Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (C...

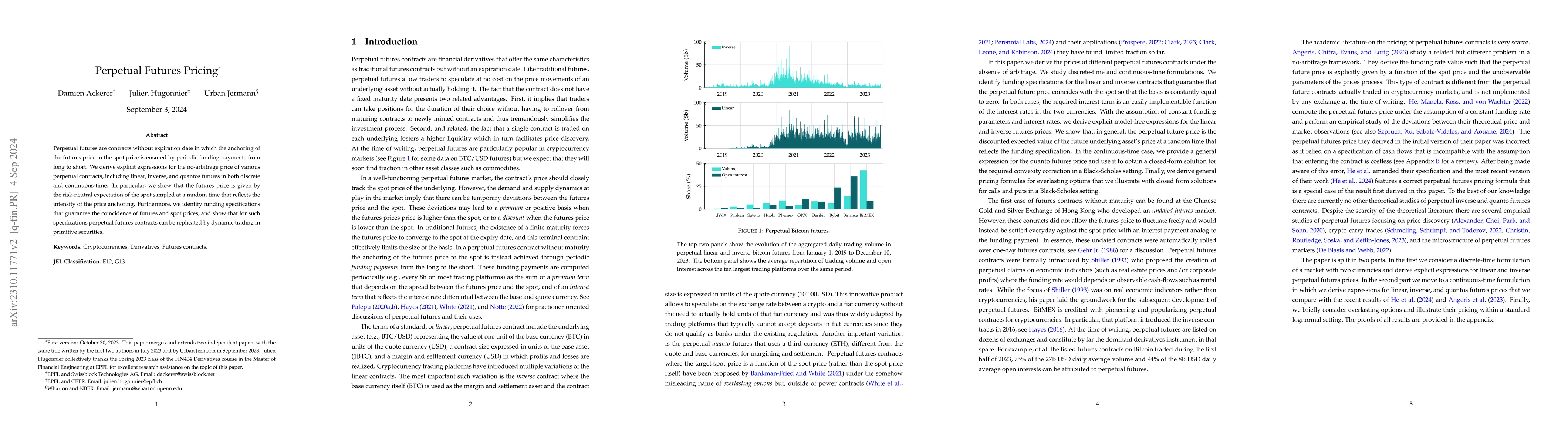

Perpetual futures are contracts without expiration date in which the anchoring of the futures price to the spot price is ensured by periodic funding payments from long to short. We derive explicit e...

We propose a game-theoretic framework to study the outcomes of packetized payments, a cross-ledger transaction protocol, with strategic and possibly malicious agents. We derive the transaction failu...

To achieve interoperability between unconnected ledgers, hash time lock contracts (HTLCs) are commonly used for cross-chain asset exchange. The solution tolerates transaction failure, and can "make ...

We introduce the vine copula autoencoder (VCAE), a flexible generative model for high-dimensional distributions built in a straightforward three-step procedure. First, an autoencoder (AE) compress...

We present a neural network (NN) approach to fit and predict implied volatility surfaces (IVSs). Atypically to standard NN applications, financial industry practitioners use such models equally to r...