Academic Profile

Statistics

Similar Authors

Papers on arXiv

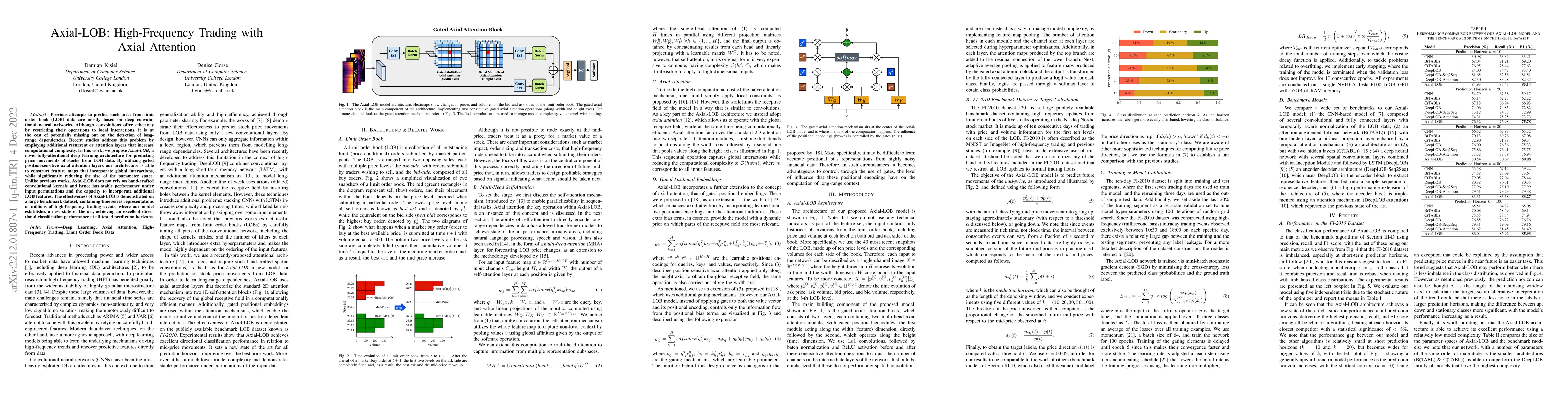

Previous attempts to predict stock price from limit order book (LOB) data are mostly based on deep convolutional neural networks. Although convolutions offer efficiency by restricting their operatio...

Traditional approaches to financial asset allocation start with returns forecasting followed by an optimization stage that decides the optimal asset weights. Any errors made during the forecasting s...

This work proposes a novel portfolio management technique, the Meta Portfolio Method (MPM), inspired by the successes of meta approaches in the field of bioinformatics and elsewhere. The MPM uses XG...