Academic Profile

Statistics

Similar Authors

Papers on arXiv

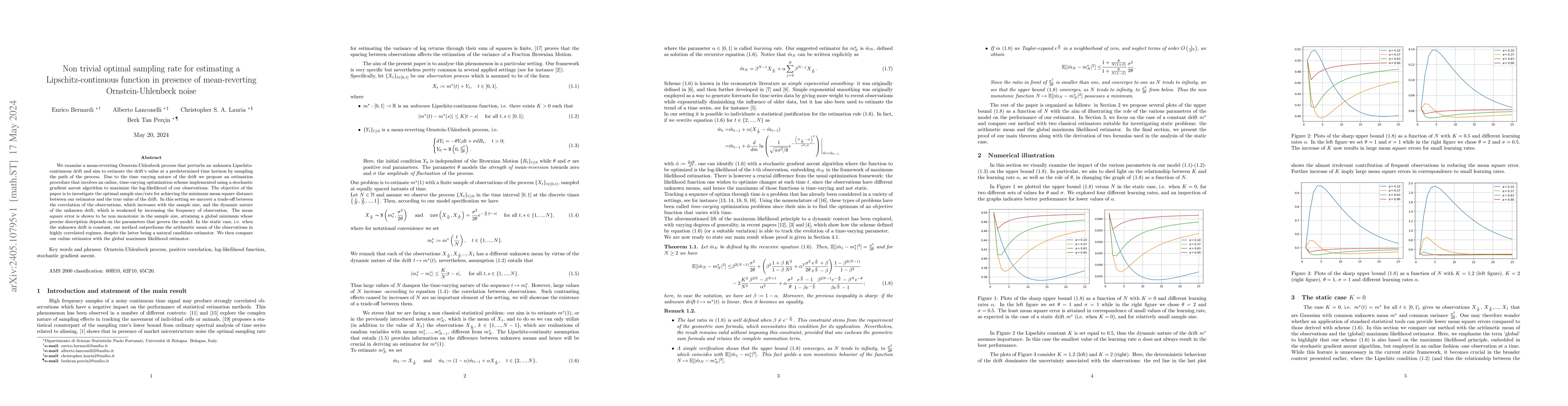

We examine a mean-reverting Ornstein-Uhlenbeck process that perturbs an unknown Lipschitz-continuous drift and aim to estimate the drift's value at a predetermined time horizon by sampling the path ...

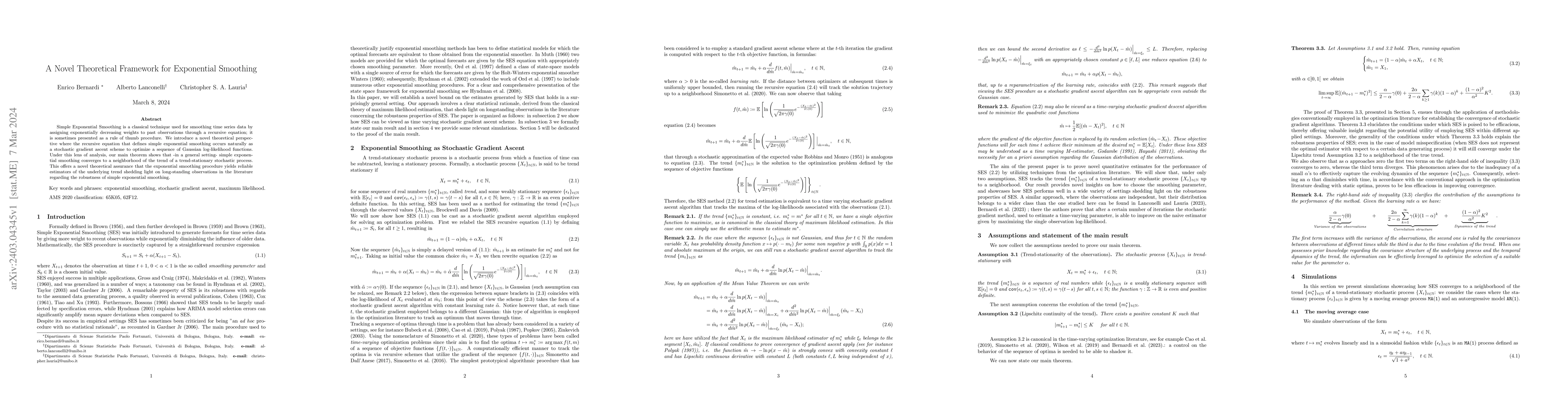

Simple Exponential Smoothing is a classical technique used for smoothing time series data by assigning exponentially decreasing weights to past observations through a recursive equation; it is somet...

This paper provides a comprehensive estimation framework for large covariance matrices via a log-det heuristics augmented by a nuclear norm plus $l_{1}$ norm penalty. %We develop the model framework...

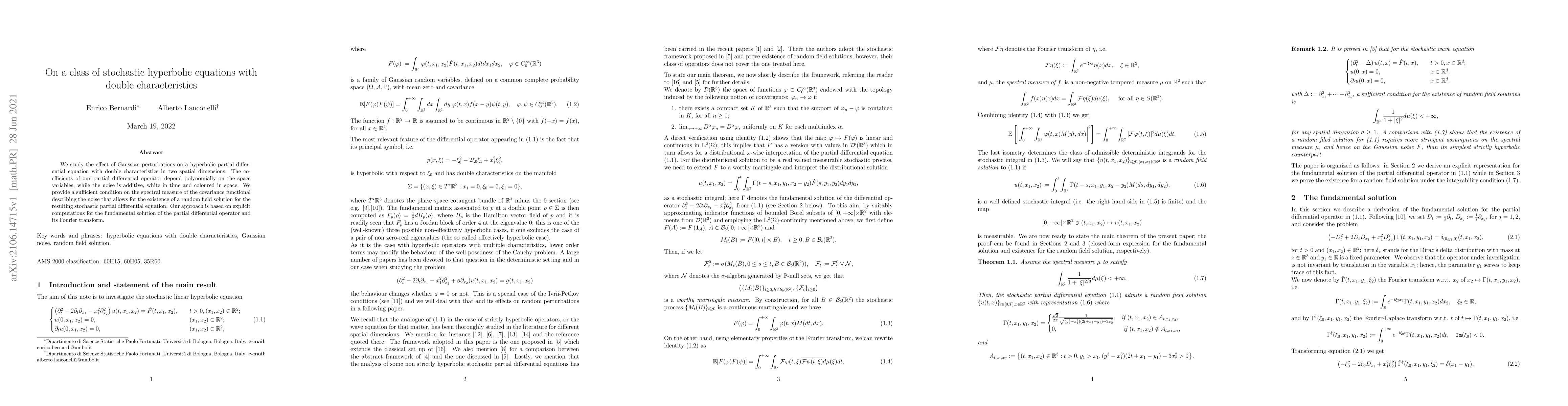

We study the effect of Gaussian perturbations on a hyperbolic partial differential equation with double characteristics in two spatial dimensions. The coefficients of our partial differential operat...

We perturb with an additive Gaussian white noise the Hamiltonian system associated to a cubic anharmonic oscillator. The stochastic system is assumed to start from initial conditions that guarantee ...

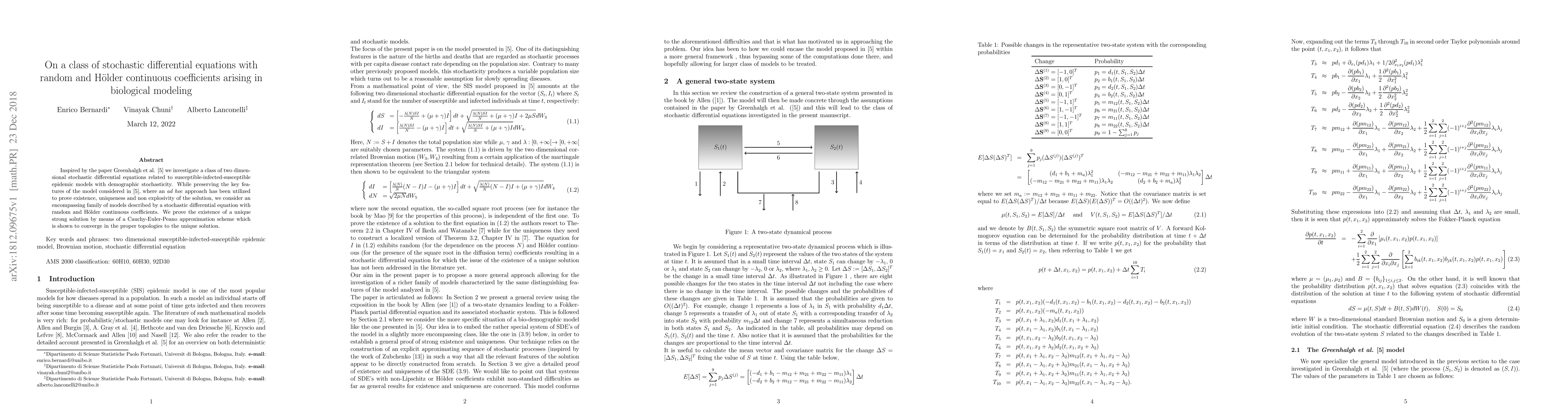

Inspired by the paper Greenhalgh et al. [5] we investigate a class of two dimensional stochastic differential equations related to susceptible-infected-susceptible epidemic models with demographic s...

We study the effect of Gaussian perturbations on a class of model hyperbolic partial differential equations with double symplectic characteristics in low spatial dimensions, extending some recen...

In this paper we study a class of non-effectively hyperbolic operators vanishing of order 2 on a manifold, on a sub-region of which the spectral structure of the Hamilton map changes type. Suitable no...

We exhibit a family of second-order hyperbolic differential operators presenting spectral transition of the Hamilton map. As a consequence we prove that the Cauchy problem is not locally solvable at t...

We study a class of Tricomi-type partial differential equations previously investigated in [28]. Firstly, we generalize the representation formula for the solution obtained there by allowing the coeff...

We present an example of a linear partial differential equation whose Cauchy problem becomes well-posed when perturbed by noise. Specifically, we make clear how a suitable multiplicative Stratonovich ...

We prove that the Cauchy problem for the model hyperbolic operator in $ \R^{4} $ \[ Q=-D_t^2+2xD_tD_y+D_x^2+x^3D_y^2+D_z^2+z^2D_y^2 \] is not locally solvable at the origin, in the Gevrey $s$ class if...

We study the Cauchy problem for the Tricomi equation perturbed by space-time Gaussian White Noise. To prove existence and uniqueness of the solution, we employ a Fourier transform approach that allows...