Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper addresses the prevalent issue of label shift in an online setting with missing labels, where data distributions change over time and obtaining timely labels is challenging. While existing...

We consider the problem of heteroscedastic linear regression, where, given $n$ samples $(\mathbf{x}_i, y_i)$ from $y_i = \langle \mathbf{w}^{*}, \mathbf{x}_i \rangle + \epsilon_i \cdot \langle \math...

This paper focuses on supervised and unsupervised online label shift, where the class marginals $Q(y)$ varies but the class-conditionals $Q(x|y)$ remain invariant. In the unsupervised setting, our g...

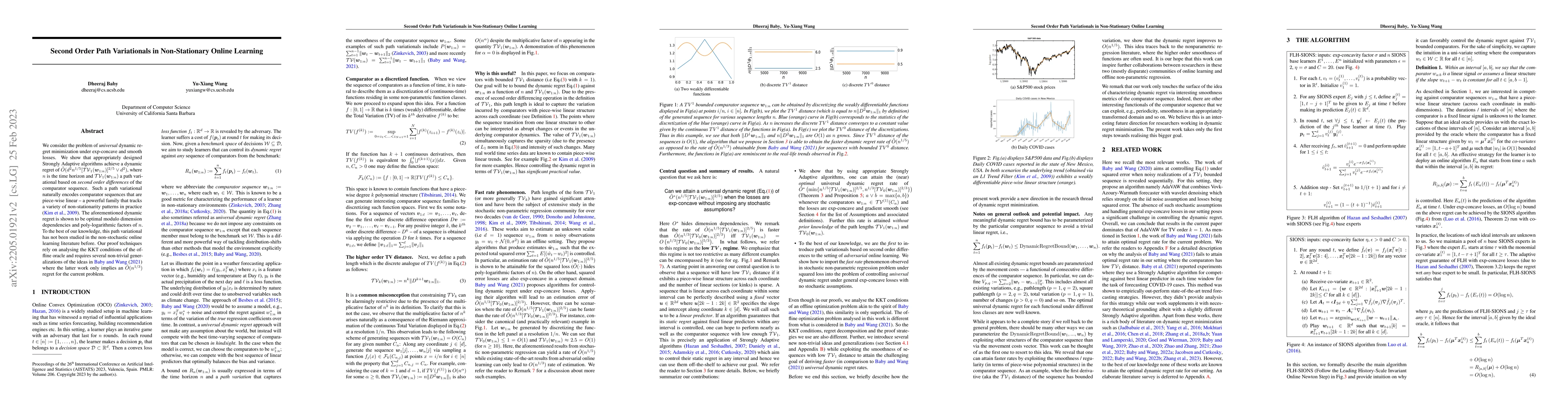

We consider the problem of nonstochastic control with a sequence of quadratic losses, i.e., LQR control. We provide an efficient online algorithm that achieves an optimal dynamic (policy) regret of ...

We consider the problem of universal dynamic regret minimization under exp-concave and smooth losses. We show that appropriately designed Strongly Adaptive algorithms achieve a dynamic regret of $\t...

We study the framework of universal dynamic regret minimization with strongly convex losses. We answer an open problem in Baby and Wang 2021 by showing that in a proper learning setup, Strongly Adap...

We consider the framework of non-stationary Online Convex Optimization where a learner seeks to control its dynamic regret against an arbitrary sequence of comparators. When the loss functions are s...

We consider the problem of the Zinkevich (2003)-style dynamic regret minimization in online learning with exp-concave losses. We show that whenever improper learning is allowed, a Strongly Adaptive ...

We consider the problem of estimating a function from $n$ noisy samples whose discrete Total Variation (TV) is bounded by $C_n$. We reveal a deep connection to the seemingly disparate problem of Str...

We consider the framework of non-stationary stochastic optimization [Besbes et al, 2015] with squared error losses and noisy gradient feedback where the dynamic regret of an online learner against a...

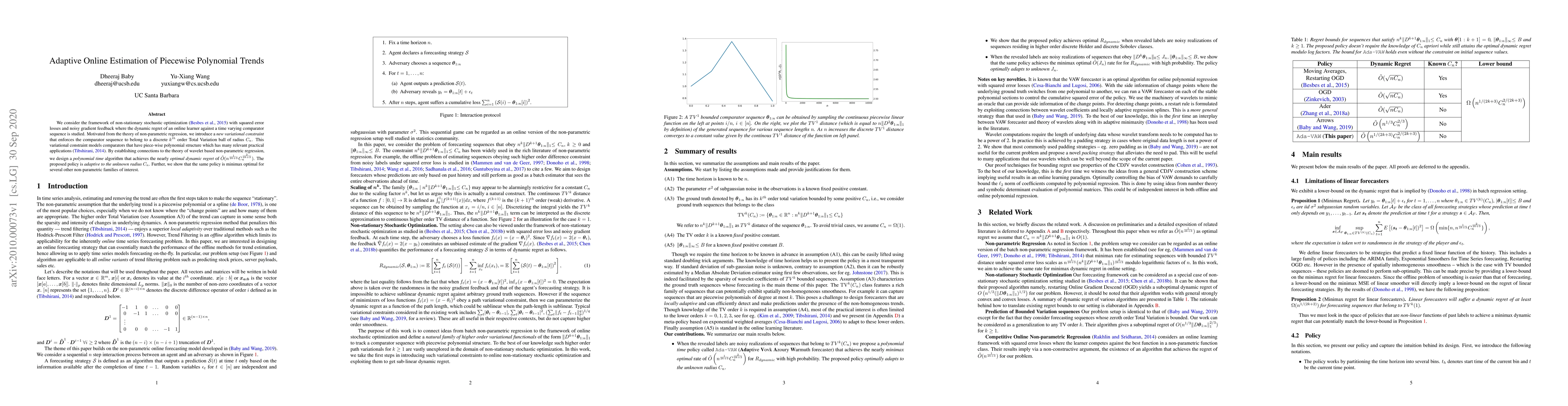

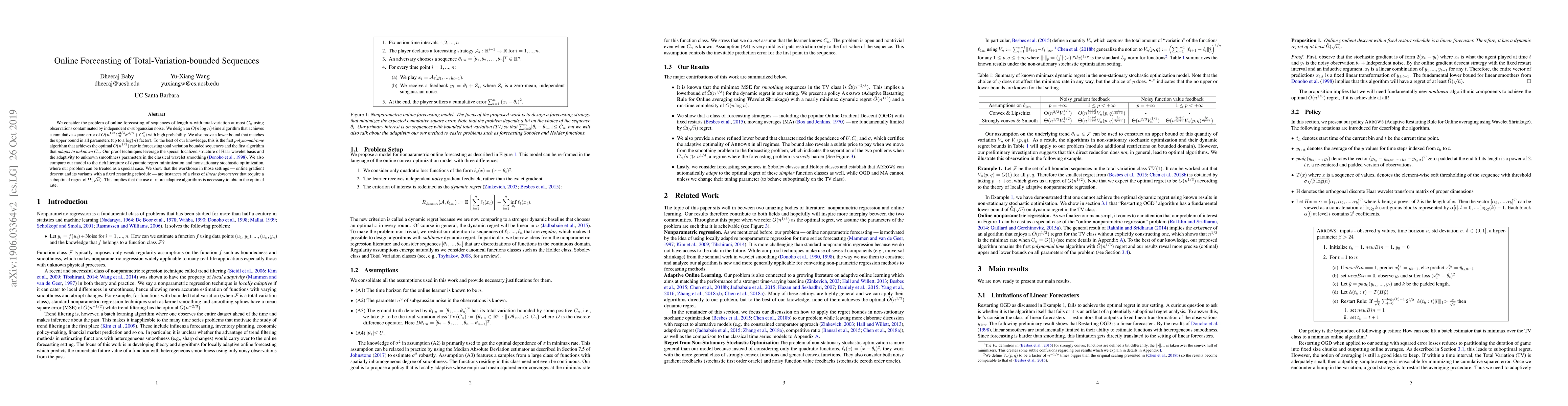

We consider the problem of online forecasting of sequences of length $n$ with total-variation at most $C_n$ using observations contaminated by independent $\sigma$-subgaussian noise. We design an $O...

We investigate the low rank matrix completion problem in an online setting with ${M}$ users, ${N}$ items, ${T}$ rounds, and an unknown rank-$r$ reward matrix ${R}\in \mathbb{R}^{{M}\times {N}}$. This ...

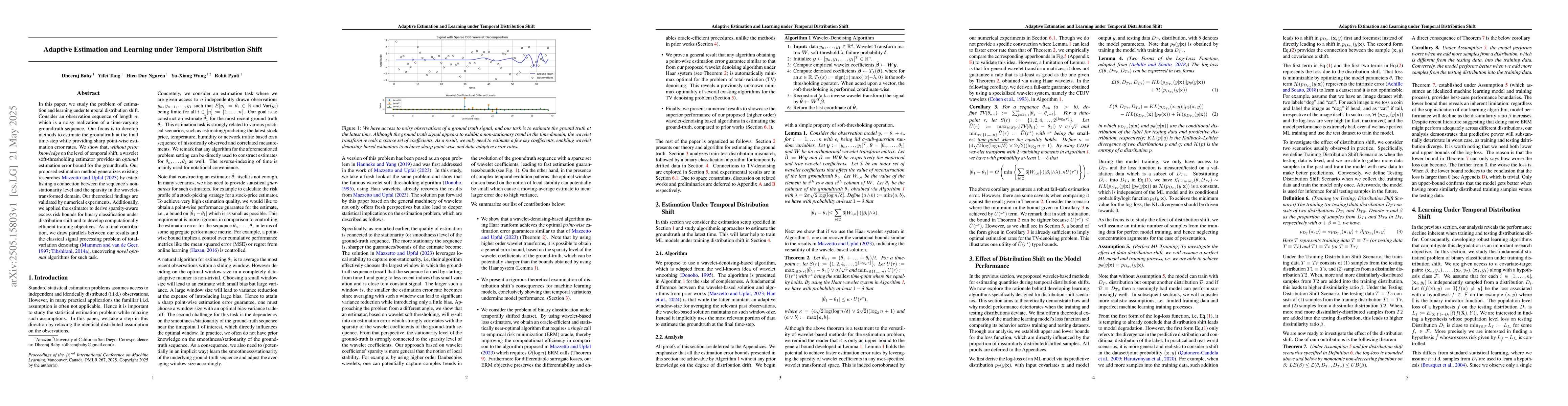

In this paper, we study the problem of estimation and learning under temporal distribution shift. Consider an observation sequence of length $n$, which is a noisy realization of a time-varying groundt...