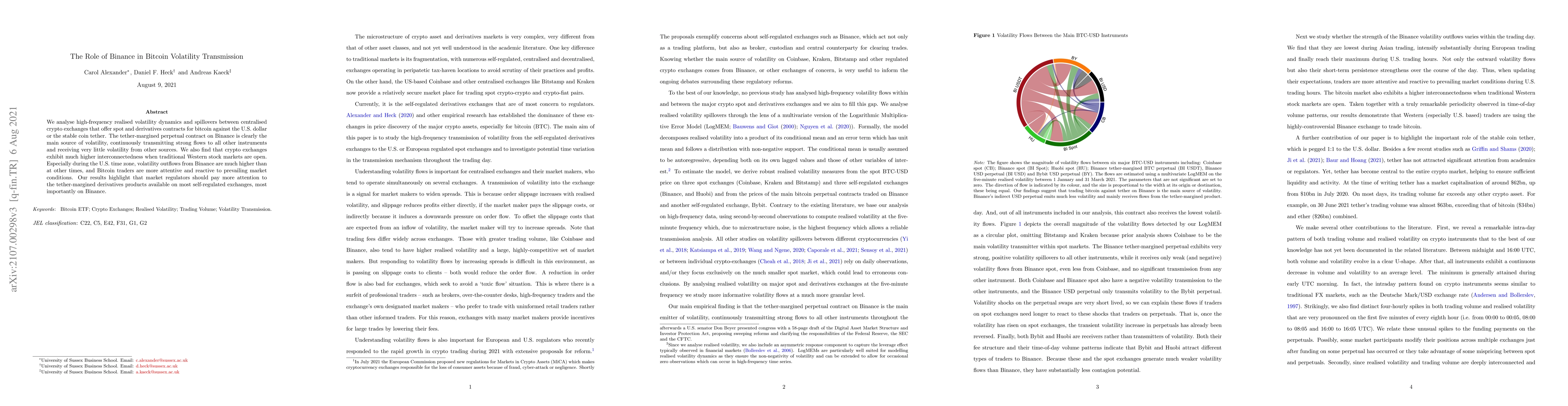

We analyse high-frequency realised volatility dynamics and spillovers in the bitcoin market, focusing on two pairs: bitcoin against the US dollar (the main fiat-crypto pair) and trading bitcoin agai...

Proper scoring rules are commonly applied to quantify the accuracy of distribution forecasts. Given an observation they assign a scalar score to each distribution forecast, with the the lowest expec...

A plethora of static and dynamic models exist to forecast Value-at-Risk and other quantile-related metrics used in financial risk management. Industry practice tends to favour simpler, static models...

Modelling multivariate systems is important for many applications in engineering and operational research. The multivariate distributions under scrutiny usually have no analytic or closed form. Ther...

This study investigates the inherently random structures of dry bulk shipping networks, often likened to a taxi service, and identifies the underlying trade dynamics that contribute to this randomness...