Academic Profile

Statistics

Similar Authors

Papers on arXiv

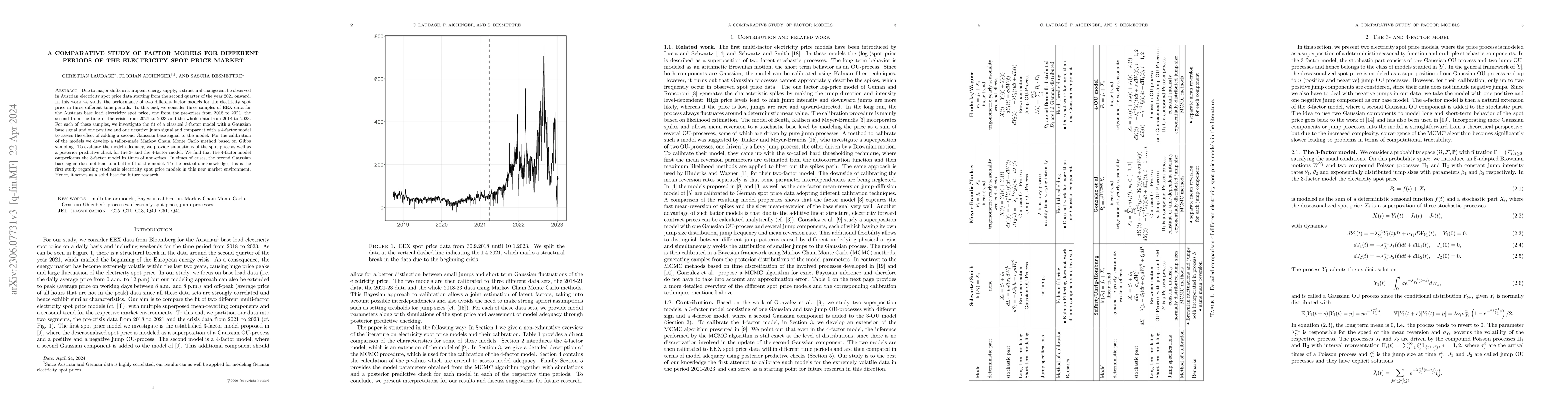

Due to major shifts in European energy supply, a structural change can be observed in Austrian electricity spot price data starting from the second quarter of the year 2021 onward. In this work we s...

Risk measures are important key figures to measure the adequacy of the reserves of a company. The most common risk measures in practice are Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). ...

We revisit the recently introduced concept of return risk measures (RRMs). We extend it by allowing risk management via multiple so-called eligible assets. The resulting new risk measures are called m...

We address the problem that classical risk measures may not detect the tail risk adequately. This can occur for instance due to the averaging process when computing Expected Shortfall. The current lit...

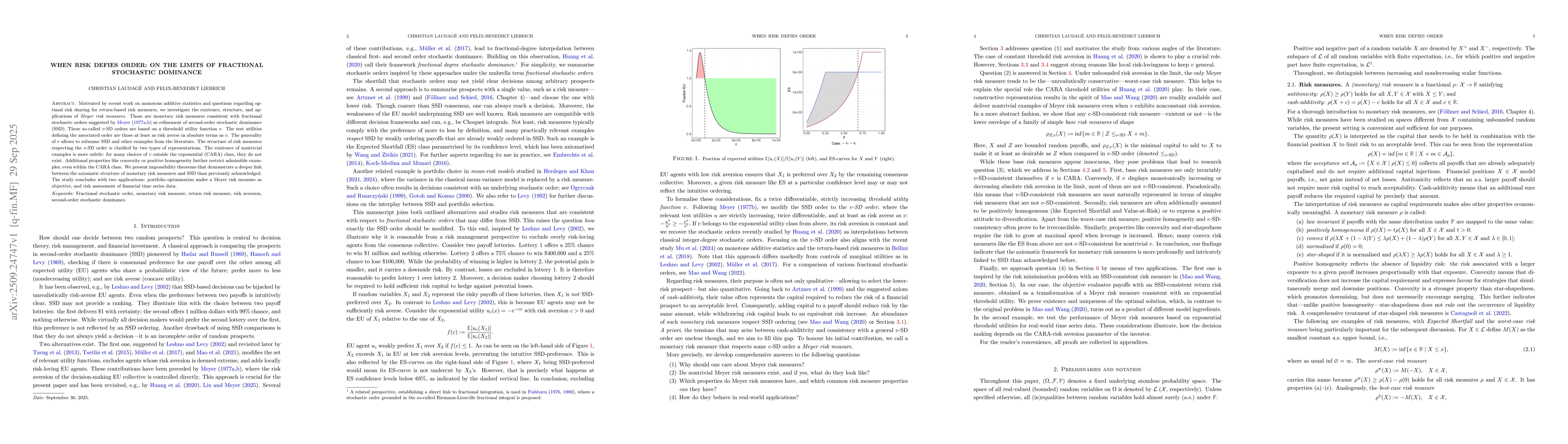

Motivated by recent work on monotone additive statistics and questions regarding optimal risk sharing for return-based risk measures, we investigate the existence, structure, and applications of Meyer...

Under Solvency II, the Value-at-Risk (VaR) is applied, although there is broad consensus that the Expected Shortfall (ES) constitutes a more appropriate measure. Moving towards ES would necessitate sp...

Monetary risk measures quantify the risk of uncertain monetary payoffs (or losses), whereas in time series analysis risk is typically assessed using logarithmic returns. Return risk measures (RRMs) pr...