Academic Profile

Statistics

Similar Authors

Papers on arXiv

We investigate sample-based learning of conditional distributions on multi-dimensional unit boxes, allowing for different dimensions of the feature and target spaces. Our approach involves clusterin...

We consider the multiple quantile hedging problem, which is a class of partial hedging problems containing as special examples the quantile hedging problem (F{\"o}llmer \& Leukert 1999) and the PnL ...

Darwinian model risk is the risk of mis-price-and-hedge biased toward short-to-medium systematic profits of a trader, which are only the compensator of long term losses becoming apparent under extre...

The dynamic hedging theory only makes sense in the setup of one given model, whereas the practice of dynamic hedging is just the opposite, with models fleeing after the data through daily recalibrat...

We introduce and study a new class of optimal switching problems, namely switching problem with controlled randomisation, where some extra-randomness impacts the choice of switching modes and associ...

We consider the numerical approximation of the quantile hedging price in a non-linear market. In a Markovian framework, we propose a numerical method based on a Piecewise Constant Policy Timesteppin...

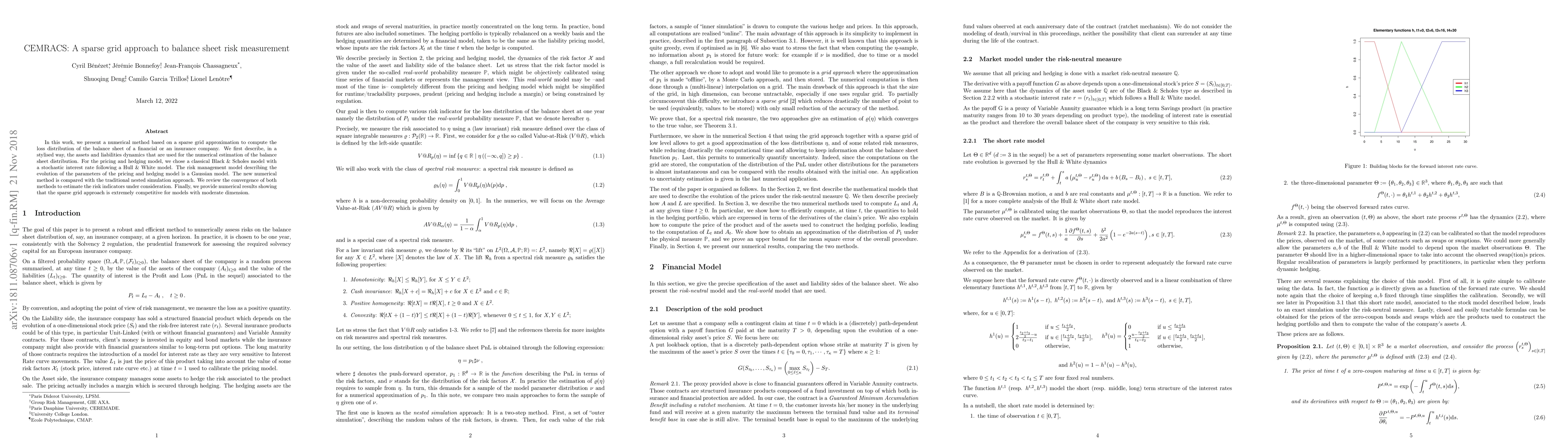

In this work, we present a numerical method based on a sparse grid approximation to compute the loss distribution of the balance sheet of a financial or an insurance company. We first describe, in a...