Academic Profile

Statistics

Similar Authors

Papers on arXiv

We provide a unified approach to a priori estimates for supersolutions of BSDEs in general filtrations, which may not be quasi left-continuous. Unlike the previous related approaches in simpler sett...

This paper is devoted to obtaining a wellposedness result for multidimensional BSDEs with possibly unbounded random time horizon and driven by a general martingale in a filtration only assumed to sa...

In this paper, we provide a general approach to reformulating any continuous-time stochastic Stackelberg differential game under closed-loop strategies as a single-level optimisation problem with ta...

This paper addresses a continuous-time contracting model that extends the problem introduced by Sannikov and later rigorously analysed by Possama\"{i} and Touzi. In our model, a principal hires a ri...

We study a generic principal-agent problem in continuous time on a finite time horizon. We introduce a framework in which the agent is allowed to employ measure-valued controls and characterise the ...

Commuters looking for the shortest path to their destinations, the security of networked computers, hedge funds trading on the same stocks, governments and populations acting to mitigate an epidemic...

We are interested in the study of stochastic games for which each player faces an optimal stopping problem. In our setting, the players may interact through the criterion to optimise as well as thro...

We prove well-posedness results for backward stochastic differential equations (BSDEs) and reflected BSDEs with an optional obstacle process in the case of appropriately weighted $\mathbb{L}^2$-data...

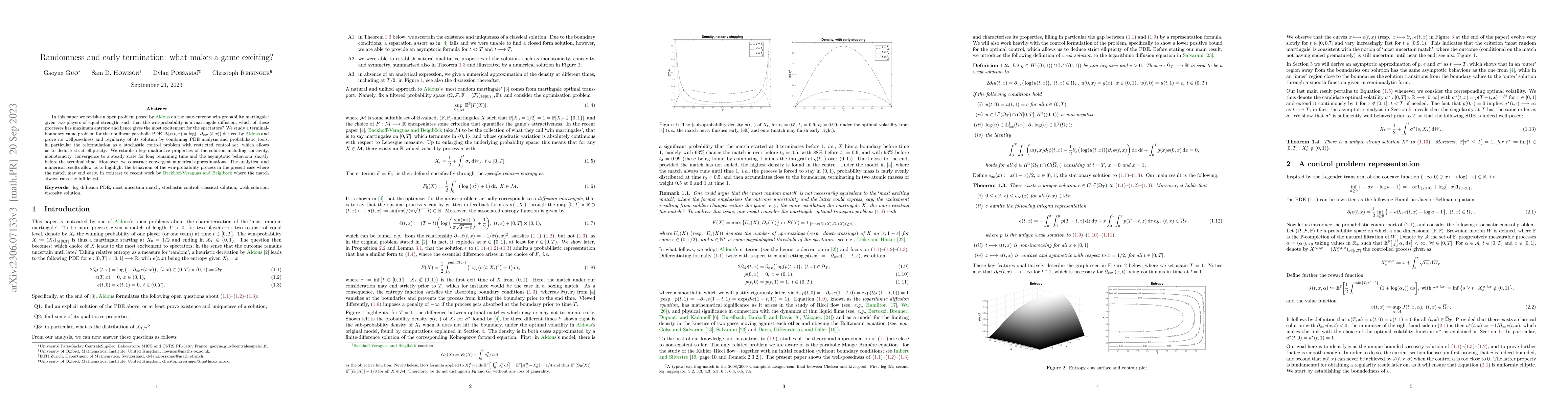

In this paper we revisit an open problem posed by Aldous on the max-entropy win-probability martingale: given two players of equal strength, such that the win-probability is a martingale diffusion, ...

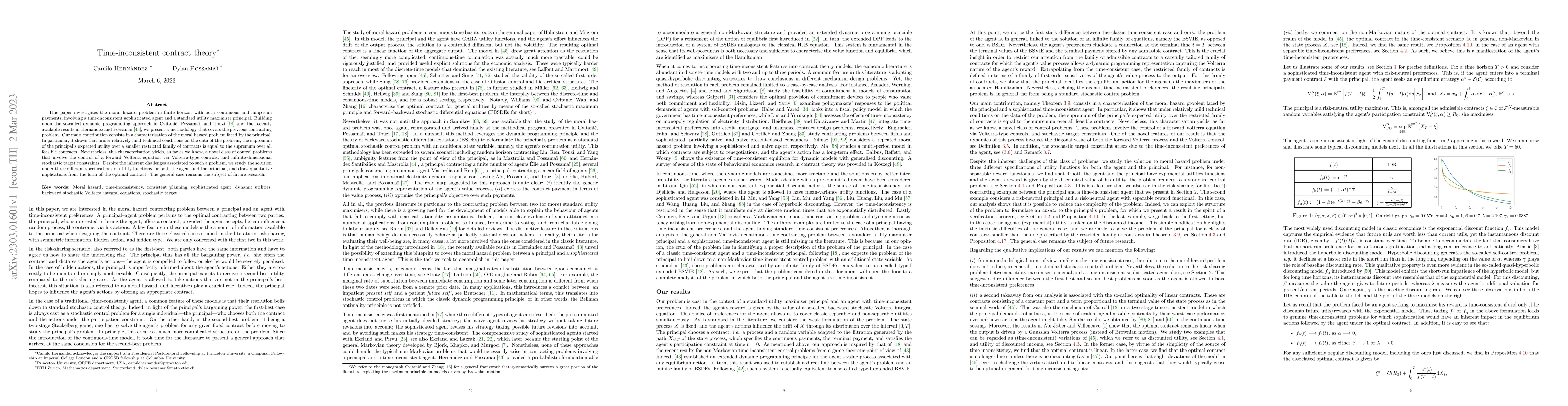

This paper investigates the moral hazard problem in finite horizon with both continuous and lump-sum payments, involving a time-inconsistent sophisticated agent and a standard utility maximiser prin...

We design a market-making model \`a la Avellaneda-Stoikov in which the market-takers act strategically, in the sense that they design their trading strategy based on an exogenous trading signal. The...

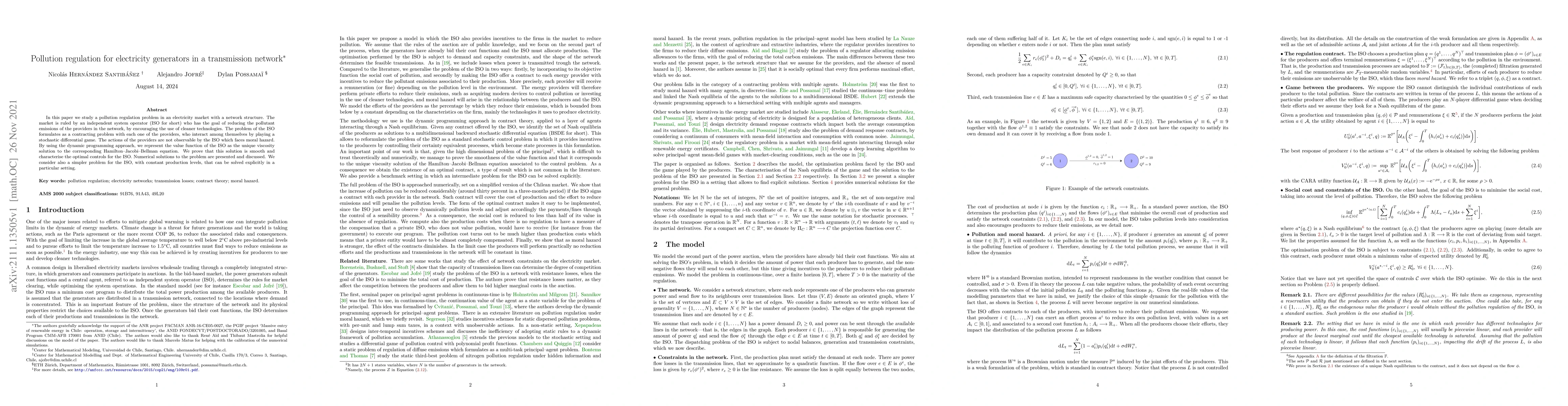

In this paper we study a pollution regulation problem in an electricity market with a network structure. The market is ruled by an independent system operator (ISO for short) who has the goal of red...

In this paper, we obtain stability results for backward stochastic differential equations with jumps (BSDEs) in a very general framework. More specifically, we consider a convergent sequence of stan...

This work is mainly concerned with the so-called limit theory for mean-field games. Adopting the weak formulation paradigm put forward by Carmona and Lacker, we consider a fully non-Markovian settin...

Motivated by the recent studies on the green bond market, we build a model in which an investor trades on a portfolio of green and conventional bonds, both issued by the same governmental entity. Th...

In this work, we provide a general mathematical formalism to study the optimal control of an epidemic, such as the COVID-19 pandemic, via incentives to lockdown and testing. In particular, we model ...

This paper provides a complete review of the continuous-time optimal contracting problem introduced by Sannikov, in the extended context allowing for possibly different discount rates for both parti...

Following the recent literature on make take fees policies, we consider an exchange wishing to set a suitable contract with several market makers in order to improve trading quality on its platform....

We study the McKean-Vlasov optimal control problem with common noise in various formulations, namely the strong and weak formulation, as well as the Markovian and non-Markovian formulations, and all...

We study the problem of demand response contracts in electricity markets by quantifying the impact of considering a mean-field of consumers, whose consumption is impacted by a common noise. We formu...

We study risk-sharing economies where heterogenous agents trade subject to quadratic transaction costs. The corresponding equilibrium asset prices and trading strategies are characterised by a syste...

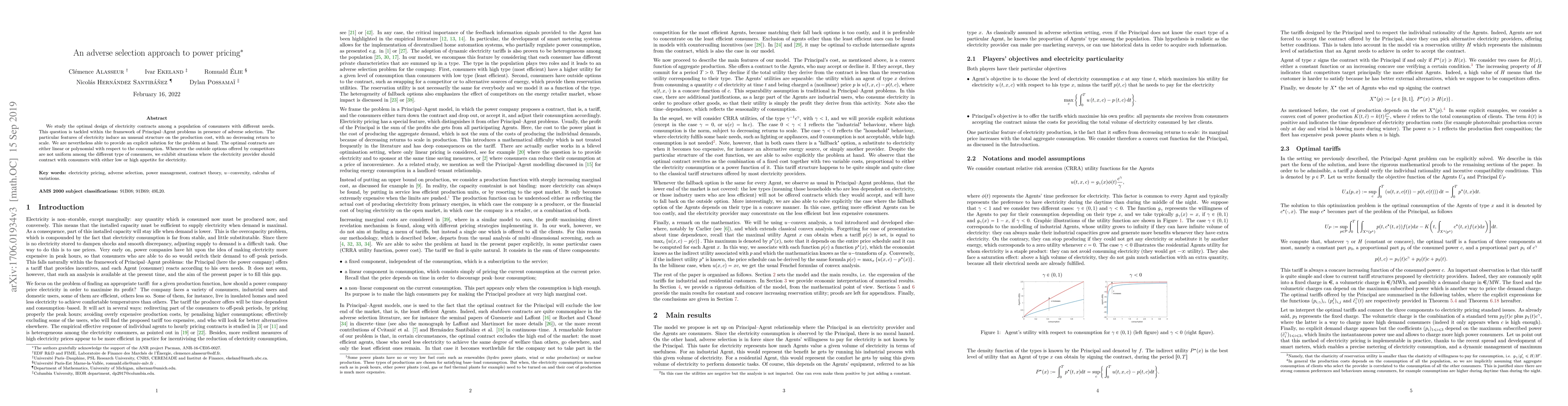

We study the optimal design of electricity contracts among a population of consumers with different needs. This question is tackled within the framework of Principal-Agent problems in presence of ad...

In this paper, we propose a new policy iteration algorithm to compute the value function and the optimal controls of continuous time stochastic control problems. The algorithm relies on successive app...

We construct an aggregated version of the value processes associated with stochastic control problems, where the criterion to optimise is given by solutions to semi-martingale backward stochastic diff...

As the mathematical capabilities of large language models (LLMs) improve, it becomes increasingly important to evaluate their performance on research-level tasks at the frontier of mathematical knowle...

We introduce a mild generative variant of the classical neural operator model, which leverages Kolmogorov--Arnold networks to solve infinite families of second-order backward stochastic differential e...

This paper focuses on the optimal control of a class of stochastic Volterra integral equations. Here the coefficients are regular and not assumed to be of convolution type. We show that, under mild re...

We investigate a time-inconsistent, non-Markovian finite-player game in continuous time, where each player's objective functional depends non-linearly on the expected value of the state process. As a ...

This paper addresses the challenge of time-inconsistent stochastic control within a continuous-time framework. Its primary focus lies in uncovering a probabilistic representation, specifically in the ...

This paper characterises optimal incentive schemes for ESG disclosure in a continuous-time principal-agent setting. We model a risk-averse principal (e.g., a platform or standard-setter) contracting w...