Academic Profile

Statistics

Similar Authors

Papers on arXiv

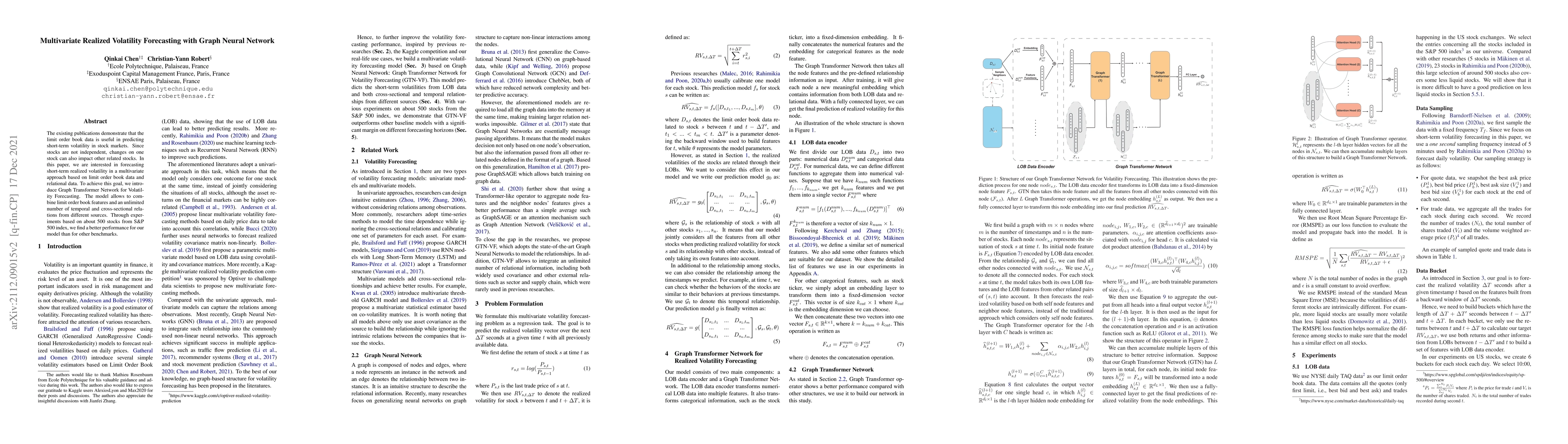

The existing publications demonstrate that the limit order book data is useful in predicting short-term volatility in stock markets. Since stocks are not independent, changes on one stock can also i...

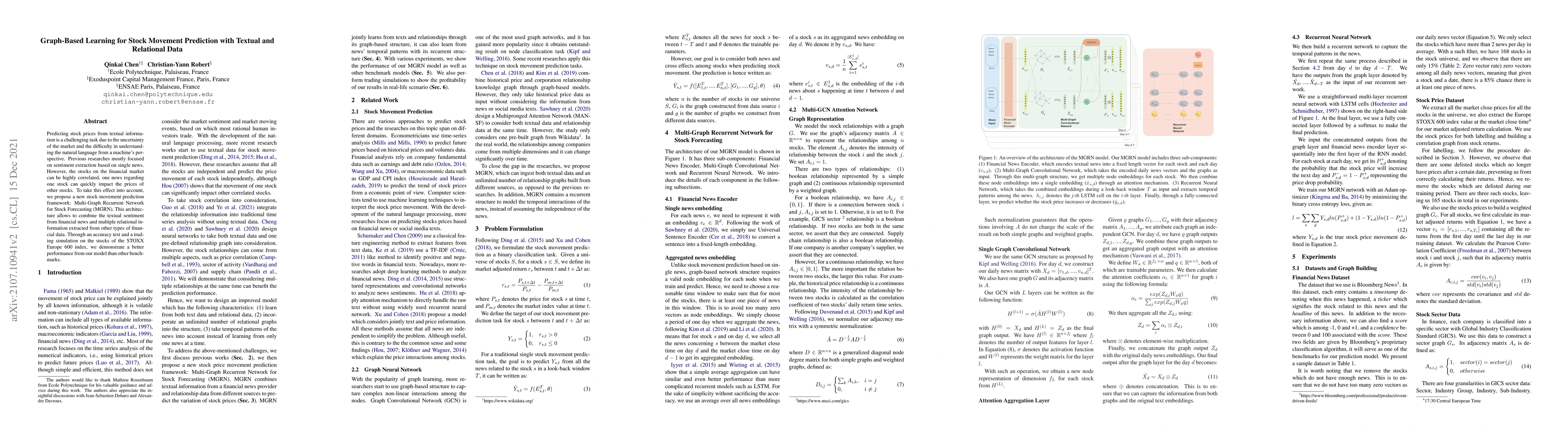

Predicting stock prices from textual information is a challenging task due to the uncertainty of the market and the difficulty understanding the natural language from a machine's perspective. Previo...

Hourly maxima of 3-second wind gust speeds are prominent indicators of the severity of wind storms, and accurately forecasting them is thus essential for populations, civil authorities and insurance c...

This paper considers one-dimensional mixed causal/noncausal autoregressive (MAR) processes with heavy tail, usually introduced to model trajectories with patterns including asymmetric peaks and throug...