Academic Profile

Statistics

Similar Authors

Papers on arXiv

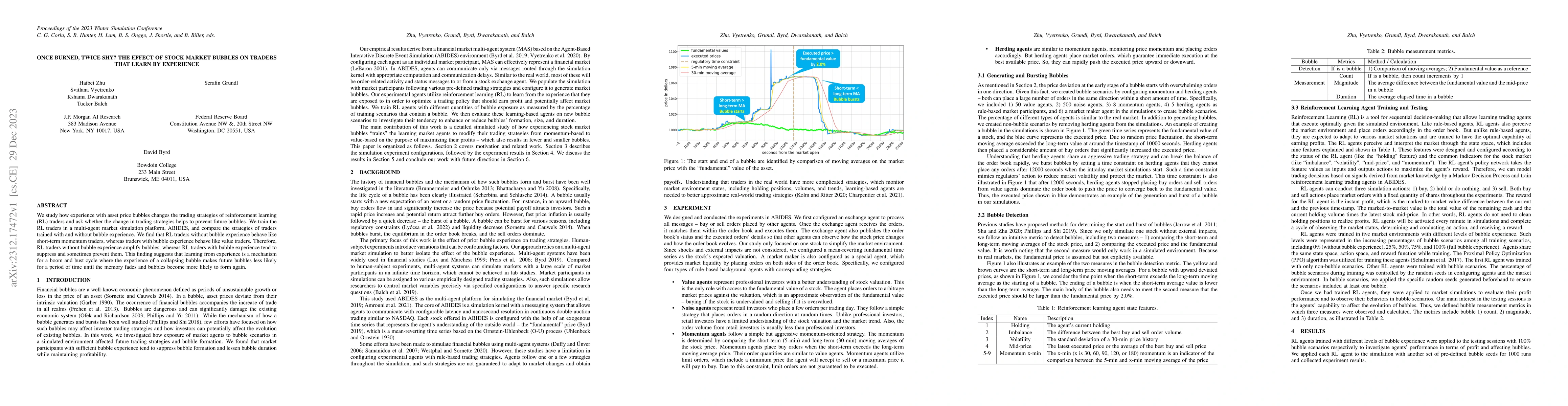

We study how experience with asset price bubbles changes the trading strategies of reinforcement learning (RL) traders and ask whether the change in trading strategies helps to prevent future bubble...

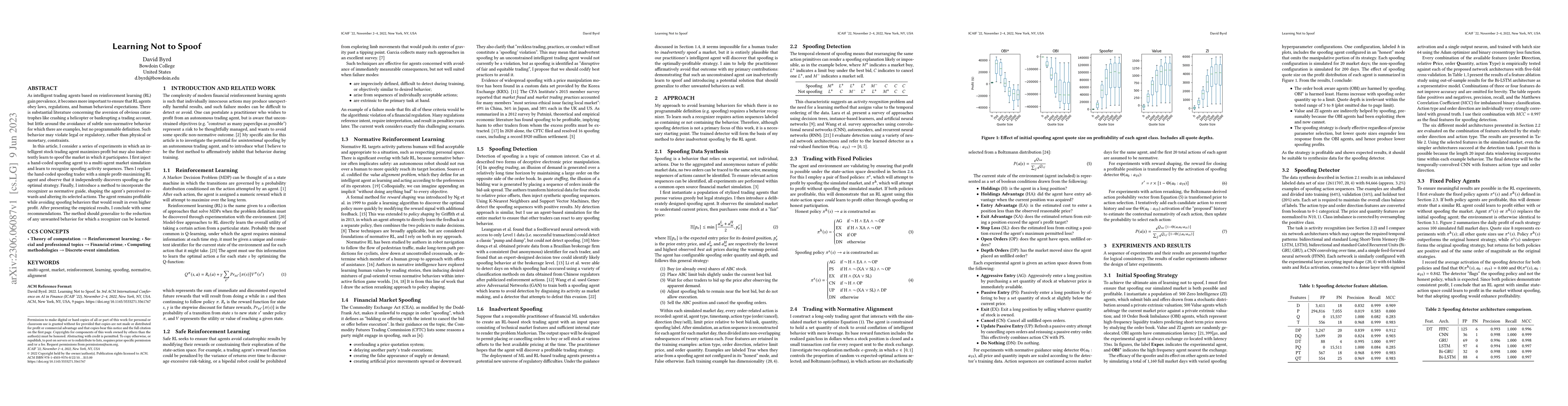

As intelligent trading agents based on reinforcement learning (RL) gain prevalence, it becomes more important to ensure that RL agents obey laws, regulations, and human behavioral expectations. Ther...

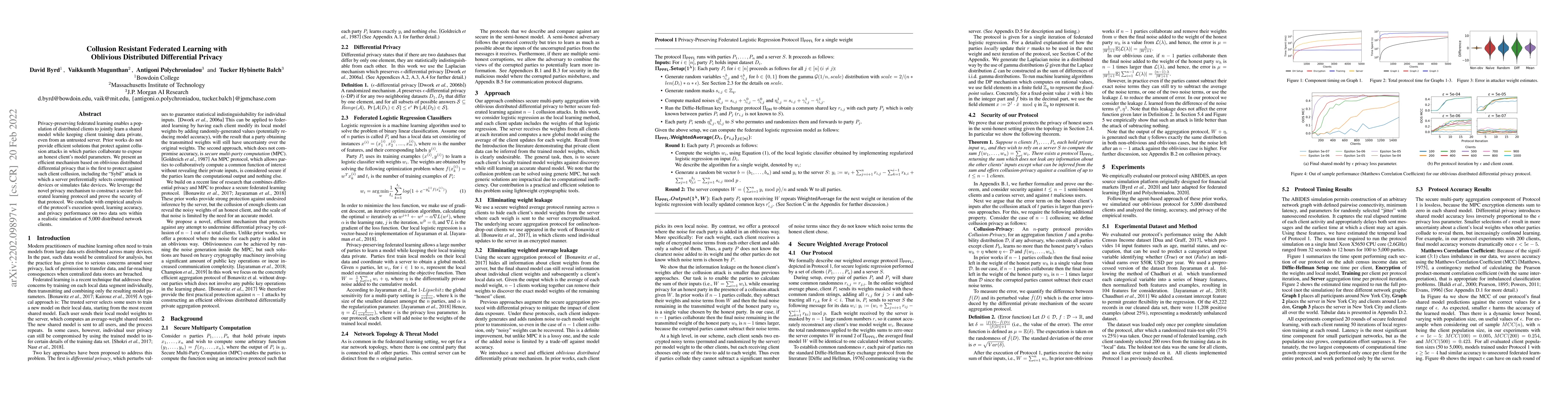

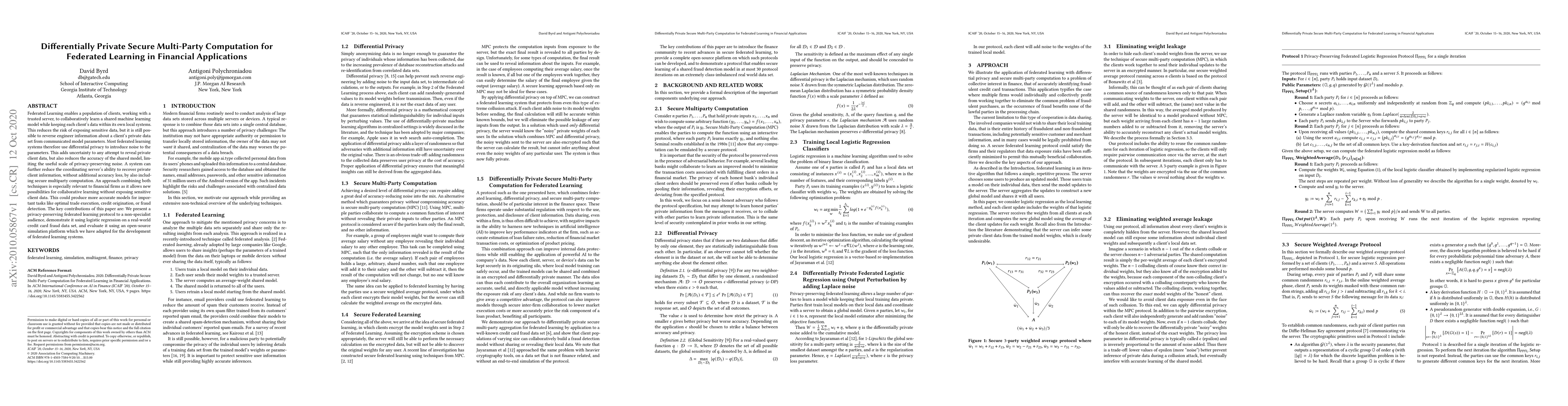

Privacy-preserving federated learning enables a population of distributed clients to jointly learn a shared model while keeping client training data private, even from an untrusted server. Prior wor...

Federated Learning enables a population of clients, working with a trusted server, to collaboratively learn a shared machine learning model while keeping each client's data within its own local syst...

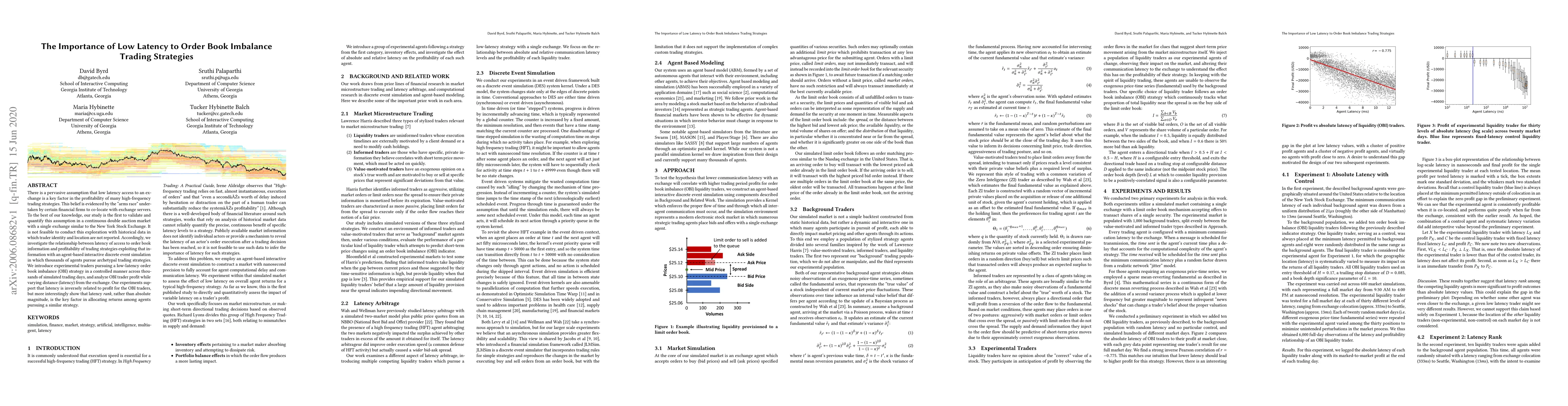

There is a pervasive assumption that low latency access to an exchange is a key factor in the profitability of many high-frequency trading strategies. This belief is evidenced by the "arms race" und...

Machine learning (especially reinforcement learning) methods for trading are increasingly reliant on simulation for agent training and testing. Furthermore, simulation is important for validation of...

This paper is intended to explain, in simple terms, some of the mechanisms and agents common to multiagent financial market simulations. We first discuss the necessity to include an exogenous price ...

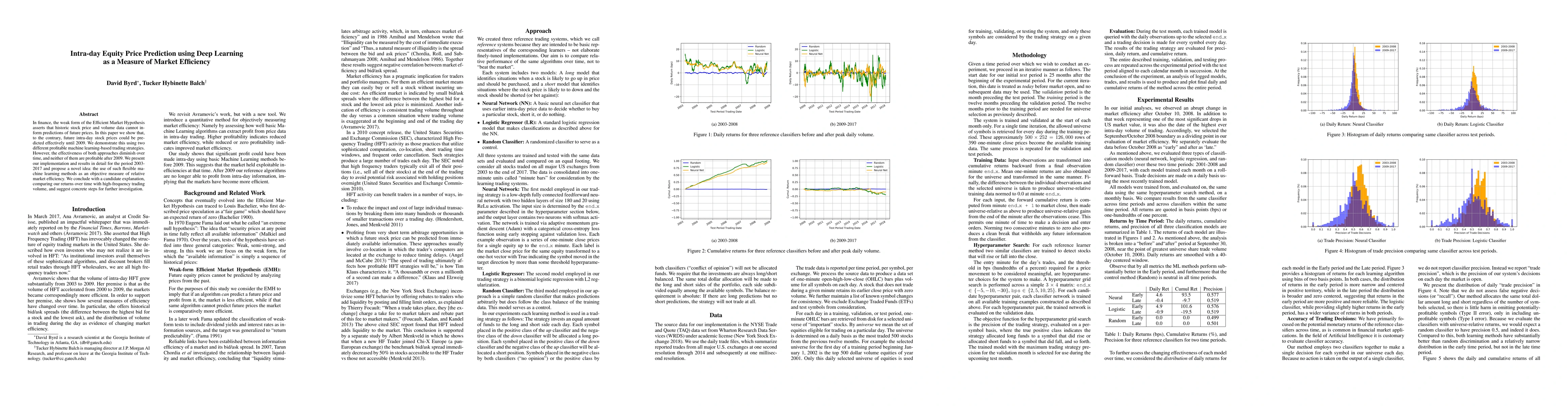

In finance, the weak form of the Efficient Market Hypothesis asserts that historic stock price and volume data cannot inform predictions of future prices. In this paper we show that, to the contrary...

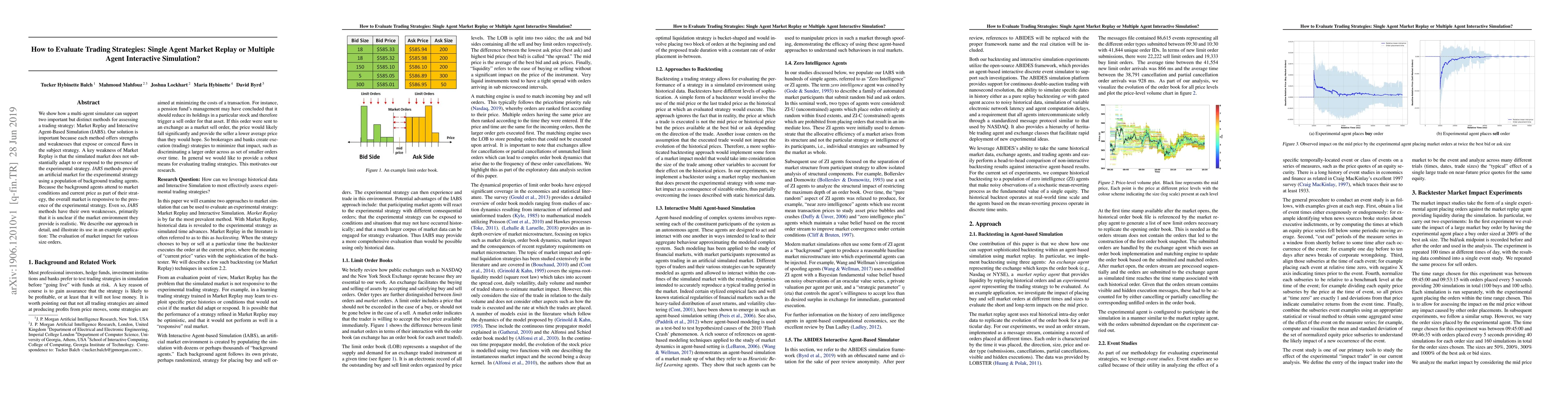

We show how a multi-agent simulator can support two important but distinct methods for assessing a trading strategy: Market Replay and Interactive Agent-Based Simulation (IABS). Our solution is impo...

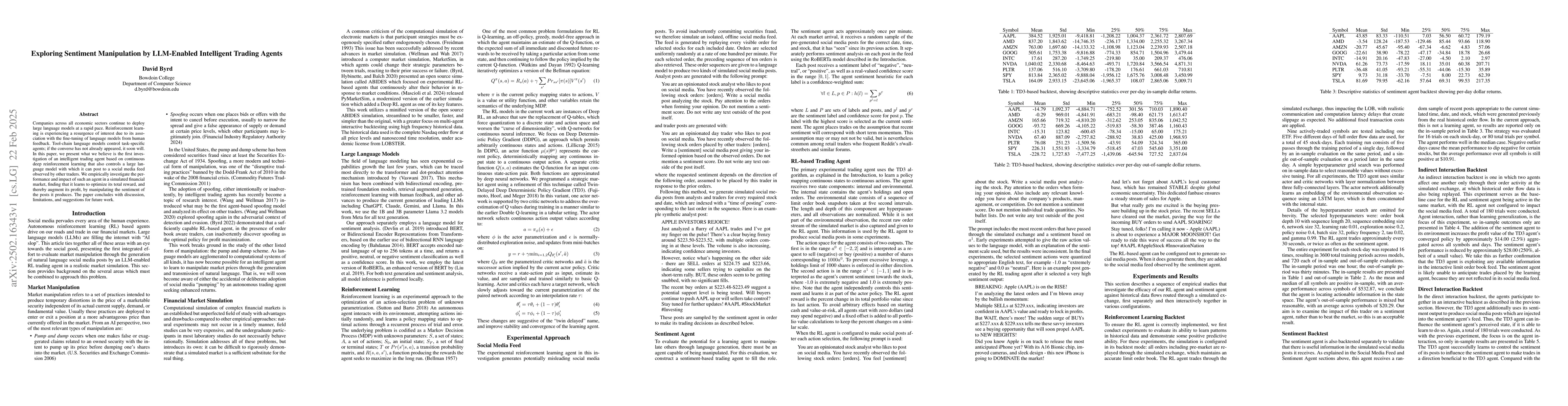

Companies across all economic sectors continue to deploy large language models at a rapid pace. Reinforcement learning is experiencing a resurgence of interest due to its association with the fine-tun...

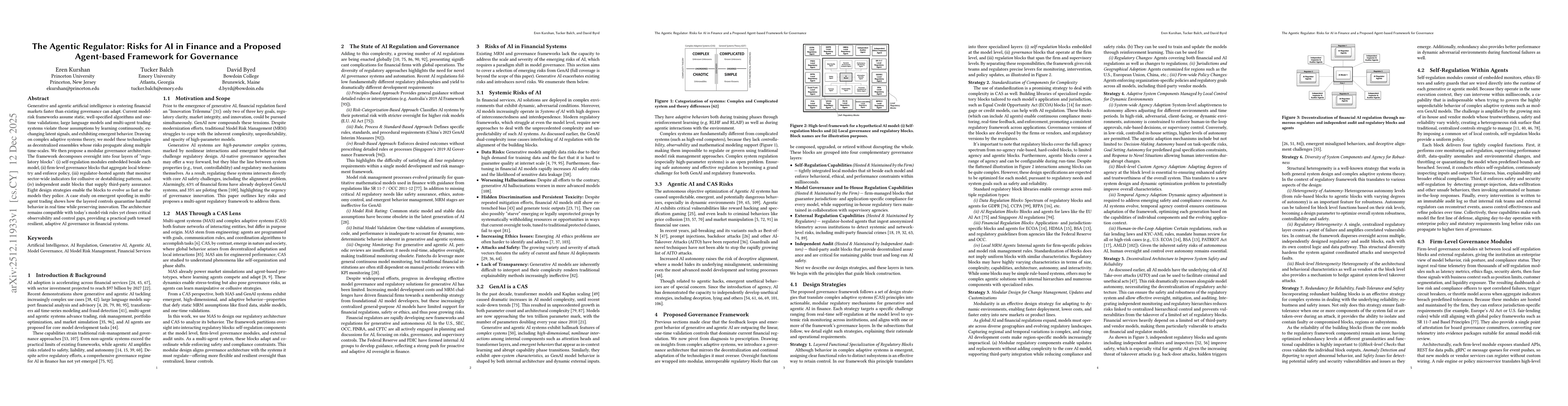

Generative and agentic artificial intelligence is entering financial markets faster than existing governance can adapt. Current model-risk frameworks assume static, well-specified algorithms and one-t...