Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a multicountry quantile factor augmeneted vector autoregression (QFAVAR) to model heterogeneities both across countries and across characteristics of the distributions of macroeconomic ti...

When agents' information is imperfect and dispersed, existing measures of macroeconomic uncertainty based on the forecast error variance have two distinct drivers: the variance of the economic shock...

A comprehensive methodology for inference in vector autoregressions (VARs) using sign and other structural restrictions is developed. The reduced-form VAR disturbances are driven by a few common fac...

In all areas of human knowledge, datasets are increasing in both size and complexity, creating the need for richer statistical models. This trend is also true for economic data, where high-dimension...

As the amount of economic and other data generated worldwide increases vastly, a challenge for future generations of econometricians will be to master efficient algorithms for inference in empirical...

This paper proposes two distinct contributions to econometric analysis of large information sets and structural instabilities. First, it treats a regression model with time-varying coefficients, sto...

This paper proposes a variational Bayes algorithm for computationally efficient posterior and predictive inference in time-varying parameter (TVP) models. Within this context we specify a new dynami...

I introduce a high-dimensional Bayesian vector autoregressive (BVAR) framework designed to estimate the effects of conventional monetary policy shocks. The model captures structural shocks as latent f...

We revisit macroeconomic time-varying parameter vector autoregressions (TVP-VARs), whose persistent coefficients may adapt too slowly to large, abrupt shifts such as those during major crises. We expl...

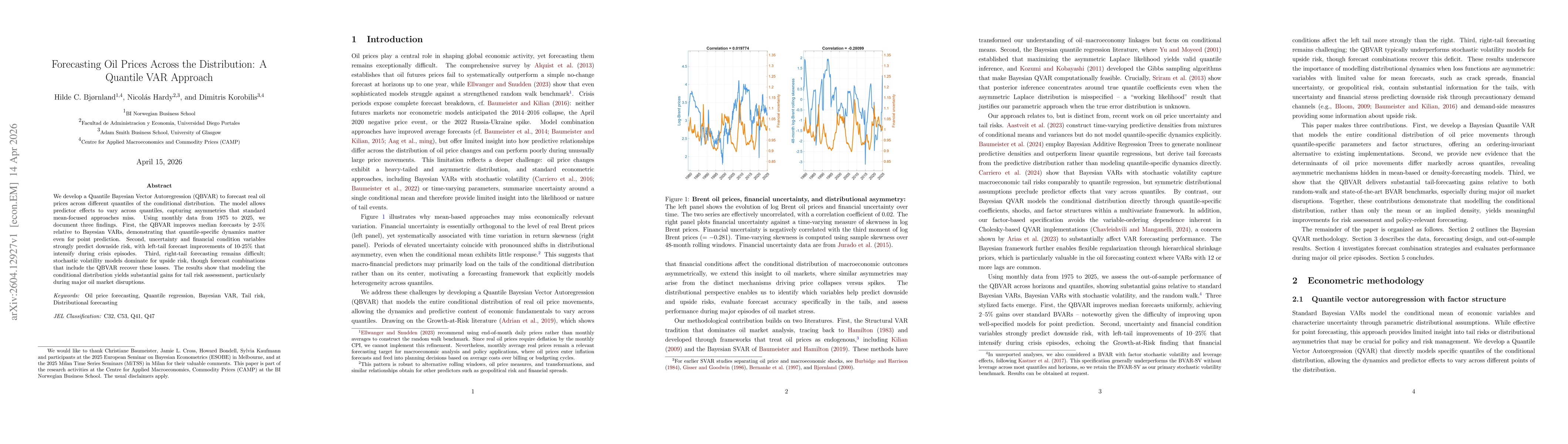

We develop a Quantile Bayesian Vector Autoregression (QBVAR) to forecast real oil prices across different quantiles of the conditional distribution. The model allows predictor effects to vary across q...