Academic Profile

Statistics

Similar Authors

Papers on arXiv

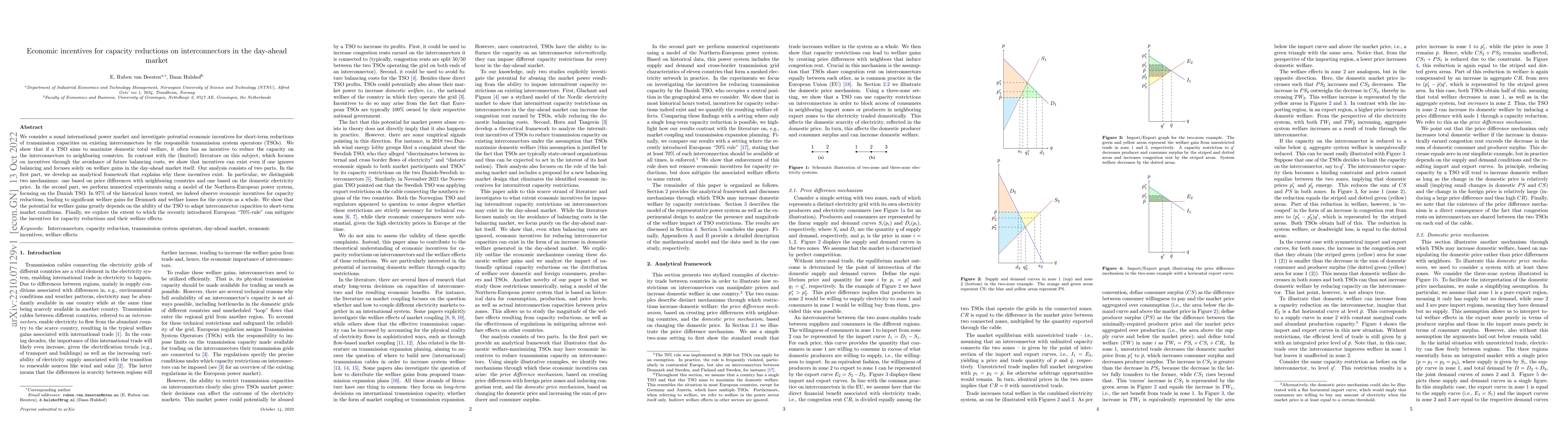

We consider a zonal international power market and investigate potential economic incentives for short-term reductions of transmission capacities on existing interconnectors by the responsible trans...

Inspired by its success for their continuous counterparts, the standard approach to deal with mixed-integer recourse (MIR) models under distributional uncertainty is to use distributionally robust o...

We consider two-stage recourse models in which the second-stage problem has integer decision variables and uncertainty in the second-stage cost vector, technology matrix, and the right-hand side vec...

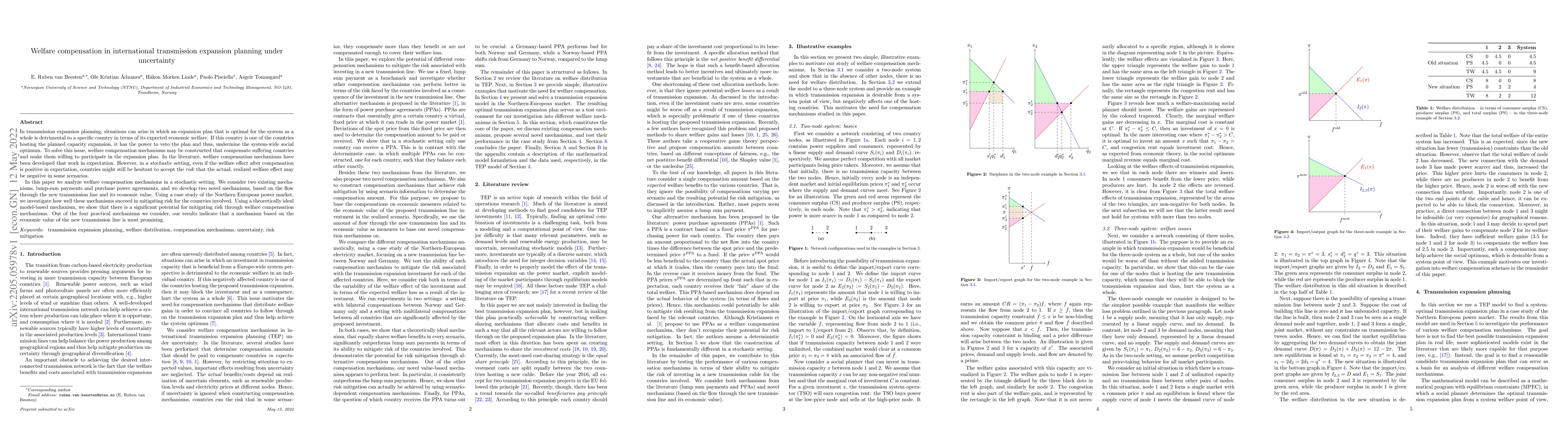

In transmission expansion planning, situations can arise in which an expansion plan that is optimal for the system as a whole is detrimental to a specific country in terms of its expected economic w...

I propose a functional on the space of spectral risk measures that quantifies their ``degree of risk aversion''. This quantification formalizes the idea that some risk measures are ``more risk-averse'...

In an optimization problem, the quality of a candidate solution can be characterized by the optimality gap. For most stochastic optimization problems, this gap must be statistically estimated. We show...