Academic Profile

Statistics

Similar Authors

Papers on arXiv

The standard approach for constructing a Mean-Variance portfolio involves estimating parameters for the model using collected samples. However, since the distribution of future data may not resemble t...

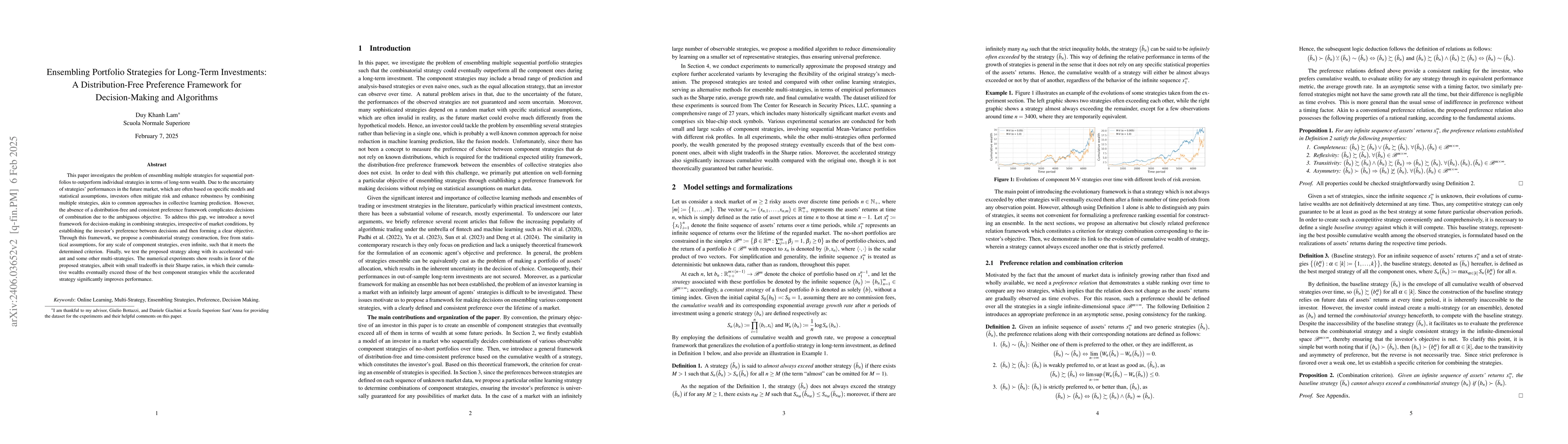

This paper investigates the problem of ensembling multiple strategies for sequential portfolios to outperform individual strategies in terms of long-term wealth. Due to the uncertainty of strategies...

This paper investigates the investment problem of constructing an optimal no-short sequential portfolio strategy in a market with a latent dependence structure between asset prices and partly unobserv...

In the online portfolio optimization framework, existing learning algorithms generate strategies that yield significantly poorer cumulative wealth compared to the best constant rebalancing portfolio i...