Academic Profile

Statistics

Similar Authors

Papers on arXiv

We establish a negative moment bound for the sample autocovariance matrix of a stationary process driven by conditional heteroscedastic errors. This moment bound enables us to asymptotically express...

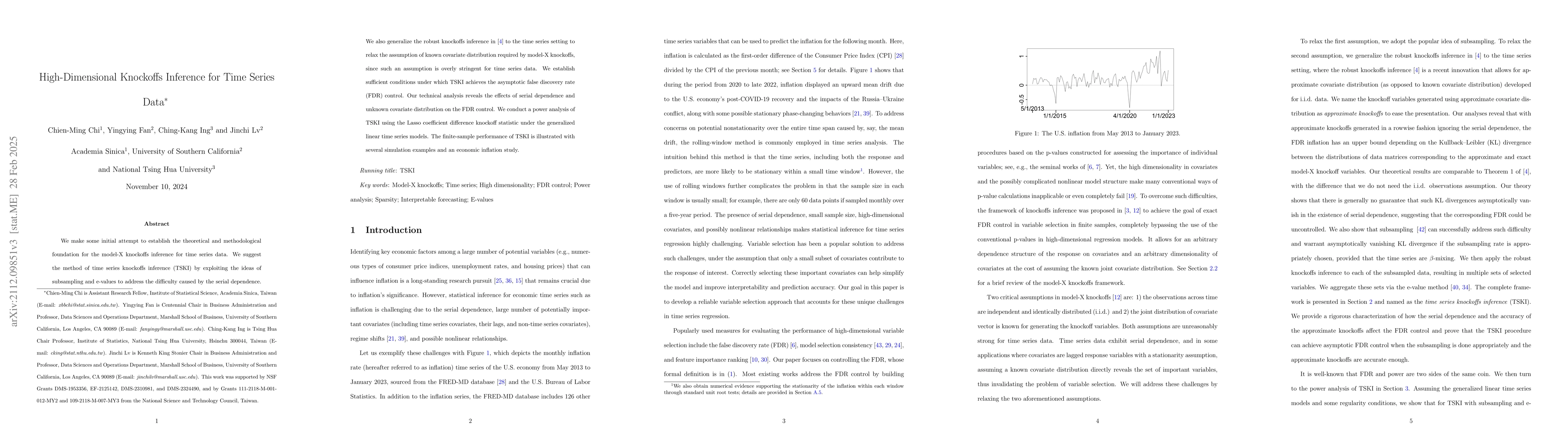

The model-X knockoffs framework provides a flexible tool for achieving finite-sample false discovery rate (FDR) control in variable selection in arbitrary dimensions without assuming any dependence ...

We consider a linear mixed-effects model with a clustered structure, where the parameters are estimated using maximum likelihood (ML) based on possibly unbalanced data. Inference with this model is ...

We investigate the prediction capability of the orthogonal greedy algorithm (OGA) in high-dimensional regression models with dependent observations. The rates of convergence of the prediction error ...

This paper studies model selection for general unit-root time series, including the case with many exogenous predictors. We propose FHTD, a new model selection algorithm that leverages forward stepwis...

Imori and Ing (2025) proposed the importance-weighted orthogonal greedy algorithm (IWOGA) for model selection in high-dimensional misspecified regression models under covariate shift. To determine the...