Academic Profile

Statistics

Similar Authors

Papers on arXiv

Maximal Extractable Value (MEV) in Constant Function Market Making is fairly well understood. Does having dynamic weights, as found in liquidity boostrap pools (LBPs), Temporal-function market maker...

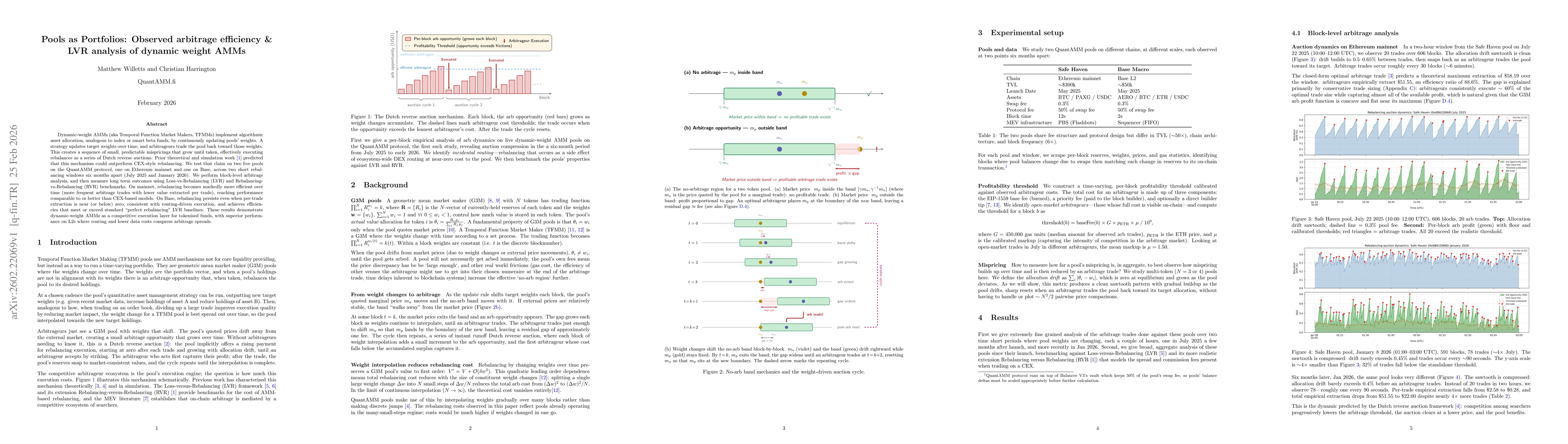

Dynamic AMM pools, as found in Temporal Function Market Making, rebalance their holdings to a new desired ratio (e.g. moving from being 50-50 between two assets to being 90-10 in favour of one of th...

Convex optimisation has provided a mechanism to determine arbitrage trades on automated market markets (AMMs) since almost their inception. Here we outline generic closed-form solutions for $N$-toke...

Automated Market Makers (AMMs) hold assets and are constantly being rebalanced by external arbitrageurs to match external market prices. Loss-versus-rebalancing (LVR) is a pivotal metric for measuring...

Dynamic-weight AMMs (aka Temporal Function Market Makers, TFMMs) implement algorithmic asset allocation, analogous to index or smart beta funds, by continuously updating pools' weights. A strategy upd...