Academic Profile

Statistics

Similar Authors

Papers on arXiv

GARCH-type time series (characterized by Generalized Autoregressive Conditional Heteroskedasticity) exhibit pronounced volatility, autocorrelation, and heteroskedasticity. To address these challenges ...

Biclustering is an effective technique in data mining and pattern recognition. Biclustering algorithms based on traditional clustering face two fundamental limitations when processing high-dimensional...

Existing edge detection methods often suffer from noise amplification and excessive retention of non-salient details, limiting their applicability in high-precision industrial scenarios. To address th...

Edge detection is crucial in image processing, but existing methods often produce overly detailed edge maps, affecting clarity. Fixed-window statistical testing faces issues like scale mismatch and co...

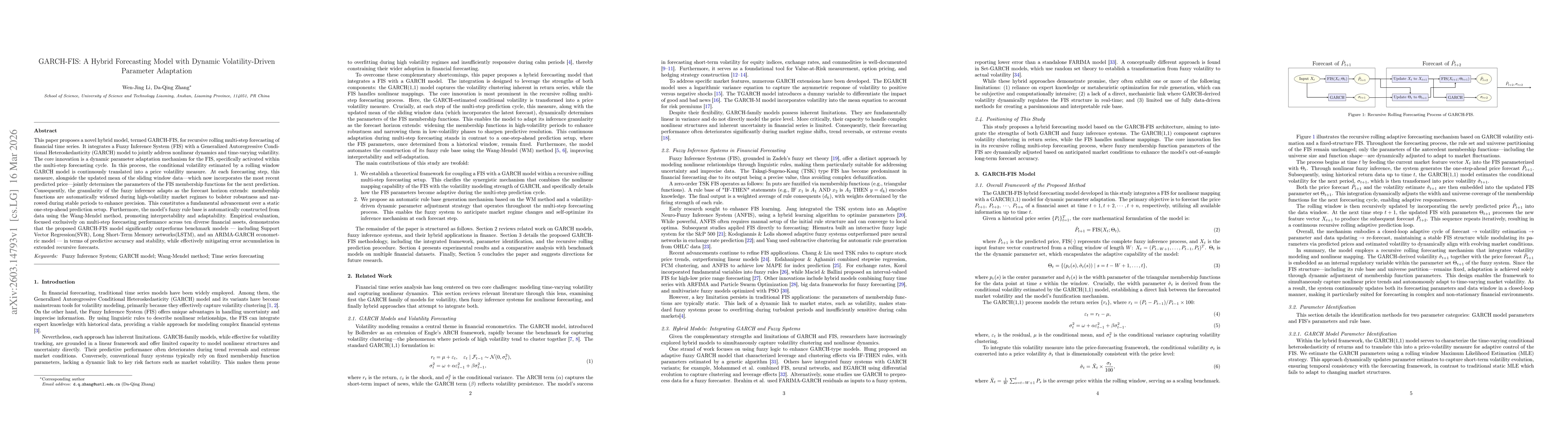

This paper proposes a novel hybrid model, termed GARCH-FIS, for recursive rolling multi-step forecasting of financial time series. It integrates a Fuzzy Inference System (FIS) with a Generalized Autor...

This paper presents Orthogonal Subspace Clustering (OSC), an innovative method for high-dimensional data clustering. We first establish a theoretical theorem proving that high-dimensional data can be ...

This paper introduces a novel variational Bayesian method that integrates Tucker decomposition for efficient high-dimensional inverse problem solving. The method reduces computational complexity by tr...