Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the numerical approximation of the stochastic heat equation with a distributional reaction term. Under a condition on the Besov regularity of the reaction term, it was proven recently that ...

We investigate the problem of joint statistical estimation of several parameters for a stochastic differential equation driven by an additive fractional Brownian motion. Based on discrete-time obser...

We study the numerical approximation of multidimensional stochastic differential equations (SDEs) with distributional drift, driven by a fractional Brownian motion. We work under the Catellier-Gubin...

The fractional Brownian motion can be considered as a Gaussian field indexed by $(t,H)\in { \mathbb{R}_{+} \times (0,1)}$, where $H$ is the Hurst parameter. On compact time intervals, it is known to...

In this work, we consider the setting of learning problems under a wide class of spectral risk (or "L-risk") functions, where a Lipschitz-continuous spectral density is used to flexibly assign weigh...

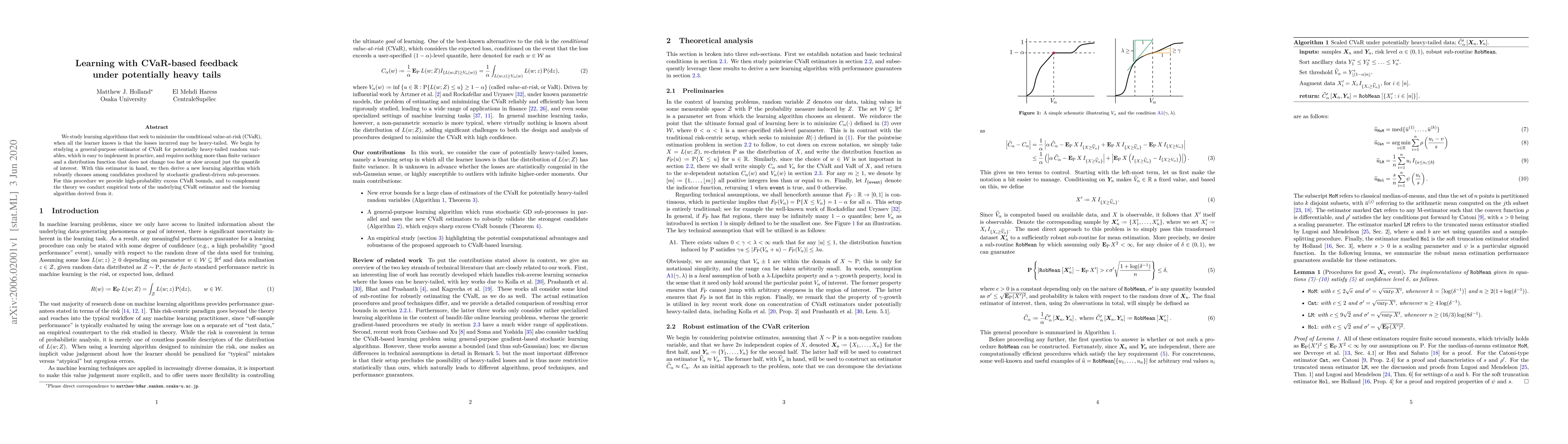

We study learning algorithms that seek to minimize the conditional value-at-risk (CVaR), when all the learner knows is that the losses incurred may be heavy-tailed. We begin by studying a general-pu...

Let the Ornstein-Uhlenbeck process $(X_t)_{t\ge0}$ driven by a fractional Brownian motion $B^{H }$, described by $dX_t = -\theta X_t dt + \sigma dB_t^{H }$ be observed at discrete time instants $t...

We study the long-time behaviour of solutions to a class of $d$-dimensional stochastic differential equations driven by fractional Brownian motion with Hurst parameter $H \in (0,1)$. The drift consist...