Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce the matrix-valued time-varying Main Effects Factor Model (MEFM). MEFM is a generalization to the traditional matrix-valued factor model (FM). We give rigorous definitions of MEFM and it...

Most factor modelling research in vector or matrix-valued time series assume all factors are pervasive/strong and leave weaker factors and their corresponding series to the noise. Weaker factors can...

We propose tensor time series imputation when the missing pattern in the tensor data can be general, as long as any two data positions along a tensor fibre are both observed for enough time points. ...

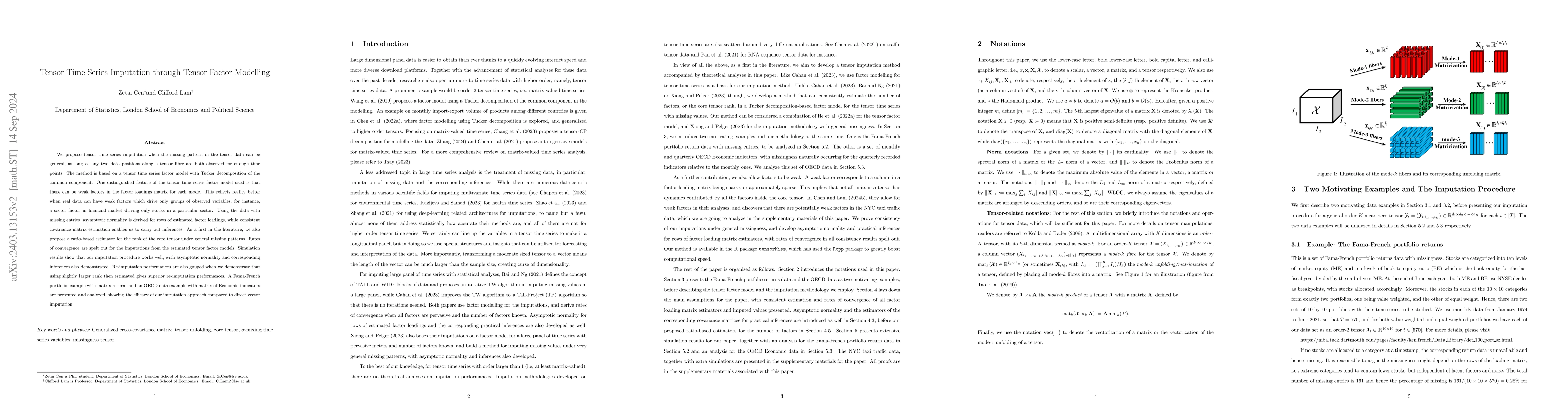

Tensor time series data appears naturally in a lot of fields, including finance and economics. As a major dimension reduction tool, similar to its factor model counterpart, the idiosyncratic compone...

We analyze a varying-coefficient dynamic spatial autoregressive model with spatial fixed effects. One salient feature of the model is the incorporation of multiple spatial weight matrices through thei...

We propose a test for testing the Kronecker product structure of a factor loading matrix implied by a tensor factor model with Tucker decomposition in the common component. Through defining a Kronecke...

We introduce sparsity detection and estimation in main effect matrix factor models for matrix-valued time series. A carefully chosen set of identification conditions for the common component and the p...