Academic Profile

Statistics

Similar Authors

Papers on arXiv

Monotonicity is a key qualitative prediction of a wide array of economic models derived via robust comparative statics. It is therefore important to design effective and practical econometric method...

In this paper, we derive non-asymptotic error bounds for the Lasso estimator when the penalty parameter for the estimator is chosen using $K$-fold cross-validation. Our bounds imply that the cross-v...

I review some of the main methods for selecting tuning parameters in nonparametric and $\ell_1$-penalized estimation. For the nonparametric estimation, I consider the methods of Mallows, Stein, Leps...

We propose a new non-linear single-factor asset pricing model $r_{it}=h(f_{t}\lambda_{i})+\epsilon_{it}$. Despite its parsimony, this model represents exactly any non-linear model with an arbitrary ...

This article introduces the R package csranks for estimation and inference involving ranks. First, we review methods for the construction of confidence sets for ranks, namely marginal and simultaneo...

We propose logit-based IV and augmented logit-based IV estimators that serve as alternatives to the traditionally used 2SLS estimator in the model where both the endogenous treatment variable and th...

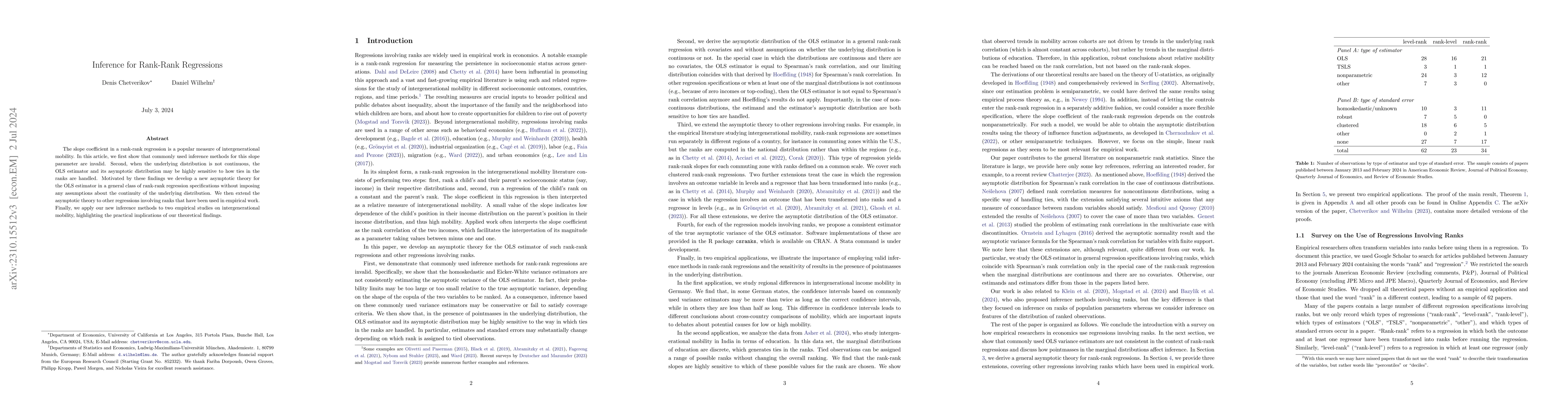

The slope coefficient in a rank-rank regression is a popular measure of intergenerational mobility. In this article, we first show that commonly used inference methods for this slope parameter are i...

We examine asymptotic properties of the OLS estimator when the values of the regressor of interest are assigned randomly and independently of other regressors. We find that the OLS variance formula ...

In this paper, we develop spectral and post-spectral estimators for grouped panel data models. Both estimators are consistent in the asymptotics where the number of observations $N$ and the number o...

This article reviews recent progress in high-dimensional bootstrap. We first review high-dimensional central limit theorems for distributions of sample mean vectors over the rectangles, bootstrap co...

In this paper, we introduce the weighted-average quantile regression framework, $\int_0^1 q_{Y|X}(u)\psi(u)du = X'\beta$, where $Y$ is a dependent variable, $X$ is a vector of covariates, $q_{Y|X}$ ...

We develop a new method for selecting the penalty parameter for $\ell_1$-penalized M-estimators in high dimensions, which we refer to as bootstrapping after cross-validation. We derive rates of conv...

This paper deals with the Gaussian and bootstrap approximations to the distribution of the max statistic in high dimensions. This statistic takes the form of the maximum over components of the sum o...

We show that the higher-orders and their interactions of the common sparse linear factors can effectively subsume the factor zoo. To this extend, we propose a forward selection Fama-MacBeth procedure ...

In this paper, we propose a triple (or double-debiased) Lasso estimator for inference on a low-dimensional parameter in high-dimensional linear regression models. The estimator is based on a moment fu...

We study inference using trimmed least squares (TLS) and trimmed least absolute deviations (TLAD) estimators of \citet{honore_trimmed_1992} in censored two-period panel-data models with fixed effects....