Academic Profile

Statistics

Similar Authors

Papers on arXiv

Central Banks interventions are frequent in response to exogenous events with direct implications on financial market volatility. In this paper, we introduce the Asymmetric Jump Multiplicative Error...

The financial turmoil surrounding the Great Recession called for unprecedented intervention by Central Banks: unconventional policies affected various areas in the economy, including stock market vo...

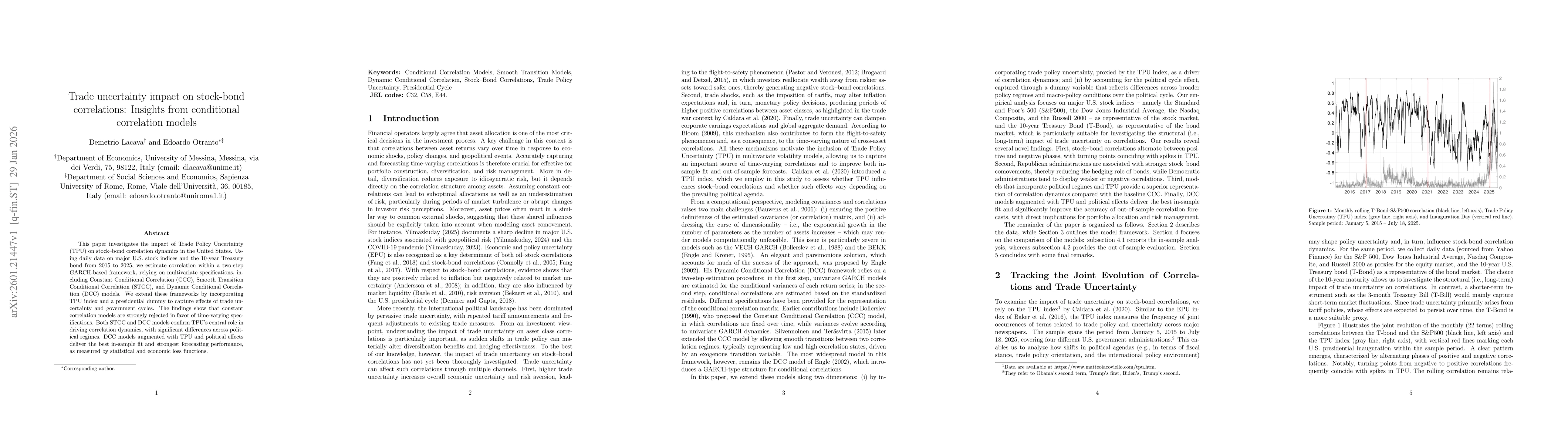

This paper investigates the impact of Trade Policy Uncertainty (TPU) on stock-bond correlation dynamics in the United States. Using daily data on major U.S. stock indices and the 10-year Treasury bond...

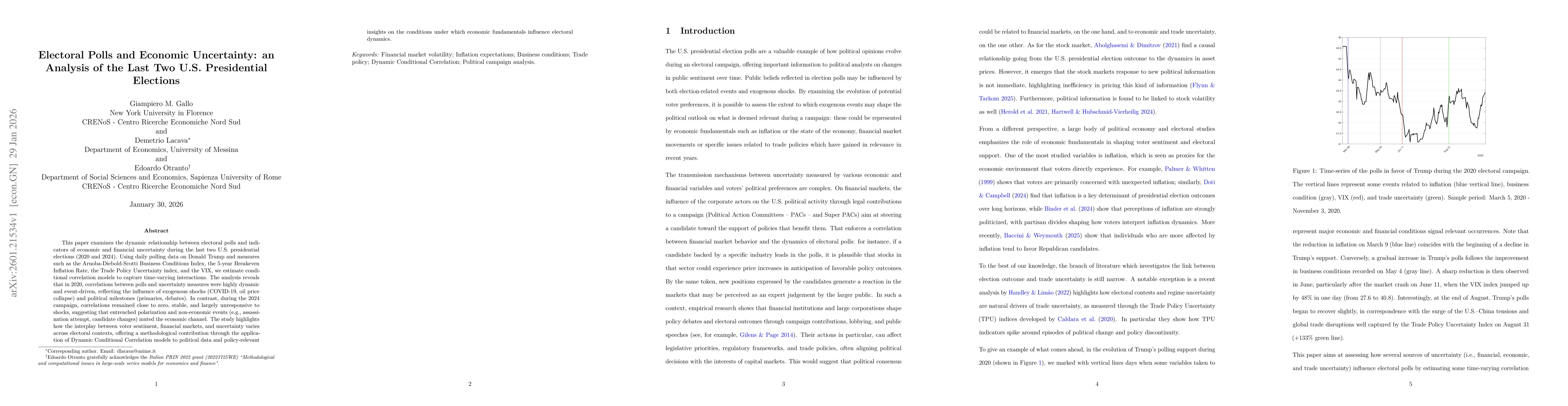

This paper examines the dynamic relationship between electoral polls and indicators of economic and financial uncertainty during the last two U.S. presidential elections (2020 and 2024). Using daily p...

This paper examines how trade policy uncertainty influences the correlation between U.S. stock indices and short-term government bonds. The objective is to assess whether policy-related shocks, especi...

This paper introduces a new extension of the Conditional Autoregressive Value at Risk (CAViaR) model aimed at improving tail risk forecasting across assets. The proposed component-based model, CAViaR ...