Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present first results from the use of XGBoost, a highly effective machine learning (ML) method, within the Bristol Betting Exchange (BBE), an open-source agent-based model (ABM) designed to simul...

We report on a series of experiments in which we study the coevolutionary "arms-race" dynamics among groups of agents that engage in adaptive automated trading in an accurate model of contemporary f...

We describe three independent implementations of a new agent-based model (ABM) that simulates a contemporary sports-betting exchange, such as those offered commercially by companies including Betfai...

I describe the rationale for, and design of, an agent-based simulation model of a contemporary online sports-betting exchange: such exchanges, closely related to the exchange mechanisms at the heart...

I introduce PRZI (Parameterised-Response Zero Intelligence), a new form of zero-intelligence trader intended for use in simulation studies of the dynamics of continuous double auction markets. Like ...

We consider issues of time in automated trading strategies in simulated financial markets containing a single exchange with public limit order book and continuous double auction matching. In particu...

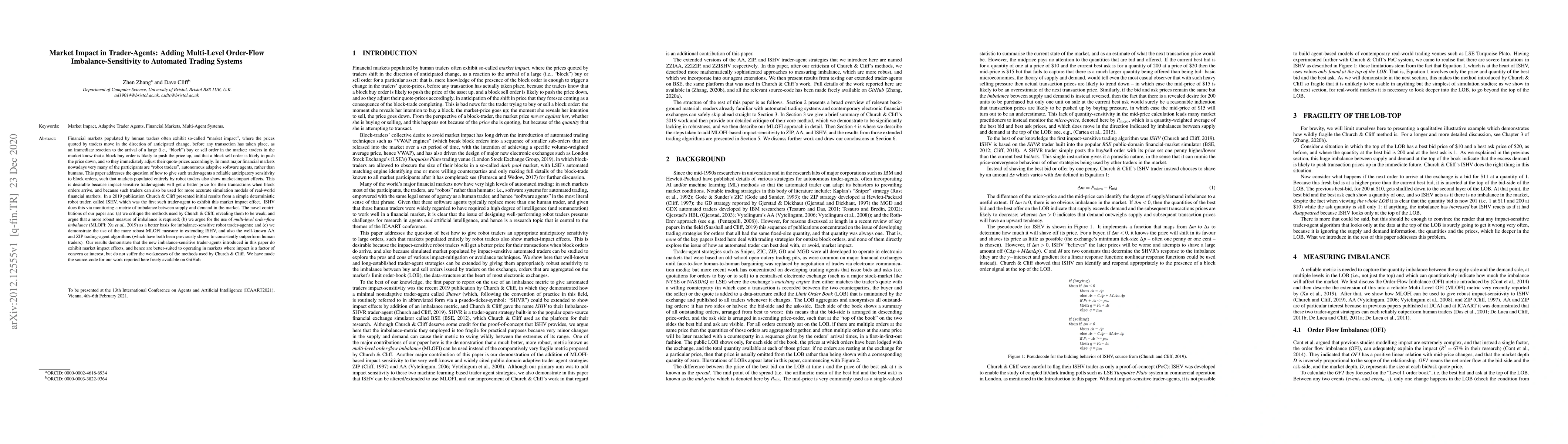

Financial markets populated by human traders often exhibit "market impact", where the traders' quote-prices move in the direction of anticipated change, before any transaction has taken place, as an...

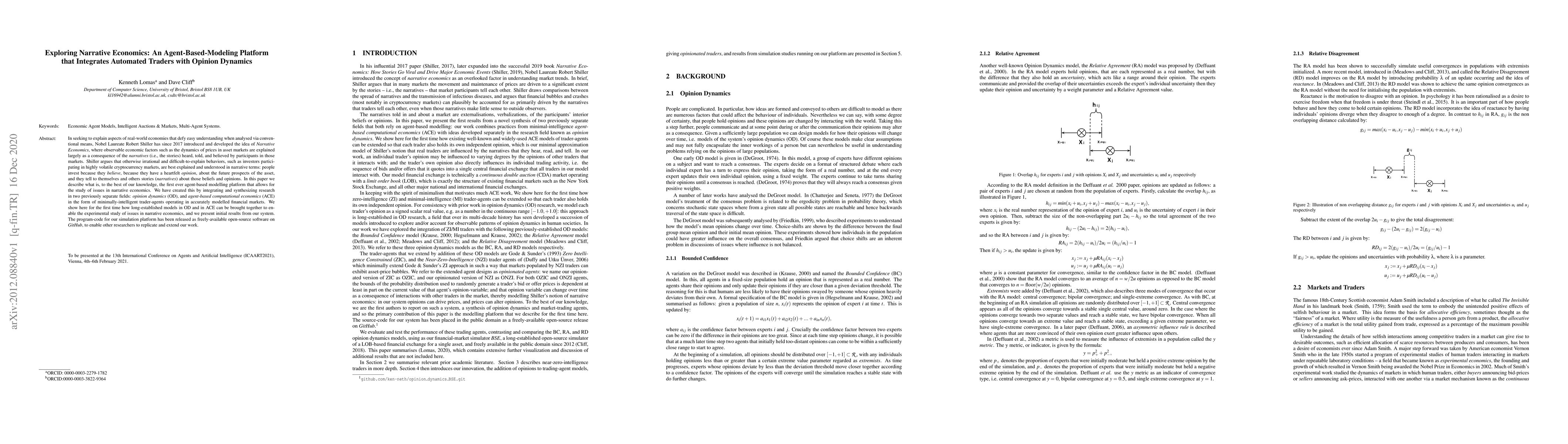

In seeking to explain aspects of real-world economies that defy easy understanding when analysed via conventional means, Nobel Laureate Robert Shiller has since 2017 introduced and developed the ide...

We present results demonstrating that an appropriately configured deep learning neural network (DLNN) can automatically learn to be a high-performing algorithmic trading system, operating purely fro...

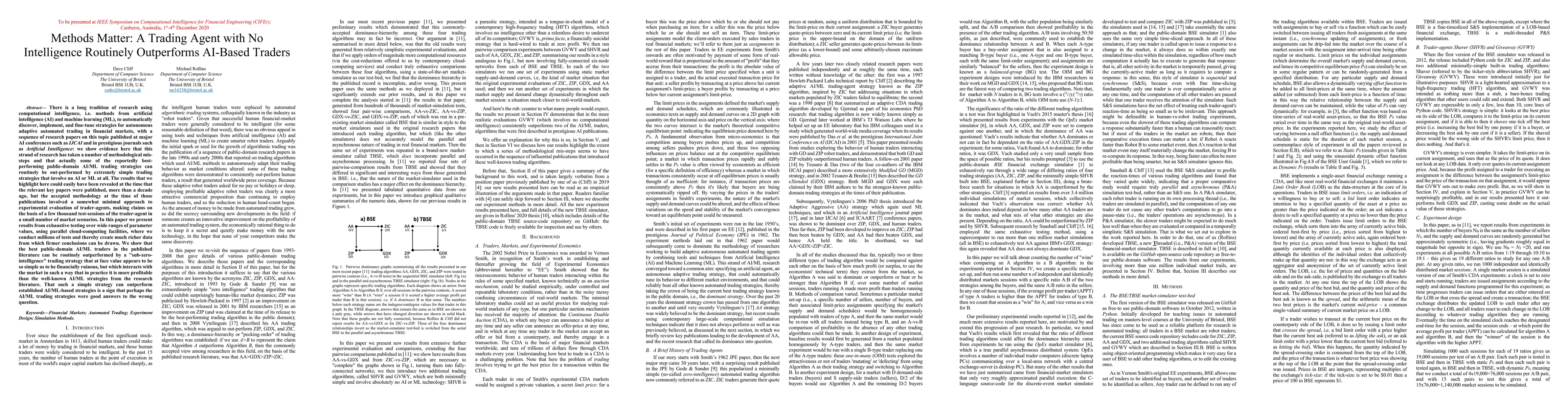

There's a long tradition of research using computational intelligence (methods from artificial intelligence (AI) and machine learning (ML)), to automatically discover, implement, and fine-tune strat...

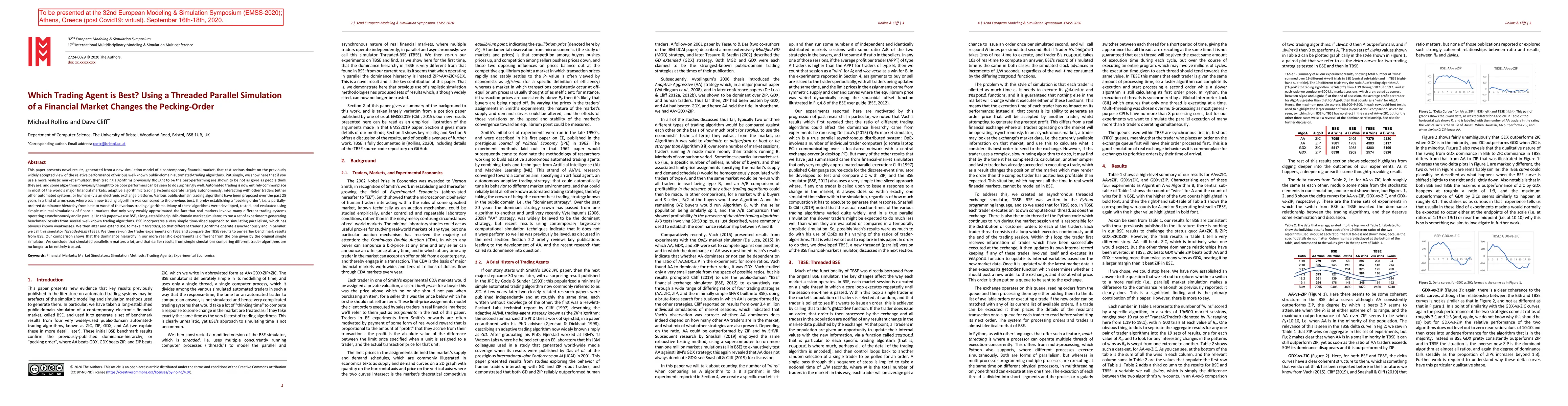

This paper presents novel results generated from a new simulation model of a contemporary financial market, that cast serious doubt on the previously widely accepted view of the relative performance...

For more than a decade Vytelingum's Adaptive-Aggressive (AA) algorithm has been recognized as the best-performing automated auction-market trading-agent strategy currently known in the AI/Agents lit...

We describe the implementation of and early results from a system that automatically composes picture-synched musical soundtracks for videos and movies. We use the phrase "picture-synched" to mean t...

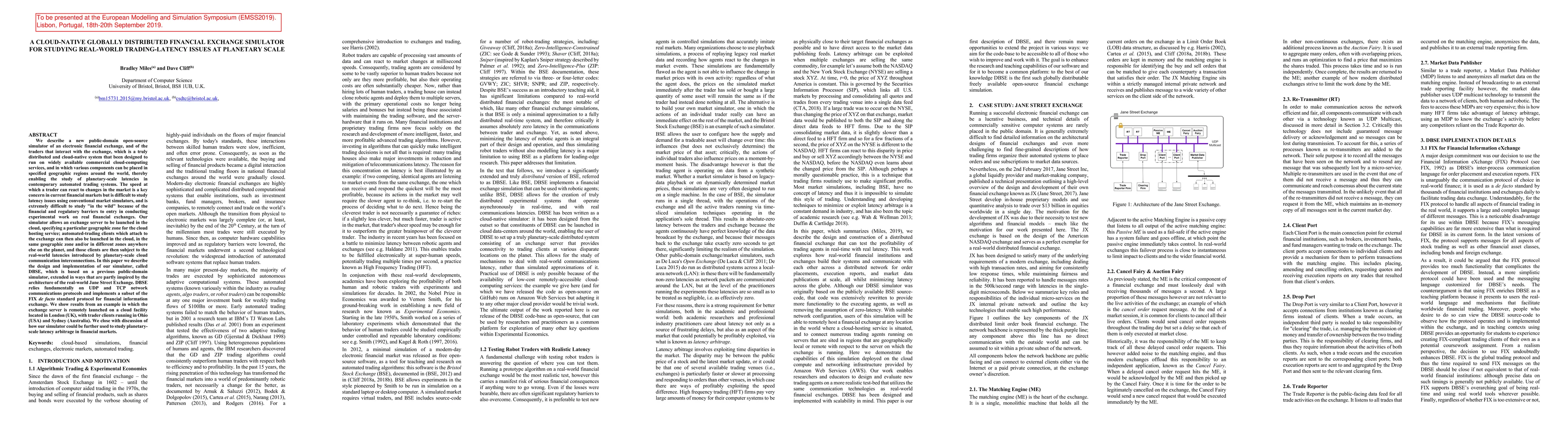

We describe a new public-domain open-source simulator of an electronic financial exchange, and of the traders that interact with the exchange, which is a truly distributed and cloud-native system th...

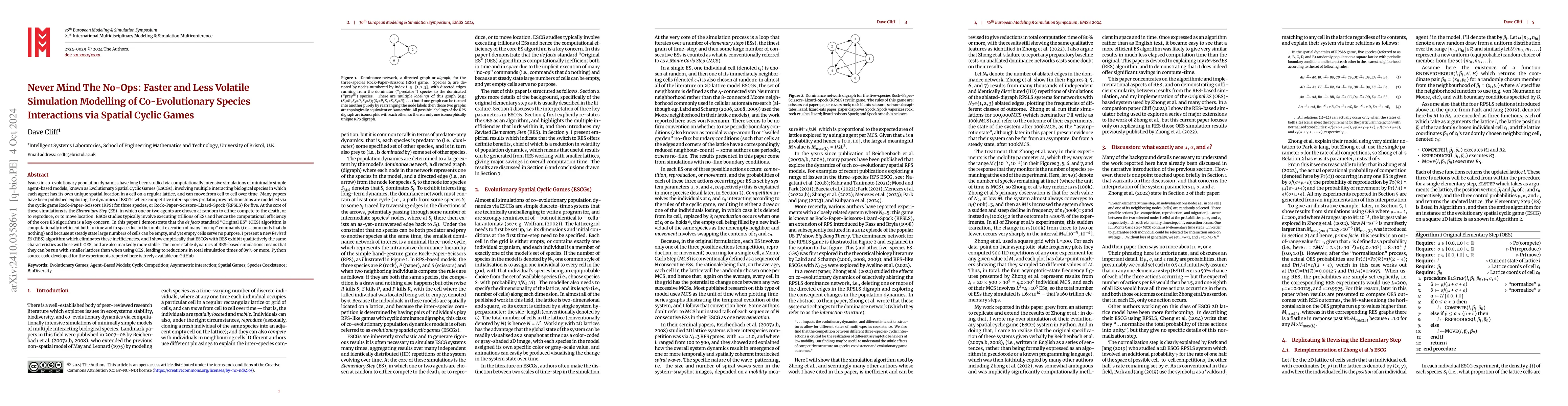

I present a replication and, to some extent, a refutation of key results published by Zhong, Zhang, Li, Dai, & Yang in their 2022 paper "Species coexistence in spatial cyclic game of five species" (Ch...

Issues in co-evolutionary population dynamics have long been studied via computationally intensive simulations of minimally simple agent-based models, known as Evolutionary Spatial Cyclic Games (ESCGs...

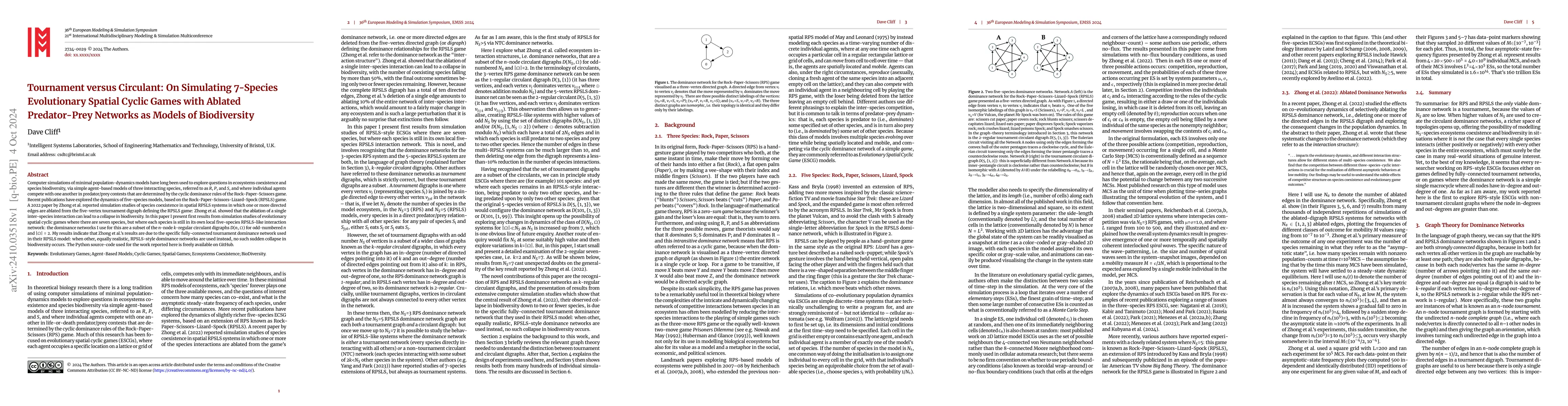

Computer simulations of minimal population-dynamics models have long been used to explore questions in ecosystems coexistence and species biodiversity, via simple agent-based models of three interacti...