Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a novel quantum high-dimensional linear regression algorithm with an $\ell_1$-penalty based on the classical LARS (Least Angle Regression) pathwise algorithm. Similarly to available classic...

This paper studies the well-posedness of a class of nonlocal parabolic partial differential equations (PDEs), or equivalently equilibrium Hamilton-Jacobi-Bellman equations, which has a strong tie wi...

This paper studies robust time-inconsistent (TIC) linear-quadratic stochastic control problems, formulated by stochastic differential games. By a spike variation approach, we derive sufficient condi...

In this paper, we propose quasilinearization methods that convert nonlocal fully-nonlinear parabolic systems into the nonlocal quasilinear parabolic systems. The nonlocal parabolic systems serve as ...

This paper proves the existence and uniqueness results (in the sense of maximally defined regularity) as well as the stability analysis for the solutions to a class of nonlocal fully-nonlinear parab...

In this paper, we establish a subgame perfect equilibrium reinforcement learning (SPERL) framework for time-inconsistent (TIC) problems. In the context of RL, TIC problems are known to face two main...

We prove the well-posedness results, i.e. existence, uniqueness, and stability, of the solutions to a class of nonlocal fully nonlinear parabolic partial differential equations (PDEs), where there i...

Social distancing has been the only effective way to contain the spread of an infectious disease prior to the availability of the pharmaceutical treatment. It can lower the infection rate of the dis...

In this paper, we establish existence, uniqueness, and regularity properties of the solutions to multi-dimensional backward stochastic Volterra integral equations (BSVIEs), whose (possibly random) gen...

This paper studies dynamic mean-variance (MV) asset allocation problems in general incomplete markets. Besides of the conventional MV objective on portfolio's terminal wealth, our framework can accomm...

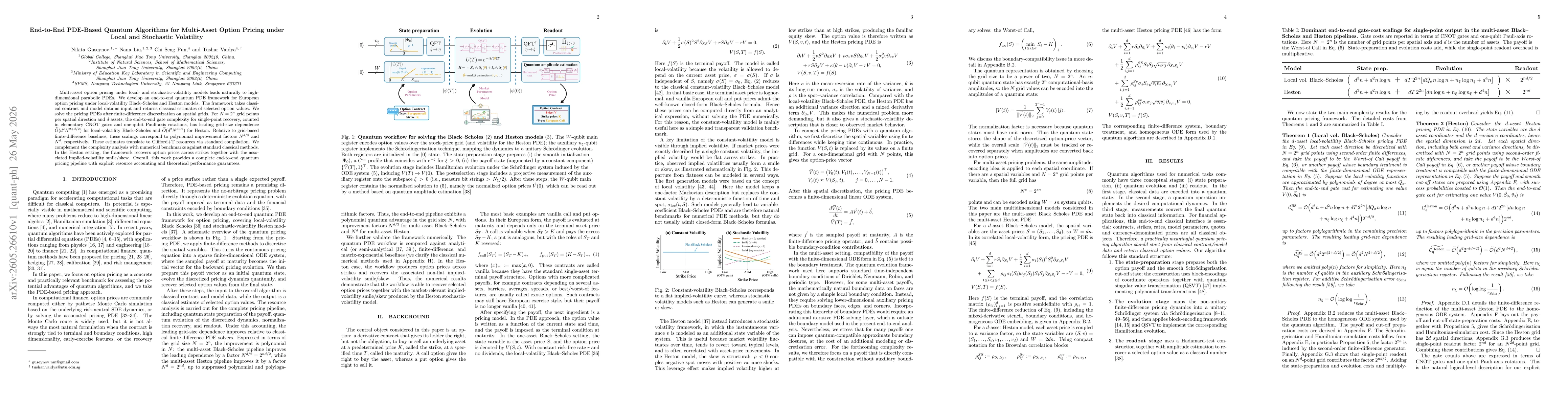

Multi-asset option pricing under local- and stochastic-volatility models leads naturally to high-dimensional parabolic PDEs. We develop an end-to-end quantum PDE framework for European option pricing ...